LightCastle Analytics Wing

LightCastle Analytics Wing

Exploring Opportunities in Market and Product-Line Diversification in Bangladesh’s RMG Industry

Originally published on the LightCastle Partners website.

Over the decades, Bangladesh has witnessed a notable surge in its export production, particularly in the realm of ready-made garments (RMG). The share of global clothing exports from Bangladesh has more than tripled, rising from 2.5% in 2005 to 7.9% in 2022 [1]. Emerging from an economy marked by severe poverty and recurrent famines, Bangladesh has transformed into the second-largest RMG manufacturing hub worldwide with a market share of USD 47 billion in 2022-23, trailing only behind China [2]. The period spanning from 2000 to 2022 witnessed a significant rise in the value added by the RMG sector in Bangladesh nearly doubling as a proportion of the GDP, escalating from 11% to 22% [3].

![Figure 1: Total apparel export in Billion USD [4]](https://lightcastlepartners.com/wp-content/uploads/2024/05/image-1.png)

Considering the close competition among Vietnam, Turkey, India, and others in the RMG sector, diversification emerges as a strategic imperative to safeguard Bangladesh’s position in the apparel export market.

Focusing on the close competition between Bangladesh and Vietnam, among others, the leading factor is the diversification of the product lines. Vietnam’s export portfolio is notably diversified, with 63.1% of its products made of both Man-Made Fiber (MMF) and cotton-based products. These include women’s knit shirts, blouses, women’s trousers, men’s knit shirts, dresses, and women’s coats, constituting the top 10 product categories exported to the USA.

In contrast, Bangladesh’s garment exports are more concentrated, with 79% of the total exports limited to just 5 basic product lines, including, trousers, t-shirts, sweaters, shirts, and jackets [5].

Bolstering Backward Linkage

Delving further into the RMG export product line, knitwear stands out as a dominant force, surpassing its target by 5.42 % for the quarter of Fiscal Year 2024, as noted in the Quarterly Review on Ready-Made Garments. This accomplishment can be attributed in part to the robust backward linkage within Bangladesh’s knitwear industry, where a substantial portion of the knitwear yarn is locally produced.

This reduced dependence on imported knit yarn, has played a pivotal role in bolstering Bangladesh’s export revenue from knitwear in the RMG sector [6]. On the other hand, woven garment suppliers, are in a disadvantaged position due to a lack of local supply of woven fabric [7].

![Figure 2: Trends of Export Earnings from Woven and Knitwear [8]](https://lightcastlepartners.com/wp-content/uploads/2024/05/image-2.png)

The trend of the data reflects that the earnings from Knitwear production have been gradually increasing from the year 2020 from USD 13,908 million to USD 25,738 million, indicating the need for Bangladesh to invest more in its locally produced raw materials to reduce the production cost.

There is also hope for potential growth in this segment as international clothing retailers and brands have shortened lead times to 45-60 days, compared to the previous 90-120 days. This adjustment, driven by heightened competition, has also prompted retailers and brands to aim for 12 selling seasons annually, up from eight [9].

However, the upcoming graduation to middle-income countries from a Least Developed Country (LDC) for Bangladesh poses significant challenges for its RMG sector. This transition may lead to a substantial shift in the sourcing patterns of global apparel buyers.

Notably, in 2022 around 73% of Bangladesh’s RMG exports benefit from duty-free market access as an LDC, a privilege that may change post-graduation. Furthermore, the discontinuation of government subsidy programs in the post-LDC era could significantly impact export competitiveness, particularly for low-cost products [10].

The cessation of these subsidies would eliminate the competitive advantage gained from price advantages, thereby threatening the industry’s overall competitiveness. At the same time, the evolving consumer demand, for clothing preferences, and buyer countries preferring nearshoring exacerbates the situation.

To address these hurdles Bangladesh needs to intensify efforts towards export diversification. Leveraging its expertise in RMG, Bangladesh can expand its product line and explore new export destinations to mitigate the risks associated with price volatility.

Diversification in the RMG Export Basket

Bangladesh has a comparative advantage in its competitive labor cost, but this advantage is gradually diminishing as other players enter the market with better trade agreements or location advantages.

As the market for basic goods becomes increasingly saturated, Bangladesh can adapt to sustain its position. Exploring additional export opportunities within the global apparel market through intra-RMG diversification could be a viable strategy for Bangladesh to navigate these shifting dynamics.

![Figure 3: Top Five Apparel Export from Bangladesh [11]](https://lightcastlepartners.com/wp-content/uploads/2024/05/image-3.png)

Currently, Bangladesh is exporting low-cost items to the world whereas its peer nation, Vietnam has expanded its production line to add high-value RMG products. The heavy reliance on exporting low-cost items poses a potential obstacle to sustaining its market share in the global RMG industry. Particularly following its graduation from the LDC status, Bangladesh may face increased difficulty in boosting its RMG export rates with these low-cost items.

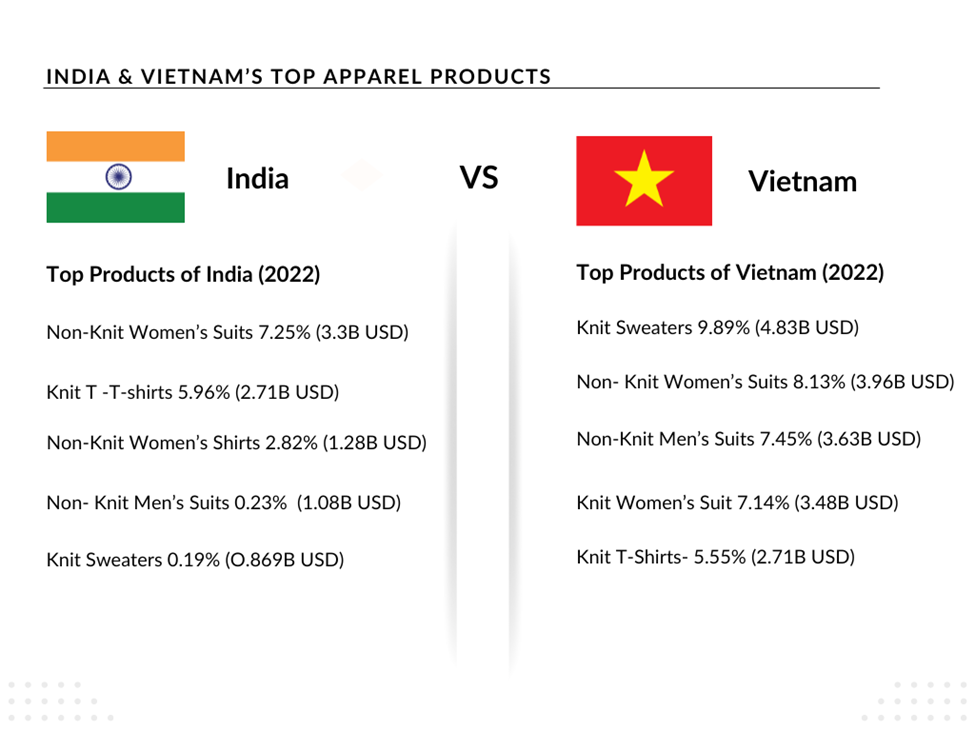

The European Union, for instance, is transitioning towards high-value-added products, signaling a shift in demand. Countries like Vietnam and India are positioned to meet this demand with competitive prices for high-value-added RMG products, potentially diverting market attention away from Bangladesh.

The new Export Policy for 2021-24 includes the need for additional high-value products such as denim goods, men’s and women’s blazers, suits, water-proof garments, leather jackets, and MMF products to retain its position in the RMG global export market [14].

Bangladesh currently utilizes 11% of MMF in its RMG basket in the EU market. Hence, to continue enjoying duty preferences for another decade, it is imperative to diversify the RMG export from cotton based items to MMF based items in the global market share [15].

![Figure 5: Percentage in Price Growth of Bangladesh for Top 5 Apparel items made of Cotton Fabric [16]](https://lightcastlepartners.com/wp-content/uploads/2024/05/image-5.png)

The data depicts a notable decline in the concentration of cotton-made products, except for knitted trousers in the USA during 2020. This trend raises concerns regarding Bangladesh’s vulnerability to shifts in market dynamics, particularly following its anticipated graduation from LDC status in 2026.

As the global market trends evolve towards greater demand for MMF production, the diminishing share of cotton fiber apparel, plummeting from 75% to 25% in recent years, signifies a decrease in demand for cotton within the industry [17].

This transition reflects changing buyer countries’ preferences and underscores a fundamental transformation in the industry’s demand structure. Diversifying its RMG export portfolio beyond cotton fabric to include a variety of products such as MMF will enable Bangladesh to maintain its competitive edge in existing global markets, aligning with shifting demand trends. Introducing high-value-added products further strengthens Bangladesh’s position by facilitating negotiations for better pricing in its RMG exports.

By expanding its RMG export basket, Bangladesh taps into segments where it possesses a comparative advantage, leveraging factors like competitive labor cost and strengthening its backward linkage production processes. This strategic shift not only enables Bangladesh to differentiate its offerings in the international market but also helps mitigate risks associated with market saturation and declining demand for low-cost items. Furthermore, diversifying the production line allows Bangladesh to cater to a broader range of destination countries’ preferences.

Traditional vs Non-Traditional Countries

For Bangladesh to bolster its competitiveness in RMG exports, it is essential to explore new export destinations. Simply diversifying the RMG export basket isn’t sufficient to enhance Bangladesh’s global apparel image or attract Foreign Direct Investment (FDI). It is quite imperative for Bangladesh to venture into new market destinations to help mitigate the risk associated with relying heavily on a few destination countries for apparel exports.

Bangladesh’s heavy reliance on traditional export destinations like the EU, USA, and UK entails an opportunity cost for the RMG export sector. With unwavering competition in these markets from countries like Vietnam, Myanmar, Cambodia, and Turkey, as well as some African and Latin American nations, there is a risk of missing out on potential growth opportunities in non-traditional regions experiencing a surge in garment demand [18]. This dependence on traditional markets highlights the need for Bangladesh to diversify its export destinations strategically to prevent any kind of economic downturn from other regions.

![Figure 6: Bangladesh Top 5 Traditional vs Non-traditional Export Countries [1]](https://lightcastlepartners.com/wp-content/uploads/2024/05/WhatsApp-Image-2024-05-28-at-18.08.28_0f03c0bc.jpg)

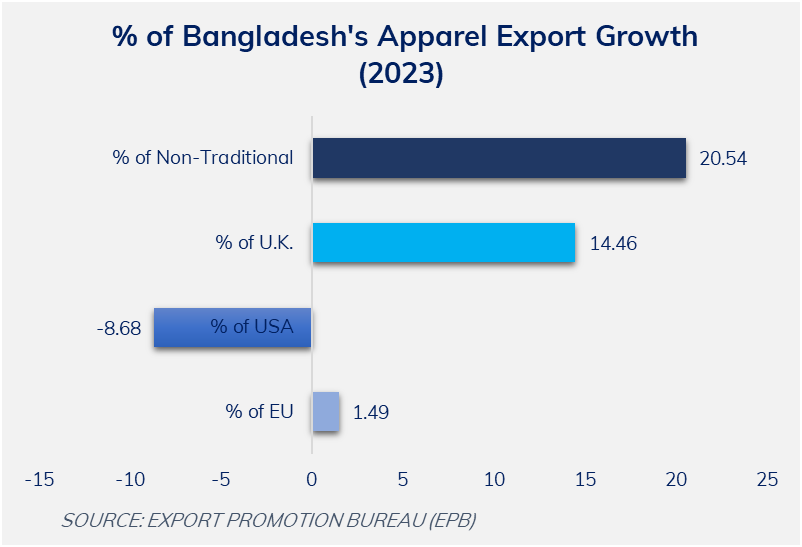

In comparison to 2022, Bangladesh experienced higher export value growth in non-traditional countries than in traditional destinations as per the Export Promotion Bureau (EPB) data. While the USA saw a decline in growth percentage at -8.68, non-traditional countries exhibited a significant increase in export growth percentage, reaching 20.54 compared to the EU [19].

Among these non-traditional countries, Japan stood out with the highest growth value, amounting to USD 1.68 billion in 2023. Nonetheless, other destinations within non-traditional countries also contributed positively to Bangladesh’s RMG export growth, resulting in a notable 20.54% increase in growth rate compared to the previous year [18].

Looking at the growth trajectory for Bangladesh’s RMG exports in non-traditional countries, it can be interpreted that Bangladesh is trying to venture into new markets. This is to be able to leverage its comparative advantage in garment production and cater to new customer segments with distinct tastes and preferences. This diversification strategy offers a crucial path forward, especially considering the challenges faced in expanding the current product base.

Non-traditional markets, with their lower competition, offer Bangladeshi manufacturers a promising opportunity to establish a foothold and capture market. This strategic shift towards diversification can ultimately lead to a broader customer base and a more robust product portfolio for the RMG sector. On the other hand, competitors are trying to expand their export production in traditional markets such as the USA and EU.

Global Landscape: Lessons from Competitors

Vietnam

In comparing Vietnam’s apparel sector with Bangladesh’s, Vietnam emerges ahead in terms of product line expansion, bolstered by a robust backward linkage. Vietnam’s industry showcases a diverse array of high-value-added products, including high-quality blazers, woven formal shirts and trousers, and outerwear tailored for colder climates [20]. Their diversified export basket would give them an edge in the case of a price war with Bangladesh’s narrow RMG export basket.

Additionally, Vietnam is renowned for producing large quantities of expensive sportswear. Positioned within the buyer-driven value chain (BDVC) that dominates the apparel market, Vietnam leverages its focus on high-value, non-mass-produced, fast-fashion non-cotton items to capitalize on better prospects in the global export market [14].

![Figure 8: Vietnam Top Apparel Export Market [21]](https://lightcastlepartners.com/wp-content/uploads/2024/05/image-8.png)

Vietnam has also diversified its export destination countries between traditional and non-traditional countries to expand the customer base, where the USA is the top destination among the traditional countries and Japan is among the non-traditional countries.

Vietnam’s robust performance in the RMG sector stands to gain further momentum with the finalization of its Free Trade Agreement (FTA) with the European Union. This agreement grants Vietnam zero-duty access to over 50 percent of the global market, reflecting its active participation in various free trade agreements.

A few of the examples include the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), EU-Vietnam FTA (EVFTA), and RCEP. Additionally, Vietnam has forged bilateral free trade agreements with countries like Japan, Australia, and New Zealand, establishing a strategic business network across Western and European regions to reinforce their destination regions for exports. In contrast, Bangladesh lags significantly behind in this regard, given the upcoming regulations from the EU for the LDC graduation [16].

Turkey

Turkey strategically leverages its advantageous geographical position to secure access to the EU market, enhancing its export prospects. Similar to Bangladesh’s strategy, Turkey also aims to diversify its destination market base for RMG exports by pursuing new FTAs with African countries like Djibouti and the Democratic Republic of Congo, as well as South American nations such as Peru and Colombia. While Turkey benefits from existing free trade agreements with European countries, it recognizes the importance of seeking preferential market access in other regions to expand its RMG export market base beyond the EU [22].

Way Forward: Beyond Borders

Navigating Footsteps of the Competitor Countries: Bangladesh’s export destinations currently lack significant diversity, posing a challenge to long-term export sustainability. Reliance on traditional markets like the EU, US, and U.K. presents a long-term sustainability risk. These established players are increasingly adopting automation, fast fashion trends, and leveraging economies of scale, making them potentially competitive threats with lower prices. To mitigate this risk, following the model of Vietnam and Turkey becomes crucial.

These nations secured favorable trade access through FTAs and bilateral deals, diversifying their export landscape. This strategic move becomes even more important as Bangladesh’s graduation LDC status in 2026 looms. The potential loss of Generalized System of Preferences (GSP) benefits and the uncertain future of the GSP+ facility necessitate securing alternative markets through proactive trade agreements. Diversifying trade destinations is thus imperative for Bangladesh to navigate evolving market dynamics and sustain its export competitiveness in the long run.

Expanding Bangladesh’s Export Footprint: European and American brands are increasingly embracing near-shoring, a practice of establishing production facilities in geographically closer locations. This rise of near-shoring by major brands poses increased competition for Bangladesh in the RMG sector, particularly from countries like Turkey, and Eastern Europe, which enjoy geographical proximity to European markets. This competition presents a potential threat to Bangladesh’s share of the European and American RMG markets if it fails to adapt to the changing landscape.

This dependence on a limited set of markets exposes Bangladesh’s RMG sector to the risk of sudden economic downturns in those regions, potentially leading to a fluctuation in demand due to changing trends in the fashion hubs. In response to these challenges, Bangladesh can adopt strategic measures to maintain its competitiveness.

One approach is to focus on non-traditional markets like Japan, India, South Korea, and countries within the proximity. Promptly to changing trends and customer demands. An incentive for Bangladesh is in the ongoing discussion of signing an FTA with Japan in order to boost trade and investment in the apparel export sector.

By situating production facilities closer to their markets and signing the FTA such as with Japan, the RMG sectors in Bangladesh can streamline supply chains and enhance agility in meeting consumer needs. It will also help the RMG sector diversify to sell more units at a potentially better price, increasing the marginal productivity of the entire apparel sector. Where with a wider range of countries to export to, Bangladesh can utilize its existing production capacity more effectively, spreading its fixed costs over a larger output, ultimately leading to a higher return on investment and increased profitability.

Hence, by diversifying its customer base, Bangladesh can spread its production volume across multiple markets, reducing its reliance on any single market and mitigating the risks associated with sudden economic downturns.

Strategic Imperative for Apparel Export Basket: If Bangladesh continues to focus solely on basic garments, it risks losing its market share in the EU as demand for these products declines along with experiencing declining marginal revenue as demand. This scenario goes against the economic principle of maximizing profit, which occurs when marginal revenue exceeds marginal cost.

In the pursuit of maximizing profit margins and maintaining competitiveness in the apparel export market, policymakers have stressed the importance of revisiting the RMG market strategy to introduce high-value products that can attract foreign direct investment (FDIs). This strategic move towards product and market diversification aims to strengthen Bangladesh’s RMG brand presence globally, thereby attracting more foreign investors to engage with the sector [18].

Similarly, Faruque Hassan, former president of the Bangladesh Garment Manufacturers and Exporters Association (BGMEA) highlighted the importance of incorporating local heritage fashion alongside non-cotton fabric products in response to growing interest in fashion fusion among international consumers. Recognizing the value of high-value addition.

“International retailers and brands are willing to pay premium prices for such garments, reflecting a shift in consumer preferences towards relatively more expensive items”.

By transitioning towards high-value, Bangladesh can access a new and potentially more lucrative market. Producing high-value garments not only enhances Bangladesh’s image from a low-cost producer to a manufacturer of high-quality and innovative apparel but also attracts new customers and solidifies its position in the global RMG market. This shift allows Bangladesh to move beyond economies of scale and potentially achieve economies of scope.

Moreover, Bangladesh can move beyond producing basic cotton T-shirts to manufacturing more technical garments like performance wear for athletes or weatherproof jackets and fusion fashion, leveraging its existing resources and expertise to gain cost advantages by producing a variety of related products.

Innovating in materials presents a strategic avenue for Bangladesh to gain a competitive edge in the existing market. Investing in research and development of sustainable materials such as organic cotton or recycled polyester. This aligns with the growing consumer demand for eco-friendly products.

Author:

This article was authored by Sadia Karim, a Business Analyst at LightCastle Partners. Advisory and editorial support was provided by Samiha Anwar, Business Consultant at LightCastle Partners. For further clarifications, contact here: [email protected].

References:

- BGMEA DAILY DIGEST, 2023

- Export Promotion Bureau (EPB)

- Bangladesh needs to diversify its export markets and step up investment, says new report | OCED, 2022

- Statista, 2022

- Industrial Analytics Platform

- Country Profile Vietnam

- World’s Biggest Exporters of Clothes, Statista

- We need to step up our RMG game | Dhaka Tribune

- Knitwear’s export performance stronger than woven, The Daily Star, 2023

- How did Bangladesh surpass China in EU knitwear exports? | The Financial Express

- Bangladesh -European Community | EU

- Quarterly Review on Ready-Made Garments, July-September of FY’24

- Country Profile India and Vietnam

- Bangladesh’s LDC Graduation: Challenges and Opportunities for the RMG industry – TBS

- Export Performance | BGMEA

- Bangladesh needs a clear strategy for GSP+ |The Daily Star

- Export diversification still in slow lane | Daily Star

- Bangladesh losing more than 40% export potential in EU: Study | TBS

- Weekly Trade Digest | BGMEA

- The 4th Industrial Revolution: How It Is Changing the Ready-Made Garments Sector of Bangladesh | LightCastle Partners

- Intra-RMG Diversification: The next Frontier | CPD

- Apparel exports surge 20.54% to non-traditional markets in 2023

- Readymade Garments Sector Landscape: Vietnam vs Bangladesh

- UNIDO Comtrade https://comtrade.un.org/labs/data-explorer/

- The Fashion War that Matters: Assessing Bangladesh RMG’s International Competitiveness | LightCastle Partners

- RMG export in February one of the highest

- Nearshoring: A Megatrend Reshaping Global Supply Chains

- BGMEA turning to heritage fashion items to meet export target