GET IN TOUCH

- Please wait...

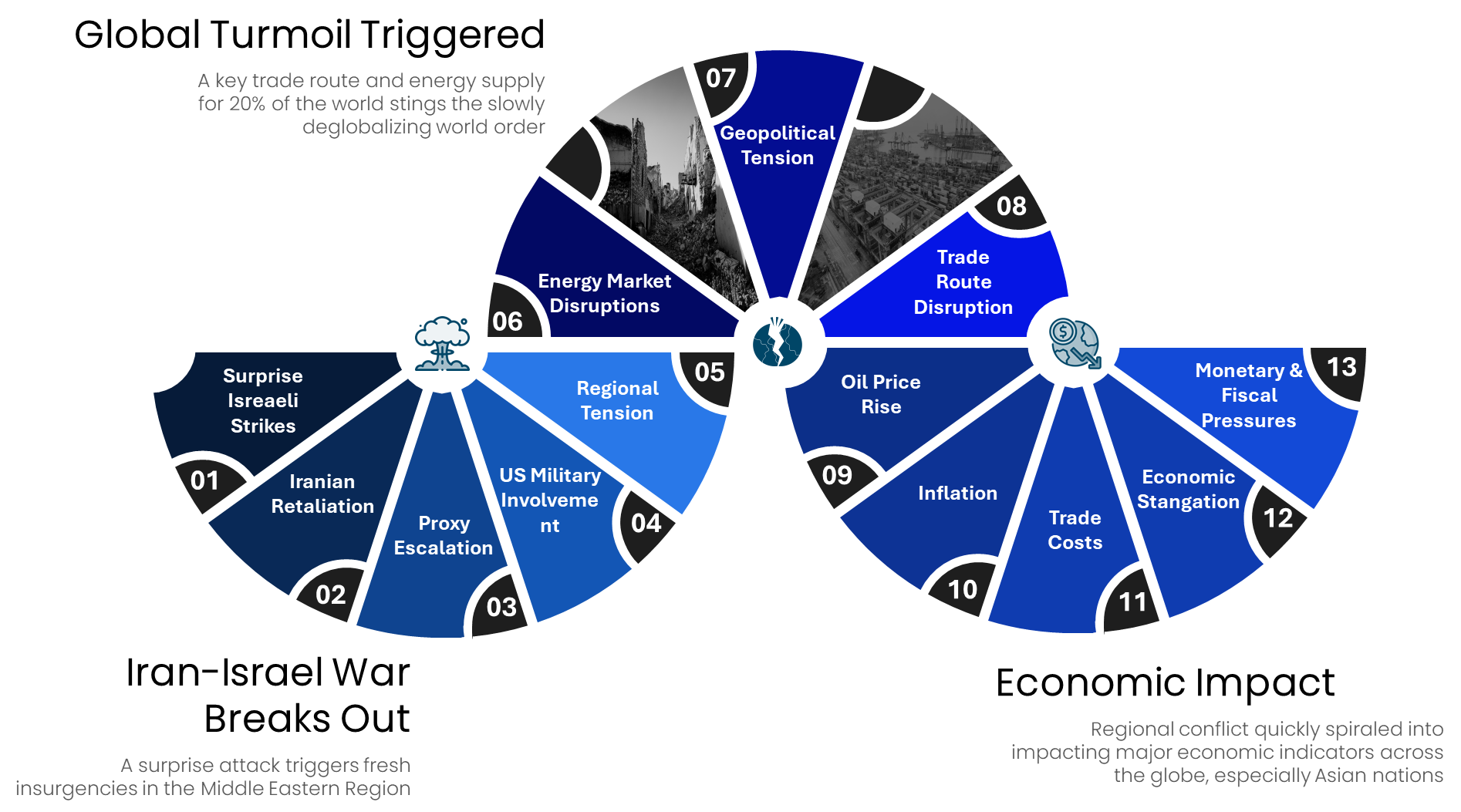

The last half a decade has been an economic, social, and environmental roller coaster for the world. Only a handful of economies weathered the pandemic and the Russia-Ukraine war, facing significant inflationary pressures as two of the world’s largest energy and wheat suppliers went to war.

The latest conflict in the Middle East (1) Reignited energy & fuel price surges – brent crude oil prices reaching five-month highs (near USD 79 in mid-June) and Asia’s spot LNG prices reached four-month highs (about USD 14/MMBtu in June)3 (2) Disrupted trade routes and freight costs – LNG tanker charter rates rose to 8-month highs and insurance skyrocketed4 (3), which in turn negatively swayed inflationary & economic indicators– including consumer spending in some regions, and threatened remittance inflow for others.

Figure: The Trickle Down Effect of Global Headwinds to Local Economies1

Figure: Brent Crude Oil Price Trends (USD) — May to June 2025

The recovery phase for Bangladesh in readjusting with pandemic-period supply chain shocks and war-led inflationary pressures had to grapple with internal turmoil alongside global headwinds. Despite challenges, a creeping decline of the double inflationary pressures (10.13% as of May 2025), a reforming and slowly replenishing central reserve (USD 21 billion as of May 2024-25 as per BPM6)5, and hopeful trade opportunities gave hope of a quick recovery.

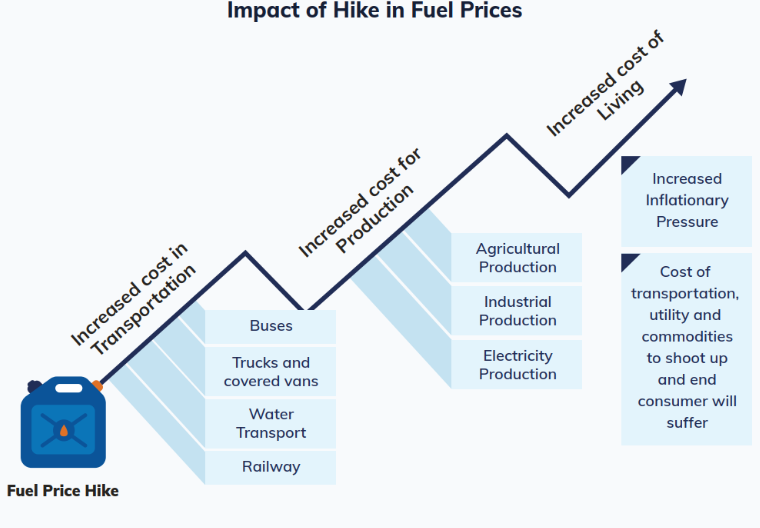

However, the conflict rippled across key economic foundations that supported this positive outlook. Any impact on energy & fuel alone, of which the Middle East is a key supplier, tends to trickle down across the factors of production to daily lives.

Figure: Rise in Fuel Prices Quickly Seep into the Burdens of Everyday Cost of Living

Any disruptions in the Strait of Hormuz, responsible for the transit of 20% of the world’s LNG supply,6 also threaten energy prices in Bangladesh. Petrobangla officials confirm that about 75% of imported LNG under long-term contracts from Qatar and Oman, and roughly 30% of spot market LNG, depend on the Strait of Hormuz for transportation. Although prices are not expected to go up in the short term, since the purchase of recent stocks precedes post-war prices.

Since mid-June, insurance premiums for tankers and freight rates on maritime routes through the Strait of Hormuz and the Suez Canal have surged by roughly 60%.7 This situation arose as insurers and shippers responded to rising regional tensions and perceived risks. Even though commercial vessels have not been directly targeted yet, the increased risk situation has already raised operating costs for global shipping.

The RMG sector, which relies heavily on predictable, cost-efficient sea freight to reach major markets in Europe and North America, is particularly vulnerable to this conflict. Rising logistics expenses affect already thin profit margins and may force exporters to raise product prices. This is expected to potentially reduce their appeal in a price-sensitive global market.

Additionally, several freight companies have begun rerouting ships to avoid high-risk zones. This will increase transit times and operational complexity. These delays can disrupt just-in-time delivery schedules and create bottlenecks in supply chains, affecting order fulfillment for large international retailers.

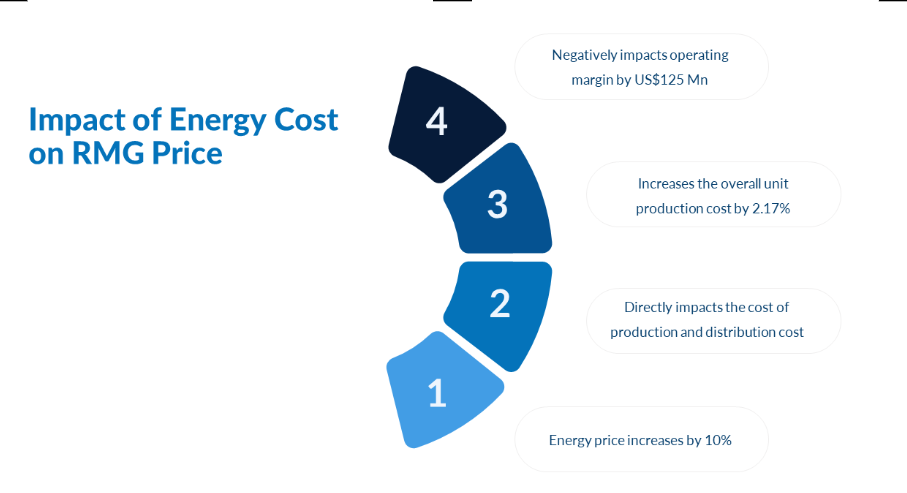

The RMG sector is the backbone of Bangladesh’s export economy. It accounted for over 80% of total export earnings and generated approximately $38.48 billion in 2024.8. This high dependence on a single sector makes the broader economy sensitive to any disruptions in its cost structure. According to the BGMEA, a 23% increase in fuel prices can increase production costs by 5%.9

That means a 10% rise in fuel prices (driven by global crude spikes) could therefore raise overall unit production costs by 2.17%. For a $38.48 billion industry with an average of a 15% profit margin (USD 5.77 billion), this translates to an annual reduction of $125 million in operating margins. These cost increases either reduce profitability or force exporters to raise prices.

These risks reduce their competitive edge in key markets such as the U.S. and Europe. Moreover, while a $10 per barrel increase in oil prices typically adds about 0.2 percentage points to inflation in advanced economies, the effect is likely more pronounced in Bangladesh due to its energy import dependence and limited fiscal capacity to absorb shocks.

BGMEA President Mahmud Hasan Khan Babu has warned that higher fuel costs, combined with ongoing challenges such as domestic inflation, rising labor costs, elevated interest rates, newly imposed U.S. tariffs, and disruptions in Indian transshipment routes, could significantly undercut the sector’s global competitiveness.

Historically, Iran’s retaliation towards US aggression has been projected across the Middle East, targeting allied nations (such as Saudi Arabia or Qatar that host US military bases). Israel’s retaliation, on the other hand, started from Gaza and was observed across the region, targeting the Axis of Resistance nations.

Although the probability of the situation spiraling further is highly unlikely at the time of publishing this article, due to the ceasefire announcement Regardless, the fragility of the agreement has left concerned nations on high alert, affecting business as usual.

Half a year back retaliation against the Axis led Israel to initiate airstrikes across Lebanon, which took the life of a Bangladeshi migrant, and further deterioration caused the return of 300-500 workers from the country, which employs hundreds of thousands of migrant workers.10

A significant portion of Bangladesh’s labor force (over 15 million people) works abroad, with a large concentration (70% of migrant workers) in the Middle East.11 A broader regional escalation could lead to economic slowdowns or unrest in Gulf countries.

This will prompt companies to cut jobs or delay hiring. Families dependent on this income would scale back spending, weakening demand for local goods and services. Any negative externalities on remittance earnings or flow have the potential to significantly skew our balance of payments, given that it has served as the only steady replenisher of the foreign reserve.

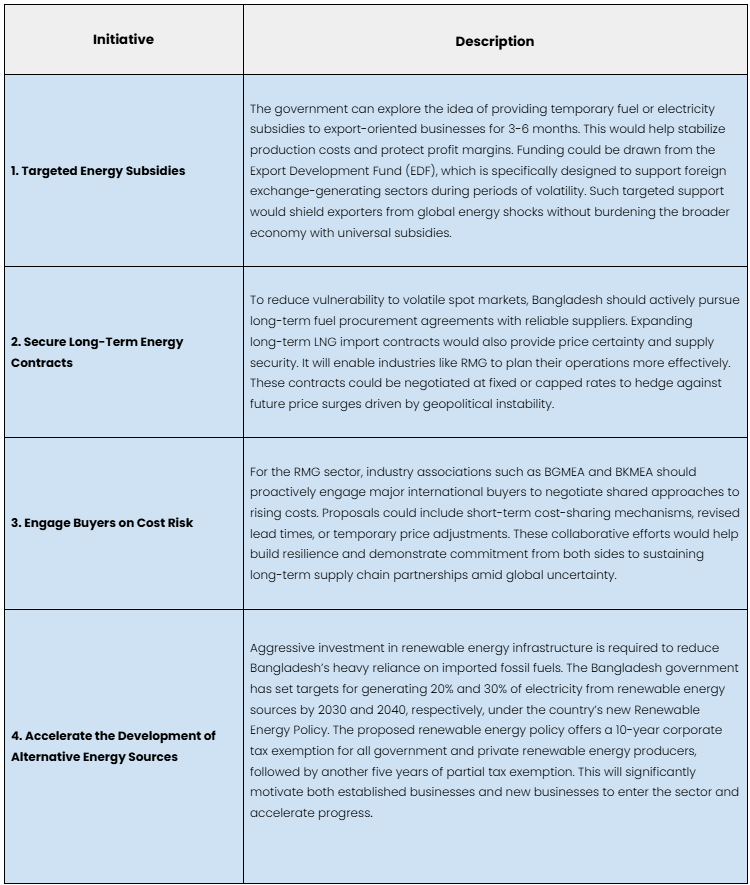

Although the Iran–Israel conflict is happening far from Bangladesh’s borders, its economic ramifications are immediate and real. Mitigating energy and shipping cost pressures, ensuring supply chain resilience, and collaborating internationally are essential to preserve the RMG sector’s competitiveness and safeguard national economic stability.

Shoumik Shahriar, Project Manager and Senior Business Consultant and Rakinul Islam, Business Consultant, at LightCastle Partners have co-authored the summary.

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights