GET IN TOUCH

- Please wait...

The global luxury market was worth USD 296.15 bn in 2013, and leather goods held a dominant share in the basket (TMR, 2013). This value is rising due to the increase in the affluent population, demanding superior quality products. According to Transparency Research, the global luxury goods market will be touching USD374.84 bn in 2020, expanding at 3.5% CAGR between the years 2014 to 2020, and that is expected to lead to growth in the leather industry as well.

While developed countries are already becoming more saturated with high-income customers, emerging countries such as China, India, Thailand, Indonesia, Vietnam, and South Africa are adding new impetus to the global demand for leather products. These countries are currently facing rapid economic growth, increasing GDP, and raising individual income.

Bangladesh is relatively small compared to the other big players in the world leather market, but has potential for growth, both as a consumer and as an exporter. Bangladesh’s leather is widely known for its high qualities of fine grain, uniform fiber structure, smooth feel and natural texture.

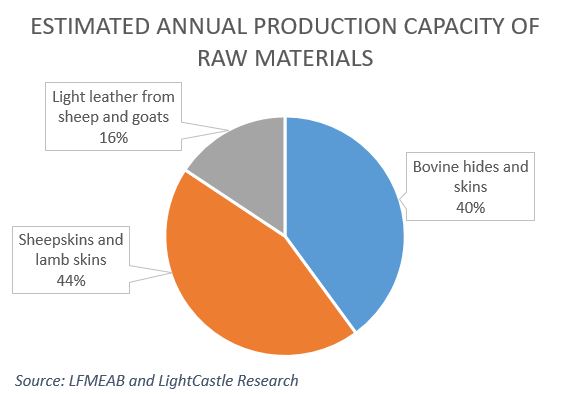

The leather industry is one of the oldest in the country. It is paving its ways towards gaining larger international market share by providing more value added goods. The country is blessed with a large supply of raw materials and inexpensive labor. The annual production capacity of raw materials is estimated to be around 750 million sq. ft. (LFMEAB and LightCastle Research)

.

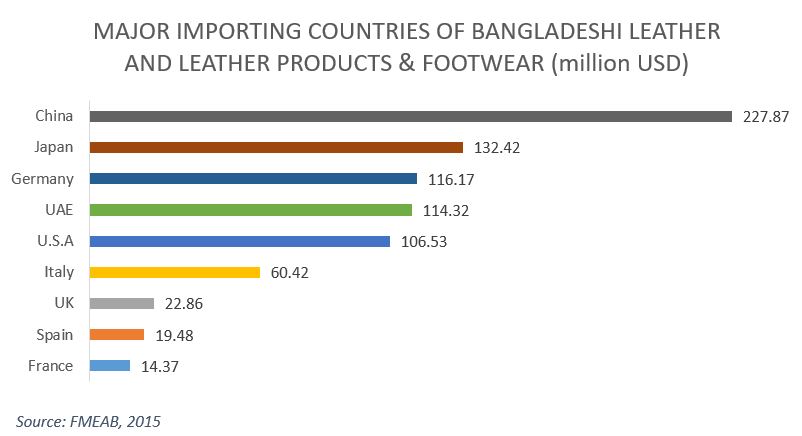

Currently, there are around 113 tanneries, mostly located in the Hazaribagh area in Dhaka city, annually producing around 300 million sp. ft. of leather; more than 75% of which is exported. As part of Bangladesh’s growth trajectory in leather export, the country has experienced CAGR growth of 16% over the last 6 years, and is currently exporting over USD 1.1 billion annually. This is roughly 0.5% of the global market. However, industry experts estimate this to grow significantly, as global demands are rising. On top of this, major leather product producers are experiencing labor cost hike in their countries, which have contributed to some of them relocating their factories to countries like Bangladesh, where overhead costs are comparatively lower.

Moving in the production of value added products the industry can earn higher revenue. The industry currently has over 3,500 companies of various sizes producing these leather products. The country has been exporting more leather footwear and other leather products, and less processed leather over the last 6 years. This is allowing the country to increase export earning, by moving up the value chain.

Broadly, the leather industry can be categorized in three phases. In the first phase, the raw hides are collected from across the country. A portion of these hides are processed in the local tanneries, while a significant percentage is illegally exported to neighboring country after undergoing basic processing.

In the second phase, the raw leather is processed in 112 plus tanneries currently operating within Bangladesh. The semi-processed and processed leather are either exported to the international market or sold to local leather product manufacturers. The leather manufacturers produce leather products e.g. Shoes, belt, Wallet and subsequently sell them in the domestic or international markets.

During Eid-al-adha (religious festival), when large number of animals are sacrificed, raw hide supply spikes up temporarily, which goes beyond the cumulative processing capacity of local tanneries. As a result, a significant percentage of raw hides are smuggled outside Bangladesh.

Beside the export market, the local market is also booming. The economic growth of Bangladesh has been impressive over the last decade, despite multiple challenges affecting the economy. Rising GDP and slowing population growth have contributed to rising per capita income exceeding lower income threshold. This has resulted in a gradual increase in consumer spending over the previous years.

According to BCG, more than half the population of Bangladesh, 84 million, have income that classify them as being bottom of the pyramid. However, this group is expected to shrink to 48 million by 2025[1]. While aspirant segment will grow to nearly 92 million by 2025, the emerging middle class will swell from 17 million to 27 million within the decade.

Despite achieving sustained growth over the last decade, industry experts still feel that the industry is not operating at its full potential. Some of the existing challenges are posing as barrier to the sector’s growth:

For charting a winning strategy for excelling in the international leather markets, all relevant stakeholders vested in the sector’s growth must play pivotal roles:

Mahir Abrar Nikhat is a business consultant at LightCastle Partners. He graduated from the University of Hong Kong, majored in economics and finance, and currently is enrolled in North South University, completing masters in economics program.

Zahedul Amin is the Co-founder and Director of Finance at LightCastle Partners, an emerging market specialized business planning and intelligence firm. Earlier, he worked as the Assistant Vice President, Risk Analysis Unit, in HSBC. He completed his E-MBA at the Institute of Business Administration (IBA), University of Dhaka, and completed his undergraduate degree from the same institute.

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights