GET IN TOUCH

- Please wait...

The Bangladesh FY26 Budget Analysis reveals a contractionary stance, with the BDT 7,900 billion budget marking a 1% decline from the previous fiscal year. This rare shrinkage highlights the government’s attempt to balance fiscal consolidation with the need to manage inflationary pressures, revenue mobilization, and targeted social protection.

Against a backdrop of global economic uncertainties and domestic reforms, the FY26 budget signals a strategic recalibration aimed at stabilizing growth while addressing critical structural challenges.

A key driver behind this downsizing is the Annual Development Programme (ADP), which has been reduced by 13.2% from last year’s original allocation. This adjustment signals the interim government’s focus on austerity, with notable cuts to lower-priority projects in an effort to streamline public spending.

This write-up takes a closer look at the key changes proposed in the budget and aims to reflect on their possible impacts in the medium to long term on businesses and the wider economy.

The interim government took charge of an economy grappling with high inflation, a fragile banking system, and rising public debt. Although remittance inflows and foreign reserves have shown some improvement over the past 10 months, the broader economic outlook remains uncertain.

Alongside these domestic hurdles, the FY 2026 budget also had to contend with external pressures. In response, the government presented a contractionary, deficit-focused budget—prioritizing stability over bold reforms.

| Category | Factors | Description |

| External | Global Commodity Prices Fluctuation | Commodity prices showed mixed trends, with fertilizer like urea increasing sharply from $338/MT in Jan-Mar’24 to $403.8/MT over the same period in 2025. In contrast, crude oil prices declined from an average of $80.6/barrel to $74.2/barrel, easing some inflationary pressure. |

| LDC Graduation | Bangladesh’s overall exports to the EU could decline by 21%, primarily due to the loss of duty-free access following LDC graduationCash subsidy on exports to be slashed by BDT 10 Bn | |

| Global Trade Barriers | Tariff on Bangladeshi products in the US has been increased from 15% to 35%India’s trade barriers on Bangladesh may impact imports worth $770 Mn | |

| Internal | Political Uncertainty | Post-uprising political uncertainty affecting investor confidence and implementation of reforms. |

| Moderately High Inflation & Currency Depreciation | Inflation, which remained over 9% for around 2 years, is showing a downward trend, reaching 9.05% in May 2025. | |

| Stressed Banking Sector | NPLs have more than doubled in just one year (24% in Mar’25 vs. 11.1% in Mar’24)Alarmingly thin CRAR at 3% (Dec’25) far below the regulatory requirement of 10%Weakened private sector credit growth at 7.5% (April’25) |

Development allocations for key public sectors like education, health, and agriculture have not seen meaningful increases—raising concern as Bangladesh approaches LDC graduation, when it will lose critical preferential benefits.

For instance, the TRIPS waiver loss may raise medicine prices by nearly 20%, while the phase-out of export subsidies and tax exemptions could significantly hurt the agriculture sector. Meanwhile, the budget’s social protection provisions may turn out to be insufficient against the backdrop of current inflation.

| GDP growth target of 5.5% in FY26 vs. to 5.25% in RBFY25 |

| Projected inflation: 6.5% in FY26 (same as FY25) |

| Revenue target: 9% of GDP in FY26 vs. 9.35% of GDP in RBFY25 |

| Private sector credit growth: 11% in FY26 vs. to 9.8% in RBFY25 |

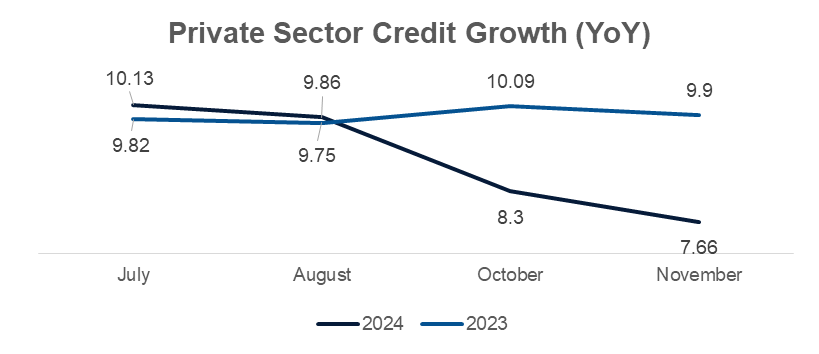

Regarding the private sector, the lack of significant improvement in the overall economic environment has led businesses to adopt a wait-and-see approach. According to LightCastle’s Business Confidence Index (2025) report, almost half of industry leaders identified the high cost of credit as a key obstacle to business operations. In this context, the projected rise in private sector credit growth may be overly optimistic, given the elevated lending rates of 14% to 16% and the government’s growing dependence on bank borrowing.

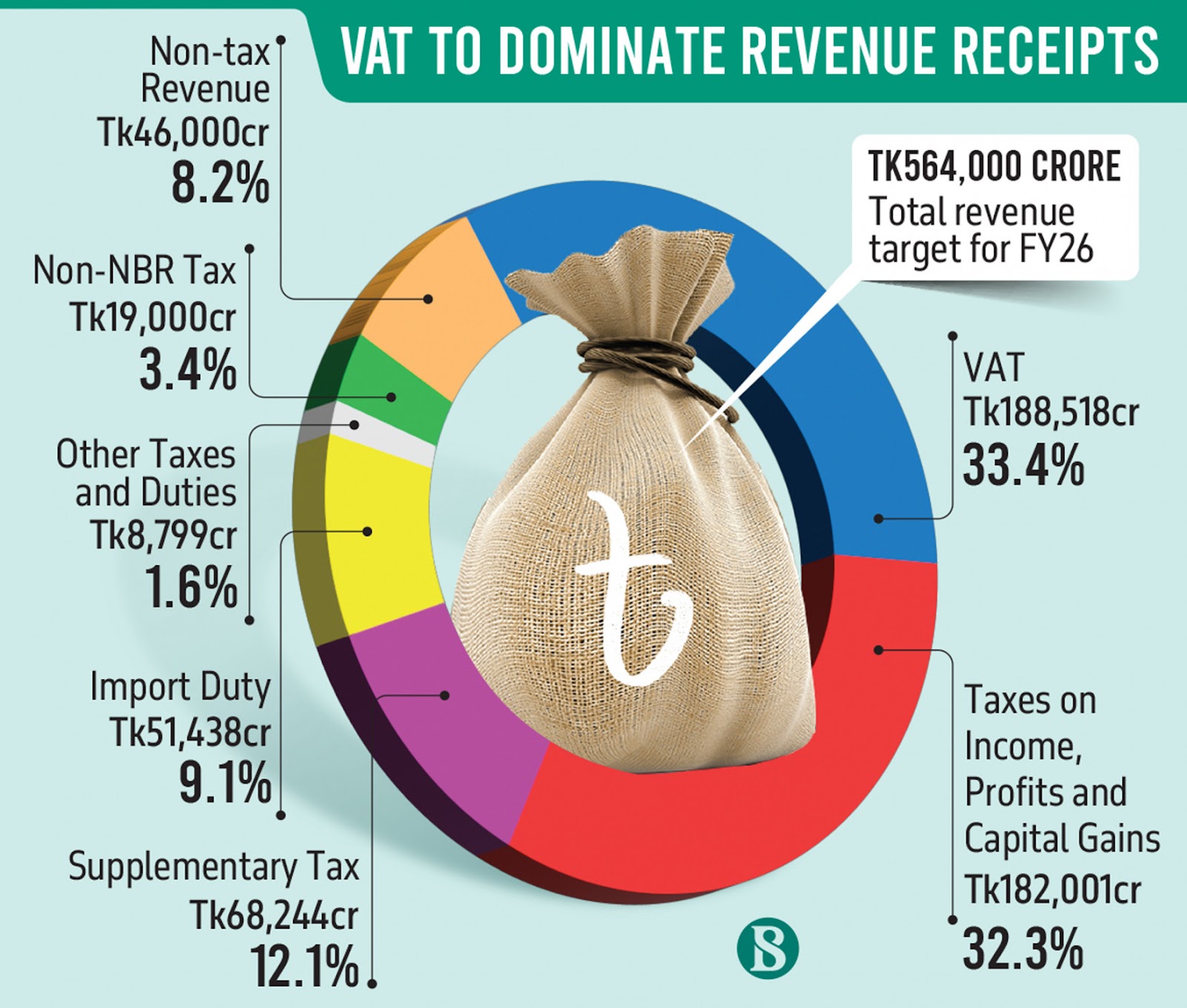

For the disbursement of the fourth and 5th tranche of the IMF lending program, one of the major conditions was increasing the tax-to-GDP ratio. This is because in Bangladesh, tax-to-GDP has remained around 7% to 8% for several years, ranking among the lowest in South Asia.

This limited revenue base underpins many of the country’s fiscal issues, including ongoing budget deficits and increasing external debt.

In FY24, Value Added Tax (VAT) and Supplementary Duty (SD) contributed 3.86% to the country’s GDP, whereas income taxes accounted for only 2.26% of GDP.

Indirect tax tends to dominate the revenue pie with two-thirds contribution and it is no different for the upcoming fiscal year. Furthermore, tax holidays, exemptions and rebates account for about 6.5% of the GDP, while total tax collection is just about 8%.

| VAT component | Previous | New | Who is affected | Impact |

| Higher (or restored) rates | ||||

| Construction services | 7.5% | 10% | All contractors, civil & finishing works (thedailystar.net) | Project costs likely to rise; developers may pass on costs to clients, slowing demand in real estate and infrastructure |

| Online marketplace commission | 5% | 15% | E-commerce platforms, delivery “aggregators” (thedailystar.net) | Higher operational costs for ecommerce platforms, food delivery apps; could reduce commission margins or lead to higher prices for sellers/buyers |

| Mobile handsets | 5% (local)/ 7.5% (import) | 7.5%/10% | Assemblers & importers; retail prices expected to rise (dhakatribune.com) | Squeezed profit margins |

| Plastic household/kitchenware & hygiene items | 7.5% | 15% | Local producers & importers (thedailystar.net) | Cost of basic consumer items to rise, especially affecting low-income households |

| New or extended exemptions/lower rates | ||||

| Basic hygiene goods | Exemption expiring ’25 | Exemption extended to 2030 | FMCG producers (tbsnews.net) | Helps maintain affordability and demand for essential items; supports public health objectives |

| LNG import | 15% | 0% | Power plants & industry (thedailystar.net) | May help mitigate inflationary pressure in energy-intensive sectors |

| Hospital beds (imported/locally procured inputs) | 15% | 0% | Health-care equipment suppliers (tbsnews.net) | Makes medical infrastructure cheaper, |

| Active pharmaceutical ingredients (API) | Expiring ’25 | 0% till 2030 | Pharma manufacturers (tbsnews.net) | Strengthens Bangladesh’s position in generic drug exports and reduces dependency on imports |

| Lithium & graphene batteries | 15% | Graduated (0 → 5 %) | Green-tech producers (tbsnews.net) | Incentivizes local assembly of EVs, solar/storage products; could attract FDI in renewables |

| Hybrid & electric vehicles | 0% (expiring) | 0 % to 2030 | Auto assemblers (tbsnews.net) | Promotes investment in EVs; may reduce vehicle costs for end-users over time |

| Thresholds & procedural tweaks | ||||

| Bank deposit threshold for VAT-exempt interest | Tk 100,000 | Tk 300,000 | Small savers (newagebd.net) | Encourages small savings and reduces VAT-related friction for retail depositors |

In line with IMF recommendations, the government has increased VAT on several goods to the standard 15% and reduced tax benefits, particularly for industries with mature local production. To ease the transition, tax exemptions on select imported raw materials used in manufacturing these products will remain in place until June 2028, providing relief for import-dependent producers.

These measures seek to strike a balance—supporting priority sectors like healthcare and technology, while gradually phasing out incentives for non-essential goods and industries with sufficient domestic capability.

Electronics & Home Appliances:

While the withdrawal of the reduced VAT for electronics aligns with a strategy to expand the VAT base, it does mark a shift away from the long-standing incentives that helped transform Bangladesh’s electronics market.

Energy & Environment

Healthcare & Pharmaceuticals

Despite having 10 million registered taxpayers with TINs, only about 30% to 35% are currently compliant and actively paying taxes. Looking ahead, although the tax-free income threshold is set to rise from the 2026–27 assessment year, no immediate relief has been extended to individual taxpayers for the upcoming fiscal year.

The income tax rates will remain unchanged for FY26 and the current threshold of Tk 350,000 stays in place. In addition, with VAT increases on essentials ranging from kitchenware to home appliances, the overall tax burden is expected to grow further, all while inflation hovers around a high 9%.

| Income Slab (FY27 & FY28) | Tax Rate (%) |

| Up to BDT 3.75 lakh | 0% |

| BDT 3.75 lakh plus to BDT 6.75 lakh | 10% |

| BDT 6.75 lakh plus to BDT 10.75 lakh | 15% |

| BDT 10.75 lakh plus to BDT 15.75 lakh | 20% |

| BDT 15.75 lakh plus to BDT 35.75 lakh | 25% |

| BDT 35.75 lakh plus | 30% |

With regards to corporate tax, it has been slashed for publicly traded companies, with specific conditions leading to rates as low as 20% if all income is transacted via bank transfer. Private universities and medical, dental, engineering, and IT-focused colleges also see their corporate tax rate reduced from 15% to 10%.

In addition, the budget has included measures to broaden the tax base or increase the burden for specific entities or activities. The National Board of Revenue (NBR) has abolished the special tax provision that previously allowed declaring investments in buildings or apartments by paying a special tax.

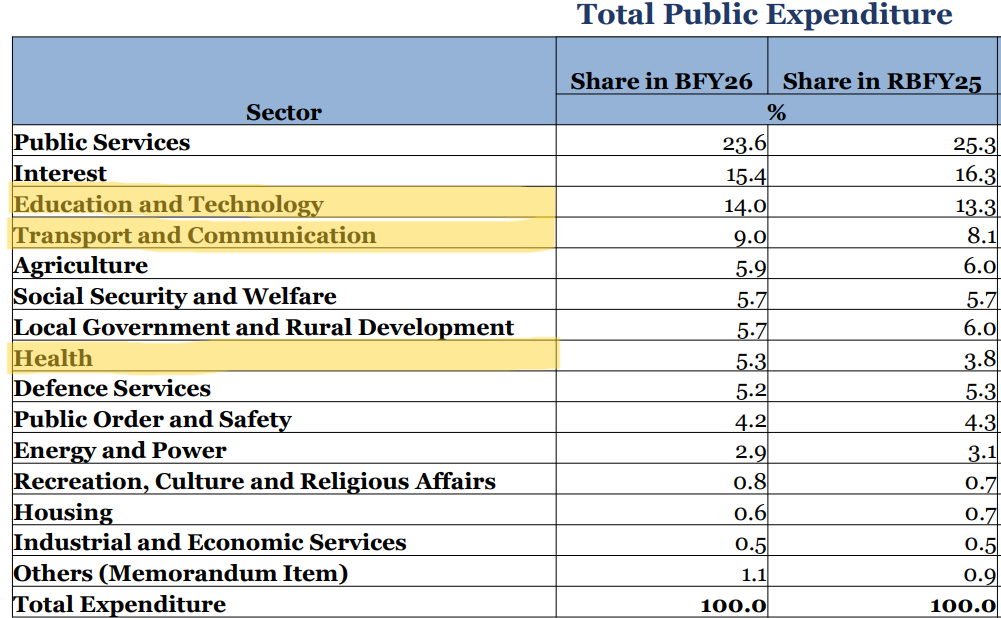

The proposed budget for FY26 adopts a prudent yet targeted strategy, prioritizing key sectors such as healthcare, transport, and education amid ongoing fiscal constraints.

Source: Centre for Policy Dialogue

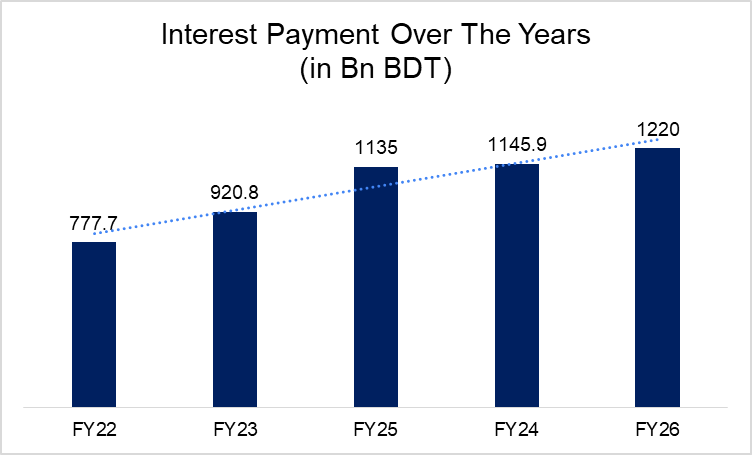

While public services and interest payments continue to receive the highest allocations, both have experienced a slight decline compared to the FY25 budget. This modest reduction in interest payment allocations comes at a time when debt repayment pressures are expected to intensify.

The expiry of grace periods for several large loans and budget support—primarily secured for mega infrastructure projects—is anticipated to increase the fiscal burden.

On a positive note, the gradual recovery of liquidity and foreign exchange reserves has contributed to the stabilization of the exchange rate, which is expected to ease the cost of debt servicing to some extent.

Source: Economic Relations Division

In the Annual Development Plan (ADP), around 70% of the total allocation has been concentrated in five key sectors: transport and communication, power and energy, education, housing and community services, and health. Notably, the Rooppur Nuclear Power Plant received the highest individual allocation for FY26. Given that the plant is about 80% complete and scheduled to begin operations later this year, this allocation may be warranted. However, attention should be paid to the projects that continue to receive funding despite limited need.

Having said that, we now turn to an analysis of the budgetary allocations for the priority sectors of the economy.

For FY26, the Agriculture and Allied Sector (AAS) has been allocated Tk 46,268 crore, reflecting a 3.8% increase compared to the revised budget of FY25. Of this amount, agricultural subsidies make up 37% of the total allocation – focusing on fertiliser and mechanisation.

As global fertiliser prices continue to climb—urea rising from $313.7 per metric ton in Q2 ’24 to $403.8 per metric ton in early 2025—the Bangladesh government has been compelled to adjust its subsidy support to shield farmers from the impact of these escalating input costs.

The budget has proposed a reduction in the advance income tax (AIT) on industrial raw materials, which is expected to lower input costs for agro-processors. Additionally, the withholding tax rate on the supply of essential goods such as paddy, wheat and potatoes has been proposed to be reduced from 1% to 0.5%.

To further strengthen food security, the interim government has maintained a tax exemption on annual income from farming activities up to BDT 500,000. Although the government has retained VAT exemption on LNG, actual gas availability is uncertain, given the pressure from the power and industrial sectors. A constrained gas supply could raise fertilizer costs and negatively affect crop production.

The White Paper on Bangladesh’s economy had underscored the importance of shifting away from a rice-centric model and encouraging crop diversification into high-value crops. While the budget does touch on positive measures such as promoting climate-resilient crop varieties and improved farming technologies it falls short of making any meaningful financial commitments specifically aimed at supporting diversification efforts.

Bangladesh, where over 70% of total health expenses are borne out-of-pocket by individuals, remains at a critical juncture in its journey toward accessible healthcare. Although government spending on the health sector has seen a gradual increase over the years, the allocation still remains modest.

The total health budget has seen a modest increase of just 1%, rising from BDT 414.08 billion in FY25 to BDT 419.08 billion in FY26. More than 50% continues to be absorbed by routine administrative expenses, leaving limited resources for direct patient care.

On the brighter side, duty and tax exemptions have been extended to include raw materials for all types of pharmaceutical products, encompassing cancer drugs and APIs. Proposal has also been floated to add 79 new items—including 23 cancer drug ingredients and 20 types of medical equipment to the list of tax‑exempt imports, aimed at improving affordability of treatment.

The proposed allocation for education remains at 1.53% of GDP, falling far short of the 4-6% recommended by UNESCO and below the national target of 3.5% by FY25. This marks a continued trend of education spending remaining below 2% of GDP for the past two decades.

While the overall education budget saw a marginal 1% increase in FY26, development expenditure remains notably low, with ADP allocation only increasing from 11.9% in FY25 to 12.4% in FY26. As such, development activities such as the construction of new schools, digital learning facilities, and educational reforms may continue to lag.

This is particularly problematic in a fast-changing global economy where innovation and digital literacy are key drivers of growth. Furthermore, the allocation for primary and mass education actually decreased from its original FY25 budget while the technical and madrasah education, along with secondary and higher education, have received increased funding.

While raising the loan ceiling and introducing a Tk 100 crore youth fund signals a commitment to entrepreneurship, without complementary investments in quality education and skill-building, the effectiveness of such financial instruments could be limited.

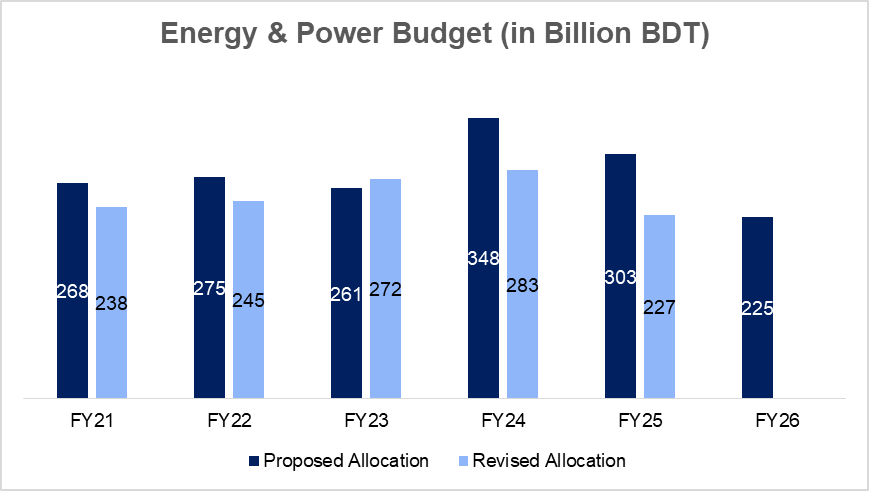

The FY26 budget reflects a significant reallocation of resources, with the power division experiencing a reduction of approximately 30% in its allocation compared to the previous fiscal year, while the energy division witnessed an almost twofold increase in funding. This reallocation is largely driven by the government’s plan to cut electricity subsidies by over BDT 110 billion through lower production costs.

On the energy front, the budget outlines an increase in LNG imports from 5 to 6.5 million tonnes, alongside a 15% VAT exemption on LNG and a reduction in TDS on electricity payments. Additionally, funds have been earmarked for drilling at least 17 new gas wells, signaling a stronger focus on domestic gas exploration as part of broader sectoral reforms.

However, the budget’s heavy emphasis on fossil fuels raises concerns about Bangladesh’s commitment to clean energy transition goals. While there is an ambition to add 3,400MW from clean energy sources, by 2028, the budget lacks any clear tariff relief for renewable energy-based power generation equipment. A reduction in VAT on additional solar components, apart from inverters, could have been a more supportive step to encourage households and businesses to adopt solar energy solutions.

Source: Ministry of Finance

In FY26, the government has proposed a total social safety net allocation of BDT 1,167.3 billion, accounting for just 1.87% of GDP. Notably, this excludes interest payments on national savings certificates (NSCs)—a commendable move. In contrast, the previous year’s allocation was heavily skewed, with pensions, NSC interest, and agricultural subsidies comprising 46% of the total, leaving limited room for direct support to the truly vulnerable.

While this year’s budget shows an intent to sharpen targeting within social safety nets, concerns remain about whether the revised allowances are enough to shield vulnerable groups from the pressure of rising living costs. Monthly benefits under ten major schemes have seen only modest increases—ranging from BDT 50 to BDT 100. Encouragingly, the government plans to widen the coverage of several schemes, signaling a stronger push for inclusivity.

Special allocations have also been proposed for those injured and the families of those killed in the July 2024 uprising. Yet, once pensions for government employees, agricultural subsidies, and freedom fighter allowances are excluded, the core allocation for social security amounts to just 0.92% of GDP.

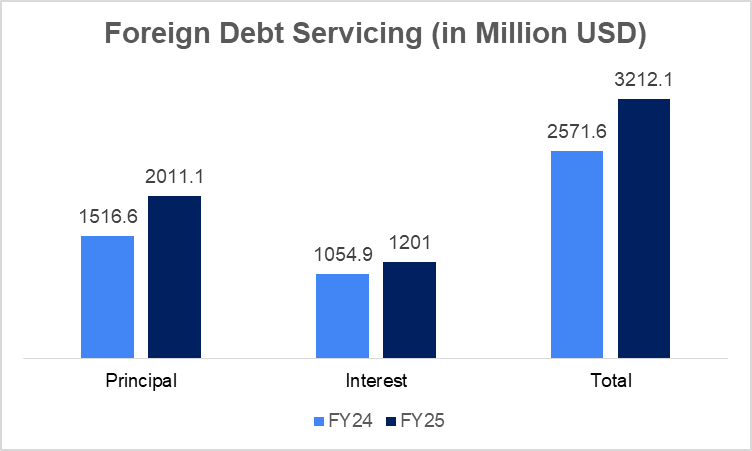

The management of the fiscal deficit for FY26 is anchored in a comprehensive strategy designed to restore fiscal discipline and combat inflation. The proposed deficit is projected at BDT 2,260 billion, which represents 3.62% of the GDP, a notable reduction from BDT 2,560 billion in the previous fiscal year. The government is committed to refraining from borrowing to finance mega projects and will not take short-term or high-interest loans to prevent increasing the debt burden.

As Bangladesh moves closer to graduating from LDC status, both multilateral and bilateral lenders have started increasing their interest rates. For example, Japan, which previously offered loans at around 1%, has now raised its rate to 2%. Similarly, organizations such as the World Bank and the Asian Development Bank are now providing part of their financing at market-based interest rates. Additionally, the depreciation of the BDT against the US dollar over the past three years has significantly increased the cost of servicing foreign loans in local currency terms.

Source: Compiled by the writer

With the budget now approved, discussions around allocations have become secondary—what truly matters is effective implementation. In this context, ensuring accountability in the public sector could help bridge the trust gap between the government and the people while further encouraging the citizens to pay taxes. In a country where tax collection remains modest and public dissatisfaction with service delivery runs high, citizens are justified in questioning how their money is being spent.

Looking ahead, alongside efforts to rebuild trust, there is also an opportunity to address the broader fiscal deficit. Bangladesh’s vast informal economy—employing nearly 85% of the workforce—remains a major hurdle to expanding the tax base.

By introducing simplified tax regimes, offering tax incentives for new registrants, the government can encourage greater compliance. Lessons from countries like Indonesia and India, where low flat-rate taxes and streamlined processes have helped formalize small businesses, suggest that similar reforms in Bangladesh could enhance revenue while gradually bringing informal enterprises into the formal fold.

Lastly, strengthening tax collection requires modernizing the National Board of Revenue (NBR) through digital tax filing systems while ensuring high-income earners contribute fairly.

This article was authored by Naziba Ali, Business Consultant. Advisory support was provided by Priyo Pranto, Senior Business Consultant and Sanjir Ali, Senior Business Consultant and Project Manager at LightCastle Partners. For further clarifications, contact here: [email protected].

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights