GET IN TOUCH

- Please wait...

The leather and footwear play a pivotal role in the nation’s economic growth, contributing significantly to export earnings and ranking second in this category. Similarly, Bangladesh maintains a prominent position in the global market, by securing a rank of 18th position in the global footwear market. With a 3 percent share in the global leather and leather products market and representing 10 percent of the worldwide leather industry, Bangladesh has established itself as a competitive player.[1] Additionally, the country’s robust backward and forward linkage industries reinforce its domestic and international standing, highlighting its potential for continued growth and investment in this dynamic sector.

![Figure 1: A Snapshot of Leather and Footwear Industry in Bangladesh [2]](https://lightcastlepartners.com/wp-content/uploads/2025/05/image-2.png)

Figure 1: A Snapshot of Leather and Footwear Industry in Bangladesh [2]

Over the past five years, the sector has seen remarkable growth, particularly in leather footwear exports, which have outpaced processed leather and leather products’ exports, signaling a shift toward higher-value products.

Figure 3: Status of leather export growth over the past five years.

One of the major reasons behind this sector’s boom is the shift of investments from China to Bangladesh’s leather and footwear industry. This shift began in 2006 when the European Union (EU) imposed anti-dumping duties of 16.5 percent on Chinese shoes and 10 percent on Vietnamese shoes, later debating whether to extend them in 2016 as well.[3] These measures redirected foreign direct investment (FDI) toward South Asian nations, with Bangladesh emerging as a major beneficiary.

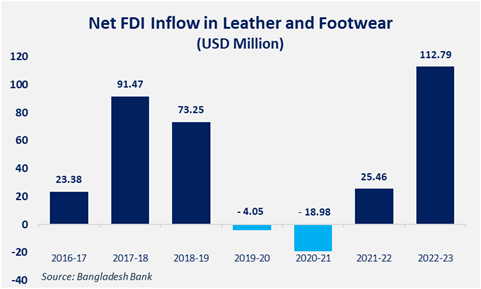

As depicted in the graph, the Fiscal Years (FY) 2019-20 and 2020-21, witnessed a downturn in FDI within Bangladesh’s leather and footwear sector. This decline is likely attributable to the global disruptions caused by the COVID-19 pandemic, which brought international trade and economic activities to a temporary halt, significantly impacting investment flows across industries. However, in FY 2021-22, the sector demonstrated resilience, recording a positive net FDI inflow of USD 25.5 million, reflecting robust investor confidence and a strong recovery trajectory in the subsequent year.

To sustain this momentum, the Bangladesh Investment Development Authority (BIDA) has prioritized the leather and footwear industry within its top 19 sectors in the FDI heatmap. The leather and footwear segment falls under category B targeted to streamline entry processes aimed at attracting further FDI and Joint Ventures (JVs), reinforcing Bangladesh’s position as a key investment destination.

In addition to the BIDA’s FDI Heatmap, the government introduced the ‘Leather and Leather Products Development Policy’ in August 2019, offering incentives to boost export earnings. Recognized as a high-priority industry under the Export Policy 2024-27 and the National Industry Policy 2016, the sector is further supported by the establishment of three industrial estates in Rajshahi, Savar, and Chattogram, dedicated to leather and tannery operations, equipping with strong infrastructural capacities.

| Policy Incentives to Support the Leather & Footwear Industry in Bangladesh[4] The government is offering Reduced Corporate Income Tax (CIT) for a duration of 5 to 10 years, depending on the location, for instance, Export Processing Zones and Economic Zones, and depending on specified sectors, including manufacturing, and information technology among others.Import duty exemption on capital machinery.Exemption from regulatory/supplemental duties for footwear producers using specific materials like tubes, pipes, plastic, PVC screens, and textile/knitted fabric, due to the rising demand for non-leather footwear around the world.50 percent tax exemption for income generated from exports.No imposition of Value Added Tax (VAT) on exported goods.Bonded warehouse license tenure extended to 3 years effective from 2024. [5]A 15 percent cash incentive on the export value of leather goods and footwear, with an additional 5 percent for crust leather from the Savar Estate. |

The export policies and shift of investment from China open significant opportunities for Bangladesh’s leather and footwear sector, attracting global brands like Nike, Adidas, and Puma, who are reportedly moving their sourcing to South Asia, reinforcing Bangladesh’s role as a key manufacturing hub. [6]

Figure 4: Emerging Opportunities in the South Asian Countries

The country’s investment-friendly policies and cost-efficient production base provide a strategic advantage, granting duty- and quota-free access to major markets, including the EU, UK, Japan, Canada, Russia, and Australia. This competitive edge positions Bangladesh as a prominent global supplier of leather goods, catering to diverse consumer demands.

The article was authored by Sadia Karim, Business Analyst at LightCastle Partners. For further clarifications please contact here: [email protected]

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights