GET IN TOUCH

- Please wait...

Few maritime corridors carry greater systemic importance to the global energy system than the Strait of Hormuz. The narrow passage between Oman and Iran functions as the primary transit route for hydrocarbons flowing from the Persian Gulf to global markets.

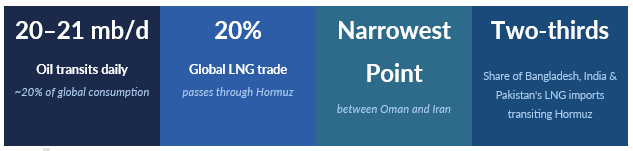

Approximately 20–21 million barrels of petroleum liquids pass through the Strait each day equivalent to nearly one-fifth of global oil consumption, making it the most critical oil transit chokepoint in the world.1 The waterway also carries a substantial share of global liquefied natural gas (LNG) exports, including shipments from Qatar, one of the world’s largest LNG exporters.2

For energy-importing economies across Asia, the Strait’s continued accessibility is often treated as a structural constant. Yet geopolitical tensions in the Gulf have periodically raised the specter of disruption. A sustained closure of Hormuz, even if temporary, would trigger cascading repercussions across global shipping, insurance markets, and energy supply chains.

For Bangladesh, whose gas-fired power sector increasingly relies on imported LNG, such a disruption would expose profound vulnerabilities in the country’s energy architecture.

This article examines a scenario in which maritime traffic through the Strait of Hormuz becomes severely disrupted, assessing how such an event could potentially affect global energy flows and Bangladesh’s energy security.

The Strait of Hormuz is widely regarded as the most strategically significant energy transit route in the world. According to the U.S. Energy Information Administration (EIA), it handles a large share of LNG exports from Qatar and the United Arab Emirates alongside its dominant oil flows.

Unlike pipeline systems, seaborne energy trade depends on a combination of physical access, maritime security, and financial infrastructure. Even limited disruptions – whether from geopolitical escalation, naval blockades, or mining operations – can rapidly constrain tanker movements. Historically, energy markets have proven to be highly sensitive to such risks. During previous periods of tension in the Gulf, insurance premiums for transiting tankers had spiked sharply and shipping companies have had to temporarily divert vessels.3

The functioning of global shipping is underpinned by a financial infrastructure that is often invisible to policymakers. Nearly 90% of the world’s merchant fleet is insured through the International Group of Protection and Indemnity (P&I) Clubs, headquartered largely in Europe. 4These mutual insurers provide coverage for liabilities ranging from environmental damage to cargo losses.

In high-risk environments, the withdrawal of war-risk insurance can effectively halt commercial shipping. Without P&I cover, shipowners face potentially unlimited financial liability for vessel losses, making most voyages commercially unviable. Conflicts in the Middle East and the Black Sea have demonstrated how rapidly insurers reclassify maritime zones as high-risk ones, triggering immediate spikes in insurance premiums and prompting shipowners to suspend operations.

For energy-importing nations such as Bangladesh, this represents a critical but often overlooked vulnerability. Even if supply contracts remain valid, cargoes may not be delivered if insurers or reinsurers deem transit routes too perilous.

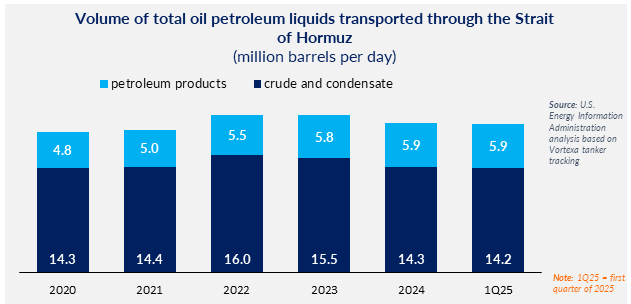

Oil markets are no longer merely “pricing tension”; they are pricing the non-trivial risk of a physical supply shock through the Strait of Hormuz. The U.S. EIA notes that around 20 million barrels per day of crude oil and petroleum products transited Hormuz in 2024, while around 20 percent of global LNG trade also passed through it,5 underscoring why even the threat of disruption provoke outsized price reactions.

As the conflict between Iran, Israel, and the United States deepened, markets reacted with alacrity. Brent crude rose above US$108 per barrel on 8 March 2026 and reached roughly US$119.5 per barrel on 9 March, hitting its highest level since mid-2022.6 The rapid escalation reveals how geopolitical risk can swiftly reintroduce volatility into energy markets, elevating inflation expectations and sending ripples through global financial systems.

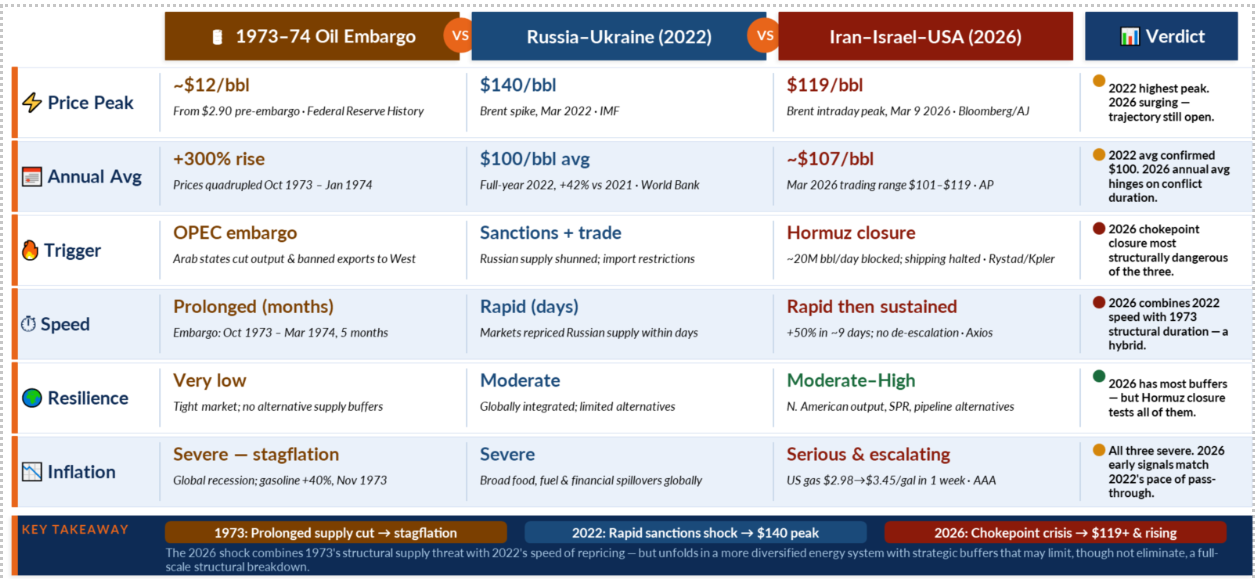

To understand the magnitude and potential trajectory of this shock, it is useful to place the current episode in historical perspective, particularly by comparing it with earlier energy crises such as the 1970s oil embargo and the price spike following the 2022 Russia–Ukraine war.

While all three instances were driven by geopolitical conflict, the structure of the shock has differed in each case. The 1973–74 embargo was a deeper and more prolonged supply crisis, unfolding at a time when the global oil market was already tight and far less diversified.7 In contrast, the 2022 Russia–Ukraine war triggered a rapid repricing of supply insecurity, with Brent briefly touching US$140 per barrel as sanctions, trade disruptions, and fears over Russian exports rattled markets. 8

Today’s crisis echoes of both. It evokes the same fear of disruption from an important region that defined the 1970s, while also producing the swift market reaction seen in 2022. Yet the energy system has fundamentally evolved. Global oil supply is more diversified, and new production centers have emerged over the past decade.

These structural shifts suggest that while markets are confronting a serious geopolitical shock, the global system now possesses greater capacity to absorb disruptions. The resilience of this system will depend largely on how effectively North American production and alternative export routes can act as buffers, which may help prevent the present shock from evolving into a prolonged embargo-style crisis, even if volatility persists.

Bangladesh’s power sector has undergone a rapid transition over the past decade. Domestic gas production, the longtime backbone of the country’s electricity generation, has stagnated as major gas fields mature. To bridge the supply gap, the government began importing LNG in 2018 through floating storage and regasification units (FSRUs) at Moheshkhali.9

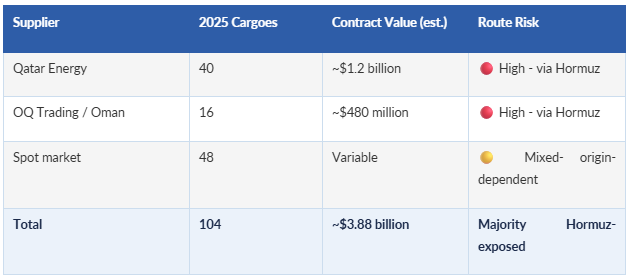

Since then, LNG has become an increasingly important and structurally vital component of Bangladesh’s energy mix. In 2025, Bangladesh spent approximately $3.88 billion to import 109 LNG cargoes, against $3.02 billion for 86 cargoes in 2024 reflecting both rising demand and prices.10

Qatar remains the country’s dominant supplier by a significant margin. In 2025, QatarEnergy received approximately $1.2 billion, the single largest supplier payment, delivering 40 contracted cargoes; while Oman’s OQ Trading supplied a further 16 under long-term agreements. The remaining 48 cargoes were procured from the spot market.11

Because Qatar’s LNG exports originate in the Persian Gulf, most shipments to Bangladesh must transit the Strait of Hormuz. As a result, the country’s energy supply chain is structurally exposed to disruptions in Gulf shipping routes.

Bangladesh has pursued a strategy of supplier diversification through contracts with multiple LNG traders and suppliers. However, contractual variety does not necessarily equate to diversification of physical supply. Many LNG traders operating in the Asian market draw from the same Gulf export terminals. As a result, supply disruptions affecting the Persian Gulf would likely affect multiple suppliers simultaneously.

For Bangladesh, the global oil price surge does not remain confined to energy markets. It quickly permeates across fiscal pressure, inflationary stress, and growing strain on the country’s external accounts. As a net energy importer, Bangladesh is particularly sensitive to swings in global fuel prices.

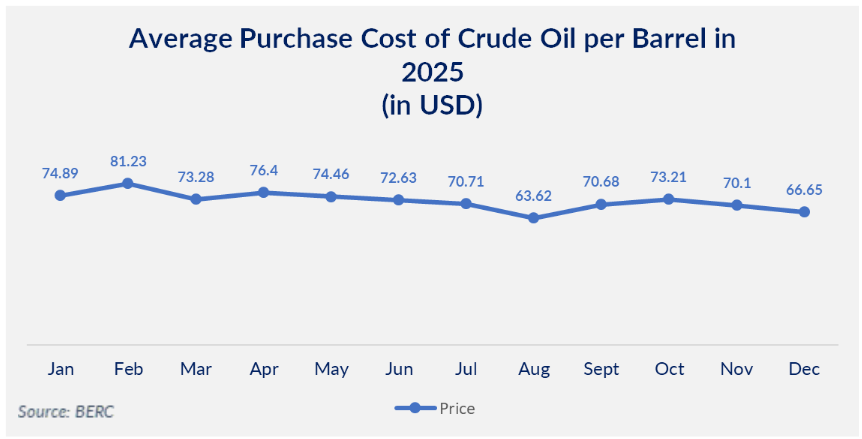

A look at the oil price trend in 2025 helps illustrate this sensitivity. As shown in the price trend, crude oil prices fluctuated between US$63.62 and US$81.23 per barrel during 2025, averaging around the mid-US$70 range for most of the year. At those levels, Bangladesh’s energy import costs remained relatively manageable. However, the ongoing Iran–Israel–U.S. conflict has introduced a new geopolitical risk premium into global oil markets, whereby even a moderate increase in oil prices quickly translates into higher external payments for Bangladesh.

According to macro research by BRAC EPL Stock Brokerage, every US$10 rise in global oil prices could increase Bangladesh’s monthly import bill by approximately US$70–80 million, reflecting the country’s heavy reliance on imported fuel for power generation, transportation, and industrial activity.

Bangladesh already spends close to US$1 billion annually to import more than 6 million tonnes of petroleum products, much of which passes through the Strait of Hormuz.12 As a result, a sustained shift in global prices from the US$70 range toward US$100 per barrel would place immediate pressure on both fiscal balances and foreign exchange requirements. This burden is further amplified by the current conflict, which has increased maritime insurance costs and disrupted energy supply routes through the Strait of Hormuz, raising the delivered cost of both crude oil and LNG imports.

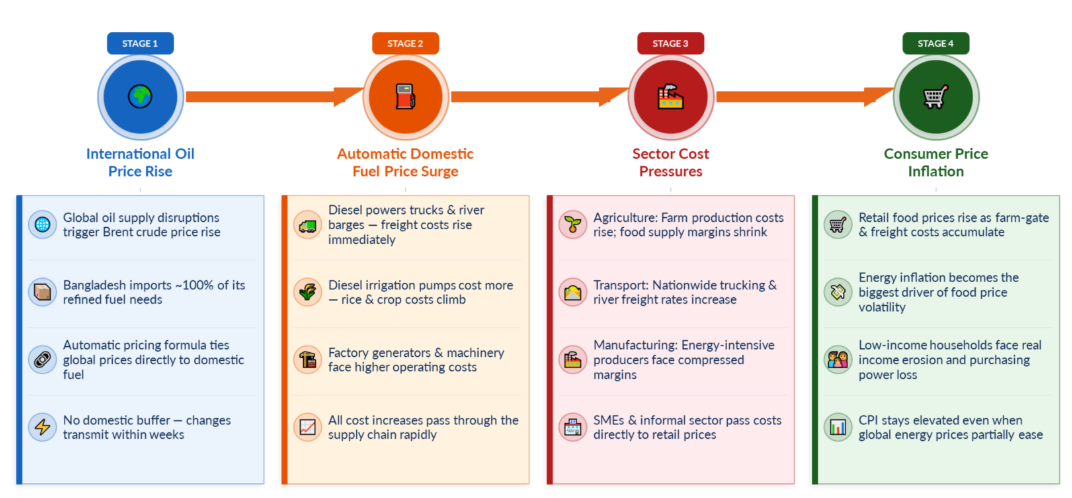

The macroeconomic implications extend beyond the import bill. Rising energy prices quickly feed into imported inflation, particularly through three key transmission channels: transport, irrigation, and food distribution.

This inflationary transmission is occurring at a time when Bangladesh’s consumer price inflation already stands at 8.58 percent year-on-year as of January 2026, leaving limited room for absorbing further energy shocks without risking broader price spirals.

Beyond inflation, the energy shock also threatens to tighten Bangladesh’s foreign exchange liquidity. With foreign exchange reserves standing at approximately US$30.27 billion under the IMF BPM6 methodology, higher oil prices increase the demand for US dollars to finance energy imports.13

In practice, the pressure may emerge first through higher LC margins, trade credit costs, and forward premiums rather than an immediate decline in headline reserves. However, if elevated oil prices persist, policymakers may once again face the difficult trade-offs seen during the 2022 global energy crisis, when Bangladesh introduced restrictions on non-essential imports to preserve foreign currency reserves.

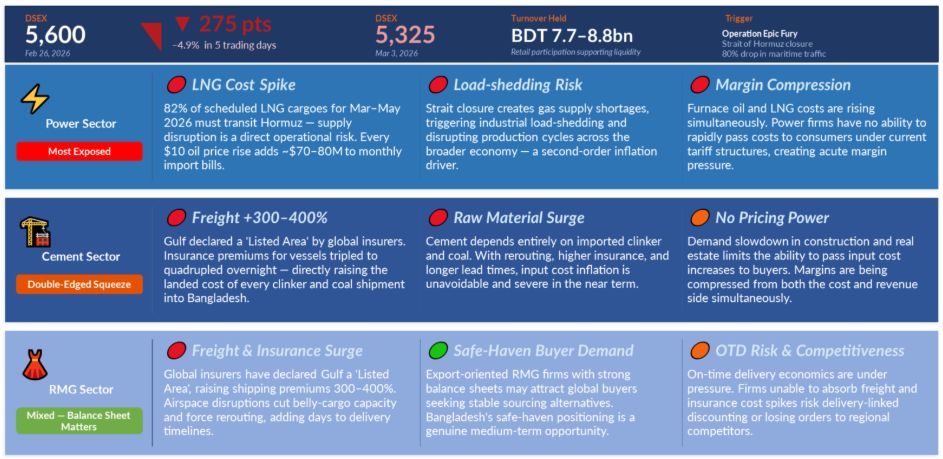

These macroeconomic pressures do not remain confined to fiscal balances or foreign exchange accounts; they quickly cascade into sectoral disruptions across Bangladesh’s domestic economy. The most immediate effects are visible in power and manufacturing, where higher fuel costs and uncertain LNG supply have already prompted policymakers to consider sector-wise energy rationing, prioritizing gas for fertilizers and electricity while expanding coal-based generation to offset Hormuz-linked LNG shortfalls. For energy-intensive industries, intermittent load-shedding is an increasingly real operational risk.

Export-oriented sectors struggle too. With the Persian Gulf now designated a “Listed Area” by global insurers, maritime premiums have surged 300–400 percent, directly raising freight costs for Bangladesh’s RMG sector.14 Tighter logistics timelines, higher transport expenses, and the need for larger inventory buffers are placing additional strain on exporters already navigating a volatile global demand environment.

Side by side, financial markets reflect the unease. The DSEX dropped from 5,600 to 5,325 between late February and early March 2026,15 reflecting a broad “risk-off” correction as investors grew cautious toward energy-exposed sectors including manufacturing, cement, and power.

Yet one stabilizing signal stands out as a countervailing force. High oil prices historically bolster Gulf Cooperation Council (GCC) fiscal revenues, sustaining infrastructure spending and labor demand in economies that account for roughly 51 percent of Bangladesh’s remittance inflows. With remittances already up 18 percent year-on-year to US$16.27 billion in H1 FY2025–26, this channel offers a meaningful, if partial, relief against the external shock, sustaining foreign exchange liquidity at a time when import costs are rising sharply.

Although remittance inflows cannot fully offset the rising energy import burden, they may still provide a partial cushion for Bangladesh’s foreign exchange liquidity during periods of global energy volatility.

If long-term cargo deliveries were disrupted, Bangladesh would be forced to rely more heavily on the global spot LNG market. However, spot prices tend to react sharply to supply shocks.

During the global gas crisis following Russia’s invasion of Ukraine in 2022, Asian spot LNG prices briefly exceeded $59.57 per MMBtu, highlighting the volatility of global gas markets during geopolitical disruptions.17 Even smaller supply disruptions can push prices well above the long-term contract levels typically paid by South Asian importers.

For Bangladesh, which subsidizes electricity tariffs and operates with limited fiscal space, sudden increases in LNG import prices could place significant pressure on public finances. Higher fuel costs would likely translate into increased electricity generation costs, raising the risk of power shortages or tariff adjustments.

Bangladesh maintains modest strategic reserves of refined petroleum products, managed primarily through the Bangladesh Petroleum Corporation. While the country maintains stockpiles of diesel and furnace oil, LNG imports are effectively delivered on a just-in-time basis due to limited storage infrastructure.

This structural feature makes the energy system particularly sensitive to disruptions in maritime supply chains. Even short-term delays in LNG cargo deliveries can force power plants to reduce output or switch to alternative fuels, increasing generation costs.

Bangladesh’s structural exposure to Gulf energy chokepoints must be read against the backdrop of its own domestic energy transition trajectory one that remains significantly behind pace. The government’s Renewable Energy Policy 2025, gazetted in June 2025, targets 20% of electricity generation from renewable sources by 2030 and 30% by 2040.

Yet the gap between ambition and execution is stark. Bangladesh’s current renewable energy capacity stands at approximately 1,696 MW only 5.24% of of total installed capacity. The current energy crisis points us towards a direction which if implemented, would positively impact Bangladesh’s energy landscape.

The Strait of Hormuz has long been recognized as a critical artery of the global energy system. For Bangladesh, the country’s growing reliance on imported LNG means that disruptions in this corridor would reverberate directly through the national power sector.

While such a scenario remains hypothetical, recent geopolitical tensions underscore the fragility of maritime energy supply chains. The lesson for policymakers is clear: resilience in energy systems cannot rely solely on contractual arrangements or market procurement. It requires diversified supply sources, strategic infrastructure, and accelerated domestic energy development.

This article has been co-authored by Sakina Binte Belayet and Sadia Karim, Business Consultants at LightCastle Partners. For further inquiries or clarifications, please contact: info@lightcastlepartners.com

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights