GET IN TOUCH

- Please wait...

Global startup funding recovered in 2025, rising to USD 469 Bn, up from approximately USD 320 Bn in 2024, marking a year-on-year increase of about 47 percent. The rebound was primarily driven by late-stage transactions and a small number of large-scale deals, while early-stage activity remained selective across most markets.

Asia followed a more muted trajectory. Total startup funding in the region increased from around USD 50 Bn in 2024 to USD 53 Bn in 2025, reflecting a modest year-on-year growth of roughly 6 percent. Capital deployment across Asian markets remained cautious, with investors prioritising scale, profitability pathways, and strategic relevance.

Bangladesh’s startup ecosystem evolved within this broader global and regional context. While overall funding conditions improved, investor behaviour continued to favour fewer, larger, and more defensible transactions rather than broad-based early-stage expansion.

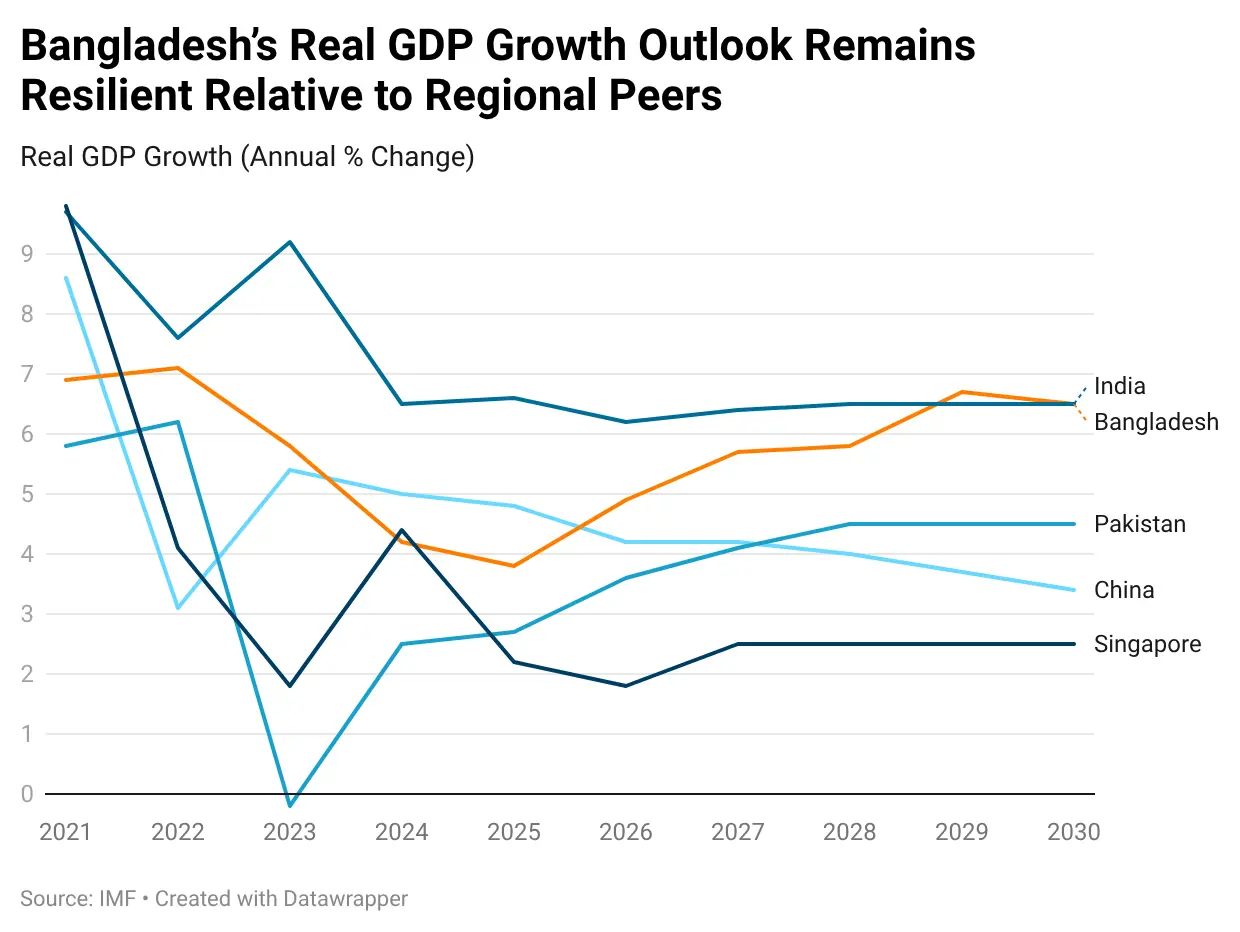

Bangladesh’s macroeconomic fundamentals continue to point toward long-term growth potential. Real GDP growth remains positive relative to many regional peers, and the underlying demand drivers for technology-enabled businesses remain intact. However, the report highlights a persistent structural gap: startup investment as a share of GDP remains low, estimated at around 0.03 percent.

This gap suggests that while the economy can support a deeper startup ecosystem, capital formation has not yet scaled proportionately. Addressing this gap is less about short-term sentiment and more about building repeatable investment mechanisms, stronger deal pipelines, and consistent institutional execution.

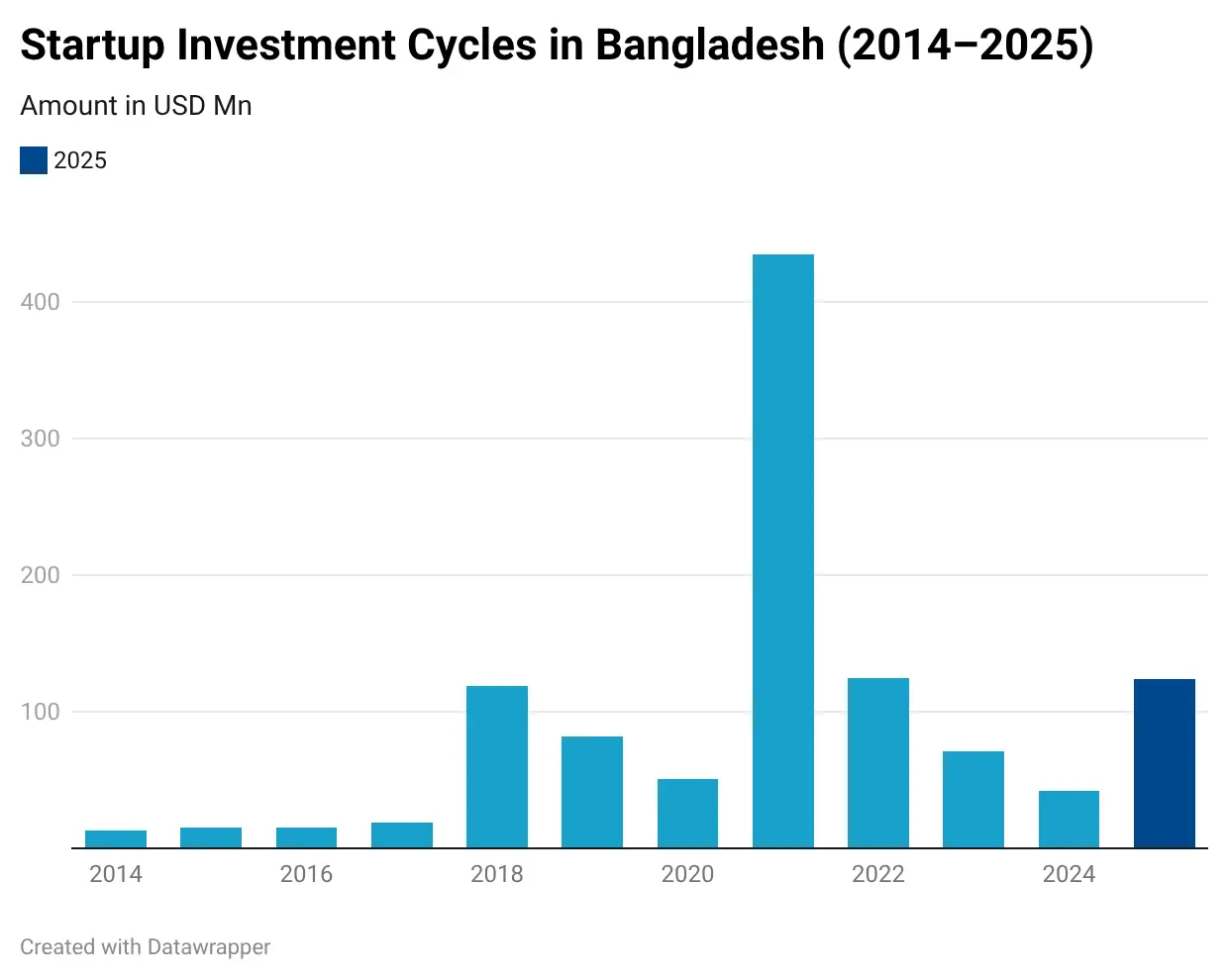

Over the past decade, Bangladesh’s startup ecosystem has moved through multiple cycles. Early years were defined by ecosystem building and small ticket sizes, followed by increased institutional participation and periodic surges driven by a handful of large transactions. The Covid period introduced exceptional capital inflows, which were later followed by a global reset as risk appetite tightened.

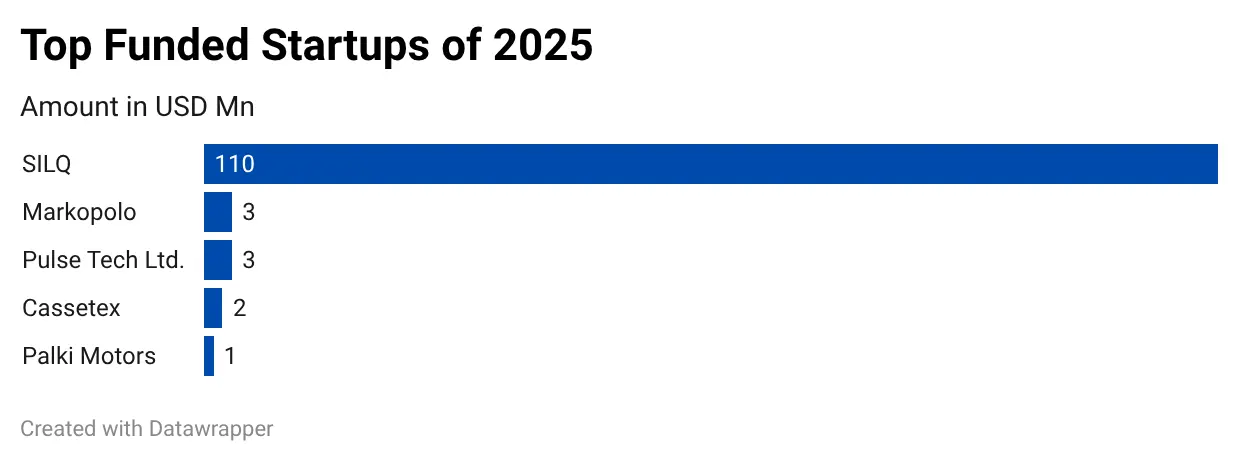

Within this historical arc, 2025 stands out as a strategic transition year. Total startup funding reached USD 124 Mn across 12 deals, compared to USD 42 Mn across 41 deals in 2024. The increase, however, was largely driven by a single transaction: the USD 110 Mn investment associated with the ShopUp–Sary merger that formed SILQ Group. Excluding this deal, funding activity remained modest, reinforcing the view that the year was defined more by concentration than by broad recovery.

Investment activity in 2025 reflected a clear preference for fewer, larger, and later-stage transactions. Nearly all funding was directed toward late-stage and strategic deals, with the top three transactions accounting for about 95 percent of total capital deployed.

Round-wise activity illustrates this shift. M&A and late-stage rounds dominated funding volumes, while early-stage investments continued at a slower pace. Average ticket sizes increased across stages, particularly at the late stage, reflecting investor focus on scale-ready businesses rather than portfolio-style experimentation.

Investor composition further reinforced this pattern. Venture capital firms remained the primary source of funding, accounting for the vast majority of capital deployed. Other channels such as angels, accelerators, and corporate investors played a comparatively smaller role, particularly at scale.

Sector-wise, Financial Services accounted for 89 percent of total funding, again largely due to the SILQ transaction. Other sectors such as software and enterprise solutions, ecommerce, energy and climate, and education remained active but attracted significantly smaller volumes. The distribution underscores how, in tighter capital environments, investors gravitate toward sectors with clearer monetisation pathways and regional scalability.

The reliance on global capital also deepened in 2025. Approximately 99 percent of total funding originated from global investors, while local investor participation declined both in value and deal count compared to the previous year. Within global flows, Gulf-based investors emerged as a more visible source of capital, indicating gradual diversification of international interest beyond traditional markets.

The patterns observed in 2025 point to a set of recurring structural priorities rather than short-term fixes.

While 2025 was shaped by concentration, it also marked a period of renewed engagement across the ecosystem. Strategic transactions, continued global investor interest, and gradual policy progress signal that the foundational pieces for growth remain in place.

The year should be read not as a full recovery, but as a transition toward a more deliberate phase of ecosystem development. If capital formation broadens, execution improves, and participation deepens across stages, future growth is more likely to be sustained rather than episodic.

|

If you are interested to learn more

|

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights