GET IN TOUCH

- Please wait...

The Bangladesh economy continues to transition through turbulence, shaped both by global headwinds and domestic political turmoil. The pandemic disrupted supply chains, the Russia-Ukraine war triggered cost-push inflation, and shifting geopolitical strategies altered trade and investment flows. These factors have collectively slowed the economic momentum.

The most transformative event came in August 2024, when a movement over public sector job quotas culminated in regime change. While historical in nature, the transition created instability in law and order, while disrupting the business environment and curbing consumer spending.

Amid this uncertainty, businesses and investors have adopted a “wait-and-see” stance, holding back decisions until political stability and policy continuity are ensured under an elected government. This sentiment was reflected in the latest LightCastle Business Confidence Index 2024-25, where confidence remained subdued at +6.44.

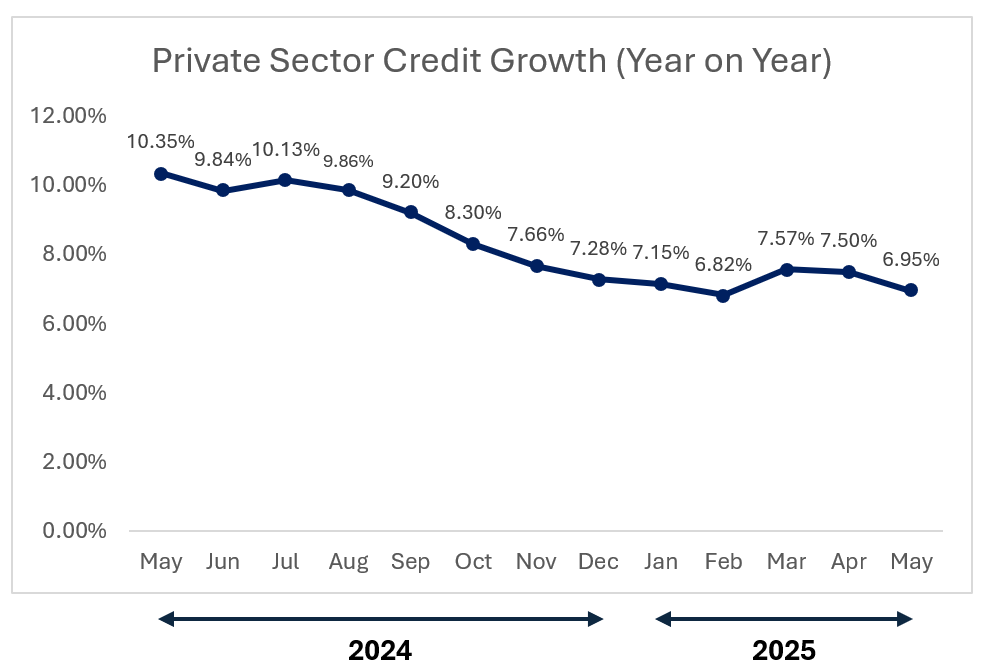

Sluggish private sector credit growth – 6.95% in May 2025, down from 10.35% in May 2024 [1] – further illustrates weak investment appetite. Industry leaders attribute this to persistent inflation, tight financial conditions, and delayed policy reforms.

The financial system has come under renewed pressure. Lending rates climbed to 9.0–15.5% in FY25 [2], while NPLs surged to BDT 345,765 crore [3]. While central bank-driven reforms and merger plans aim to improve sector resilience, the near-term effect has been tighter credit conditions, restricting liquidity for both businesses and households.

On the demand side, consumers remain constrained by inflation, borrowing costs, and political uncertainty. Industry experts in FMCG and consumer durables report declining sales, with households prioritizing essential goods and services over discretionary spending.

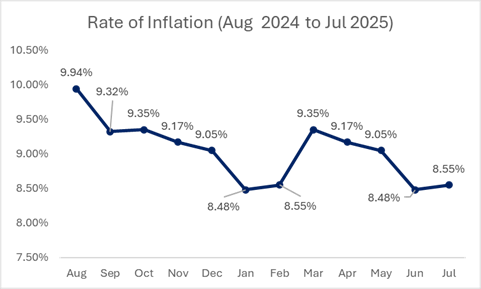

Inflationary pressures remain one of the key policy challenges. General inflation stood at 8.55% in July 2025, while food inflation remains at 7.56%. While the monthly inflation has reduced from the 11.66% peak in July 2024, average inflation over the past 12 months remained elevated at 10.03%.

To address demand-side inflation and stabilize the economy, Bangladesh Bank has maintained a contractionary monetary policy by tightening liquidity and raising interest rates. These measures are expected to remain until inflation stabilizes below the 8% threshold.

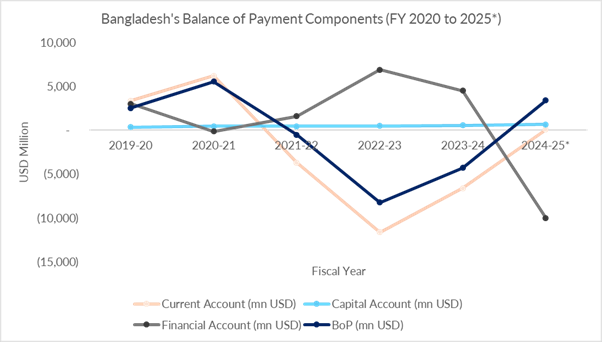

Bangladesh’s external balance has shown notable improvement. In the first seven months of FY25 (July–January), the overall Balance of Payments (BoP) deficit fell by nearly 75% year-on-year, offering relief to foreign exchange reserves and the exchange rate.

This turnaround was driven by:

However, underlying weaknesses persist. Lower imports, including capital machinery, signal weakening economic activities and investments. The balance of error and omission also expanded sharply, up 161% to USD 1.7 billion, reflecting significant unrecorded outflows.

Policy interventions, including contractionary monetary measures and the adoption of a crawling-peg exchange rate, have helped stabilize currency markets. But long-term resilience will depend on sustained inflows and stronger measures against illicit capital flight.

The World Bank recently downgraded Bangladesh’s FY25 growth forecast to 3.3%, down from 4.1% projected in January [4]. Political unrest and subdued investment were cited as key drivers.

For context, Bangladesh’s forecast lags regional peers such as Vietnam (4.0%) [5], Nepal (4.5%), and Bhutan (6.6%) underscoring the urgency of restoring investor confidence and accelerating policy reforms.

Bangladesh’s near- and medium-term outlook will hinge on several milestones:

Short Term

Medium Term

Bangladesh’s economy today stands at a crossroads displaying both resilience and vulnerability. External balances and remittances provide a cushion, yet structural challenges in banking, investment, and inflation remain pressing.

The immediate priority is to facilitate a smooth political transition that restores policy continuity in the short to medium term. In the medium term, preparing for LDC graduation and adapting to ESG-driven trade requirements will determine whether Bangladesh sustains growth momentum or risks further slowdown.

This article was authored by M.Rakinul Islam, a Business Consultant and Sadia Rahman Shupta a Business Analyst working in the Development & Management Consulting department at LightCastle Partners. For further clarifications, contact us here: [email protected]

[1] Economic Data, Bangladesh Bank

[2] Interest Rate of Scheduled Banks, Bangladesh Bank

[3] State of the Bangladesh Economy in FY24-25, CPD, May 2025

[4] South Asia Development Update, World Bank, April 2025

[5] East Asia and Pacific Economic Update, World Bank, April 2025

This article was originally published on the AmCham magazine.

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights