LightCastle Analytics Wing

LightCastle Analytics Wing

Key Insights from the Networking Session of Bangladesh’s 2030 Outlook of the RMG Sector

Bangladesh’s recent negotiation with the United States on reciprocal tariffs has reinforced its position as a reliable sourcing hub. Yet, beneath this diplomatic success lies a more sobering reality. The deal required Bangladesh to open its markets to more US products, underscoring how vulnerable an export-dependent economy remains when over 80% of its earnings hinge on one sector.

This tectonic shift in the international trade regime might have a short to medium-term adverse impact on global trade flow. Higher tariffs in the U.S. could dampen their domestic demand and affect exporters across key markets, including Bangladesh. Within this evolving trade, to remain competitive, the ready-made garments (RMG) sector should shift from volume-based expansion to resilience-led competitiveness, where innovation, diversification, and sustainability define long-term success.

To reflect on this transition, LightCastle Partners recently hosted an exclusive networking session titled “Stitching Tomorrow: 2030 Outlook” under the Oporajita Phase 2 initiative. The event convened industry leaders, policymakers, and development partners to deliberate on the evolving trajectory of Bangladesh’s RMG sector.

Discussions centred on the sector’s critical priorities—trade realignments, sustainability transitions, and worker wellbeing. Building upon those insights, this article examines how these dynamics are shaping the next phase of Bangladesh’s trade diplomacy and industrial strategy.

The Imperative for Action: Diving Deep into the Key Insights

The RMG industry now stands at a crossroads. Its future will be defined by how effectively it balances three intertwined priorities: economic competitiveness, social inclusion, and environmental compliance. These dimensions are no longer optional; they increasingly determine market access and investor confidence.

Shifting Global Trade Dynamics and Market Access Threats

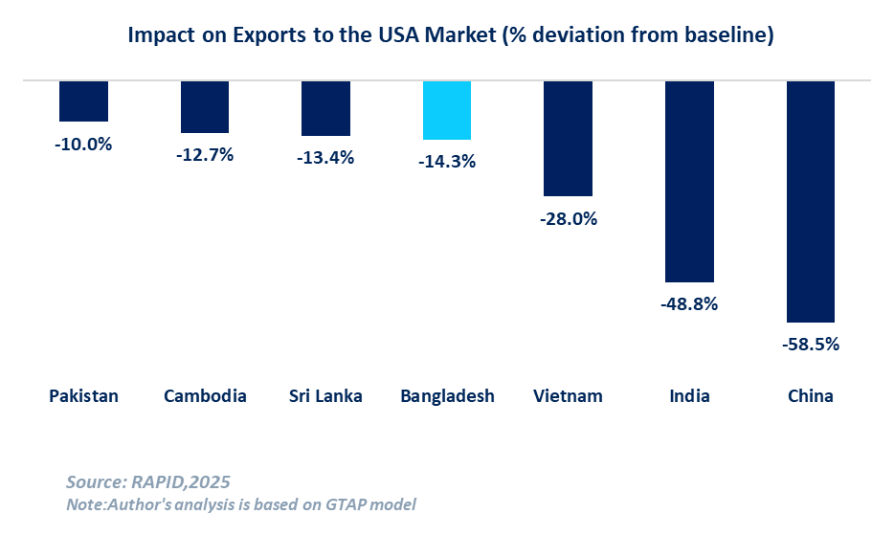

The ripple effect of the US reciprocal tariff is unfolding a complex set of challenges for Bangladesh’s apparel market stability. A recent study by Research and Policy Integration for Development (RAPID) stated that the higher absolute tariff burden means the overall US apparel market is likely to shrink by about 12%, translating to a $10 billion reduction.i

Consequently, simulations project that Bangladesh’s own exports to the US may decline by approximately 14% (around $1.25 billion)ii. The exports to the US have already started to slow down. After August, Bangladesh’s goods exports to the global market fell again in September – by 4.61% to $3.63 billion – driven by a decline in RMG shipments.iii

Furthermore, some U.S. buyers are reportedly requesting Bangladeshi suppliers to absorb 5–7% of the new tariff cost, in some cases even more, squeezing factory margins and threatening order stability.iv

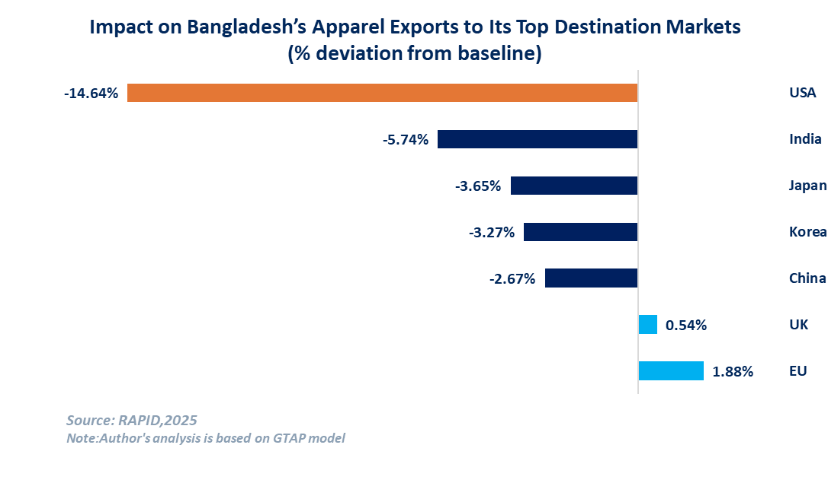

The simulations by RAPID further indicate that Bangladesh’s apparel exports to the European Union (EU) might increase modestly, by about 2%. However, this growth is likely to come with downward pressure on prices and increased competition, as major exporters such as China renew their focus on the EU market.v

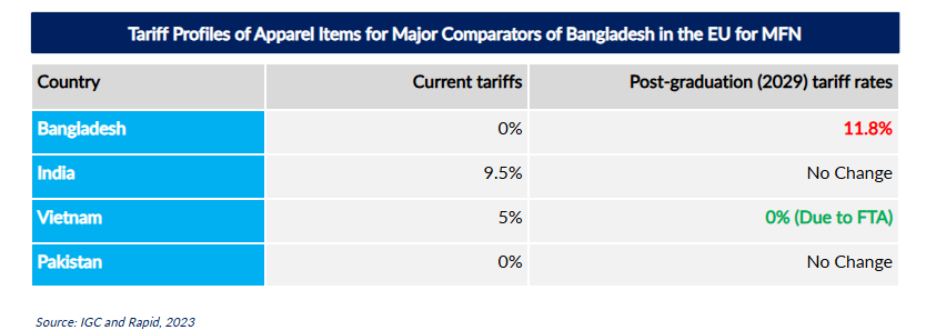

These immediate tariff challenges are compounded by a far more significant, long-term threat: the impending 2026 Least Developed Country (LDC) graduation. As Bangladesh prepares to graduate from LDC status by 2026, its apparel exports face a new era of conditional access. Without integrating sustainable practices in line with EU regulations, Bangladesh risks losing competitiveness in its largest buyer market.

The post-graduation tariff rates would translate to an annual $2.7 billion loss in potential exports for Bangladesh RMG alone losing out $1.08 billion.vi On top of that, limited alignment with the EU Green Deal and its instruments, including the Digital Product Passport that requires disclosure of a garment’s full lifecycle, could further weaken the competitiveness of Bangladeshi RMG manufacturers.

Structural Bottlenecks: The Domestic Productivity Gap

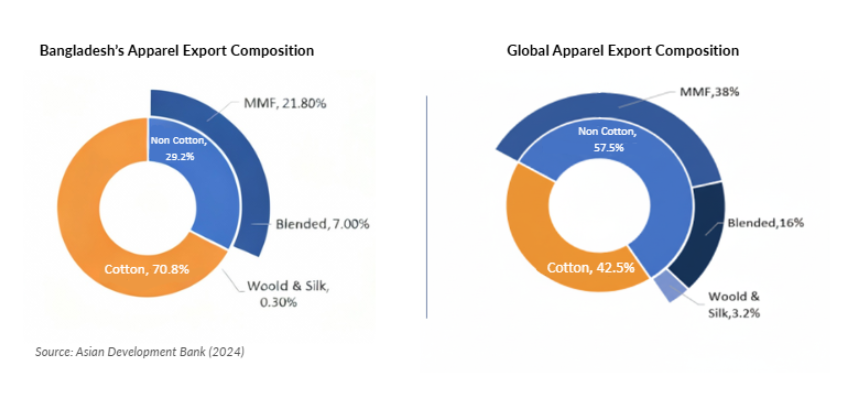

Bangladesh’s apparel industry continues to face deep-rooted structural bottlenecks that constrain its competitiveness. Productivity per worker remains about 30% lower than Vietnam’svii, energy costs are rising, and around 70% of exports still come from a few basic product categoriesviii. Heavy reliance on cotton-based items leaves Bangladesh exposed to demand swings and raw material price volatility.

However, this dependence, paradoxically, has offered some short-term relief. In the recent U.S. tariff negotiations, cotton garments faced lower restrictions than synthetics, the mainstay of Vietnam and China’s exports.

While this short-term relief offers a momentary cushion, it would be unwise to assume such favorable circumstances will persist. Sustaining competitiveness will require more than occasional tariff advantages. Limited progress in automation and digitalization not only jeopardizes long-term cost competitiveness but also presents a severe social risk.

Around 60% of the workforce, mostly women, faces job displacement risks from mechanization, while access to upskilling programs and financial inclusion remains limited.ix These converging challenges, from global market shifts and domestic inefficiency to social displacement risks, clarify the roadmap for reform.

Analytically, four imperatives emerge:

A coordinated reform agenda built on these pillars could help the RMG sector evolve from a cost-based supplier to a trusted sustainability partner in global fashion value chains.

Introducing the Second Phase of Oporajita

In this context, Oporajita Phase II emerges as a strategic platform to drive inclusive and sustainable change within Bangladesh’s apparel ecosystem. Supported by the H&M Foundation, Sweden, and COS, with The Asia Foundation serving as the backbone organization, the initiative advances a collective impact model focused on gender equity, responsible business practices, and collaborative innovation.

By bridging knowledge and action, LightCastle Partners as the key collective impact partner of Oporajita Phase II along with 10 other players, seeks to address the sector’s intertwined challenges, ranging from social inclusion and climate resilience to future-ready skill development.

During the networking session’s opening remarks, Ainee Islam, Program Director at The Asia Foundation, reflected on the initiative’s achievements to date and outlined the priorities guiding this new phase. She emphasized that bringing together eleven partner organizations, will be central to turning these objectives into measurable outcomes for the industry.

Future Outlook of the RMG Industry of Bangladesh

Looking toward 2030, Bangladesh faces both opportunities and perils. According to the Bangladesh Garment Manufacturers and Exporters Association (BGMEA), the industry aims to reach $100 billion in exports and create 6 million jobs by the end of the decade. Yet, achieving this milestone depends on how effectively the sector adapts to shifting global sourcing strategies, rising technological thresholds, and intensifying sustainability requirements.

In recent times, global sourcing is diversifying: Western brands are eager to reduce reliance on any single country, especially with recent tariffs on China and Vietnam. Bangladesh could gain share by moving into higher-value segments, including technical fabrics and by adopting new technologies.

Leading factories such as DBL and Envoy textiles, etc. are pioneering automation adoption by integrating IoT-enabled machinery, AI-infused software, and digital dashboard systems. Yet, while some frontrunners are embracing Industry 4.0 practices, the broader challenge lies in aligning production and regulatory focus with changing global material preferences.

Similarly, as discussed earlier, Bangladesh’s apparel export is heavily concentrated in cotton-based fabrics. This overdependence misaligns the country with the evolving global trend where consumers prefer non-cotton apparel for their sustainability and superior performance. Beyond man-made fibers (MMF), there is also untapped potential in natural alternatives such as silk and wool. These materials are gaining popularity for being both premium and environmentally friendlier than synthetics.

In response to these evolving trade dynamics, the RMG sector of Bangladesh is prioritizing the use of man-made-fiber, the major non-cotton fabric, for production. The country’s MMF exports to the U.S. have grown steadily, their share climbing from 17% in 2013 to roughly 25% in 2023. x

As Amer Salim, Director of Knit Asia, pointed out during the networking session, knowledge gaps among stakeholders and outdated HS (Harmonized System) code classifications continue to hinder product diversification and discourage innovation. Addressing these policy bottlenecks will be key to unlocking higher-value production and market access.

Meanwhile, Bangladesh should try to follow the footsteps of its peer nations. Vietnam and Turkey, for example, enjoy multiple free-trade agreements (EVFTA, RCEPxi, etc.) and have deliberately broadened their product mix, including home textiles and footwear. India, with a fast-growing MMF industry, already exports ~$15 billion of apparel.xii

In contrast, Bangladesh’s RMG exports around $38–40 billion in FY 2024-25 remain heavily weighted toward basic knits and wovens.xiii To sustain momentum, the country must not only expand its product basket but also look beyond traditional markets where competition is intensifying.

The country, therefore, should diversify by moving beyond its top 5 garment types and expand into non-traditional export destinations, where demand is rising and competition is less saturated. These emerging markets offer Bangladesh a chance to reduce overdependence on a few Western buyers and build resilience through product and market diversification.

Decarbonizing the Ready-Made-Garments (RMG) Value Chain

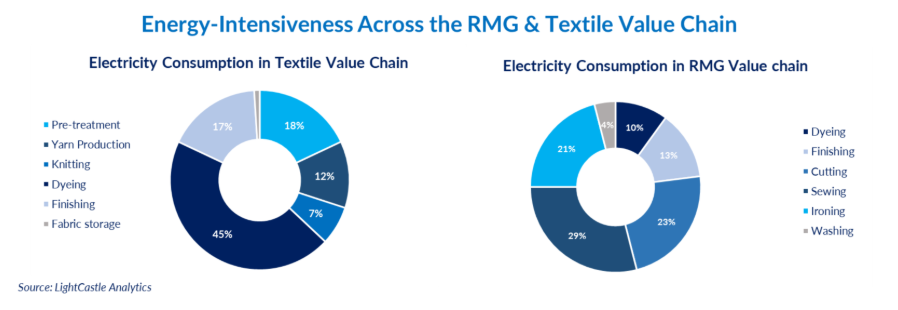

Sustainability is now mission-critical for Bangladesh’s apparel sector. The sector is a major climate hotspot: one assessment notes that the combined RMG and textile industries contribute roughly 15.4% and 12.4% of the nation’s CO₂ emissions, respectively.xiv Much of this comes from electricity-intensive operations, such as spinning, weaving, and finishing, powered by fossil fuels and driven by coal- or gas-fired boilers used in dye houses.

Simultaneously, Bangladesh’s factories still burn more fuel per garment than many peers. A recent analysis found that shifting production from Bangladesh to the EU could cut emissions per unit by ~45%.xv In other words, Bangladesh is lagging in low-carbon manufacturing.

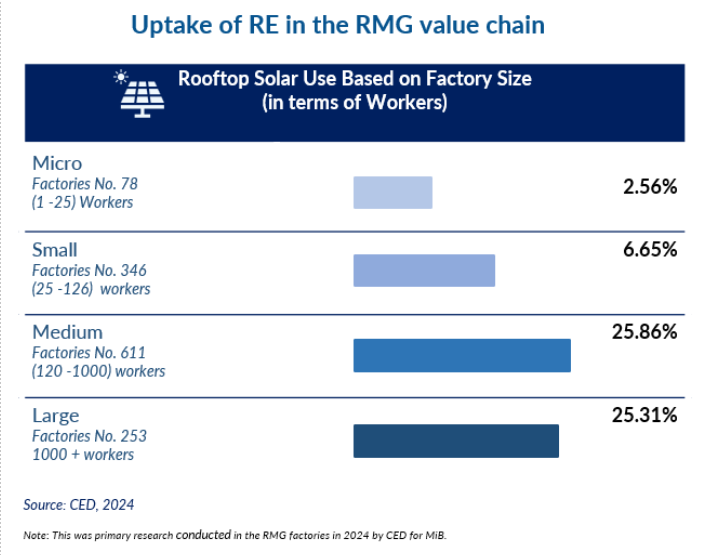

Yet progress is underway. Many leading factories are going green: Bangladesh now hosts over 250 LEED-certified “green” garment factories, the world’s largest such cluster, and it has set ambitious renewable-energy targets, about 20% of power from renewables by 2030. Still, renewables penetration remains modest – less than 5% of the grid capacity, and only a niche, often rooftop solar used in factories.xvi

The slow pace of decarbonization is closely tied to a persistent financing gap. While large manufacturers have begun accessing sustainability-linked loans, small and medium-sized factories continue to face high borrowing costs and limited access to green finance. Despite the existence of programmes such as the Green Transformation Fund and IDCOL’s textile-energy efficiency loans, many businesses remain unaware of or unable to qualify for these instruments.

As Mohammed Jabed Emran, Chief Risk Officer at IDCOL, noted, sustained policy incentives, such as tax relief, blended finance mechanisms, and risk guarantees, will be imperative to expanding the reach of climate finance.

However, recently, the focus has begun to shift toward private-sector driven initiatives. The government’s ratification of the Merchant Power Plant Policy (MPPP) now allows private producers to sell electricity directly to businesses and consumers through the national grid. This marks a significant change from the earlier Independent Power Producer (IPP) model, where the government acted as the sole buyer of power.

Under the MPPP framework, Bangladesh has launched its first Corporate Power Purchase Agreement (CPPA) through a partnership between H&M, PRAN, and the IFC.xvii The pilot project aims to accelerate the country’s renewable energy transition and enhance the RMG sector’s competitiveness in markets that increasingly prioritize low-carbon production.

Integration of Just Transition in the RMG Sector

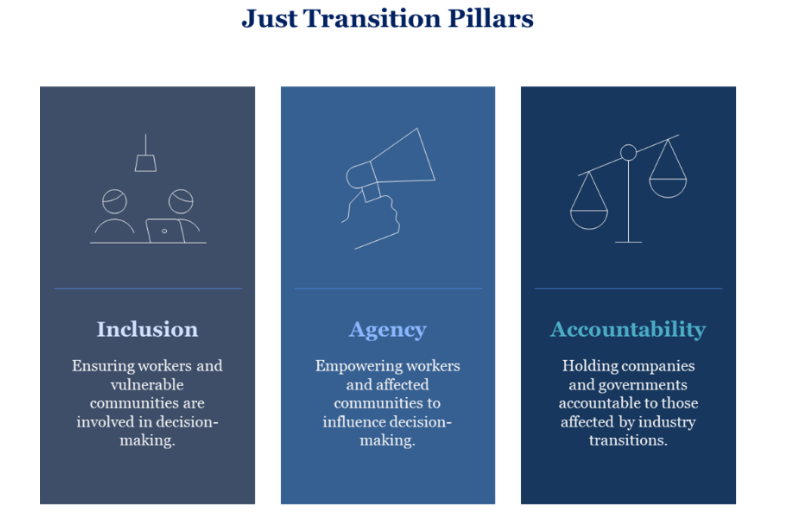

As the discussion on greening the RMG value chain unfolded, attention turned to another crucial pillar of worker wellbeing, the integration of Just Transition principles. The conversation underscored the need to balance climate goals with social justice to ensure that no one is left behind in the transition.

To explore the intricacies of this theme, Saif Moinul Islam, Senior Programme Officer at the International Labour Organisation (ILO), emphasised the urgency of integrating Just Transition principles into the apparel industry. Although the sector has made commendable strides in improving workplace safety and strengthening worker welfare, there remain significant opportunities to mainstream the broader components of Just Transition across factories nationwide.

A Just Transition in the RMG sector involves more than adopting green technologies; it requires placing worker inclusion, agency, and accountability at the center of sustainability strategies. This means ensuring decent working conditions, fostering participatory decision-making, and equipping workers with the skills and protections needed to adapt to evolving production processes.

Particular emphasis was placed on the wellbeing of women workers, who form the backbone of the industry. Enhancing workplace safety standards through better ventilation, improved roofing materials, reduced crowding, heat control from machinery, and active cooling systems. Investments in ‘green’ factory infrastructure that address these factors can create safer, more productive environments for workers.

Evidence shows that if at least half of Bangladesh’s RMG industry manufacturers invest in cooling practices and temperature reduction, productivity could rise by 2.66% annually by 2030. Moreover, such measures could help the industry avoid a projected loss of 28.44% in export earnings ($7.58 billion) and 73,372 jobs that might otherwise be lost due to heat stress. Pushing the share of green factories above 50% could yield even greater productivity and economic gains by 2050, positioning Bangladesh’s RMG sector as a global leader in climate-resilient and worker-centered industrial transformation.xviii

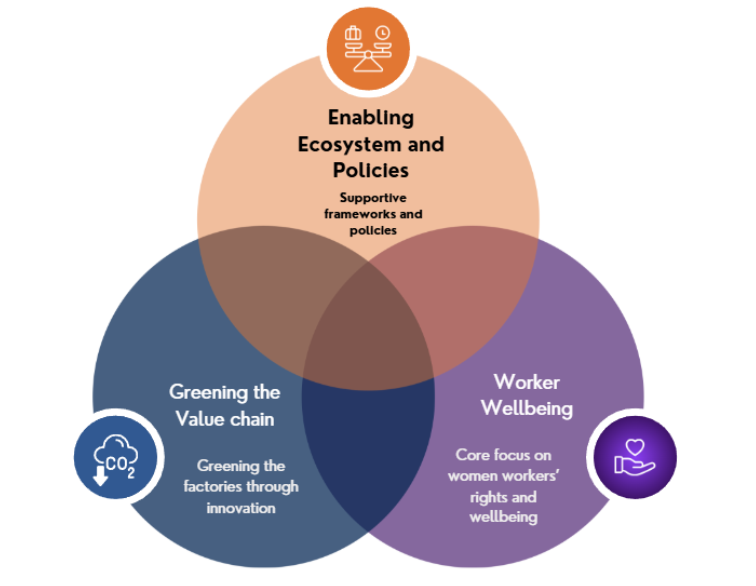

Weaving the Threads Together — Oporajita’s Integrated Approach

Building on these discussions, the discourse reaffirmed that through the Oporajita initiative, the apparel sector holds the potential to drive systemic transformation by embedding Just Transition principles and advancing decarbonization across the value chain. However, for this transformation to be sustainable beyond the project’s lifecycle, change must take root at every level of the ecosystem, from factory floors to institutional frameworks.

Figure: Oporajita: Towards a Green and Just Transformation in the RMG Sector

Such an approach ensures that all ecosystem actors, including manufacturers, policymakers, financiers, and development partners, play an active role in fostering behavioral and structural shifts that promote worker wellbeing and support the greening of Bangladesh’s apparel sector.

Concluding the Networking Session

The closing segment of the session led to the launch of an in-house publication developed by the project team, a policy brief on Corporate Power Purchase Agreements (CPPA). The publication highlighted the transformative potential of CPPAs in unlocking private sector investments to accelerate renewable energy adoption across Bangladesh’s industrial landscape.

It further outlined the regulatory gaps and strategic entry points necessary for private sector engagement, particularly within the RMG industry, to foster a cleaner and more resilient energy transition.

At the end, Faisal Bin Seraj, Country Representative of The Asia Foundation, emphasized that advancing sustainability in the RMG sector demands a shared responsibility, where brands, government, and workers collectively shape a future that balances economic growth with social equity. He reiterated that the pathway to a resilient and sustainable apparel industry lies in joint ownership of change, ensuring that the sector continues to thrive while safeguarding the wellbeing and dignity of its workforce.

Author:

Safin Sadique, a Trainee Consultant, and Sadia Karim, a Business Consultant at LightCastle Partners, have co-authored the write-up. For further clarifications, contact us here: [email protected]