GET IN TOUCH

- Please wait...

Bangladesh’s micro, small and medium enterprises form the country’s economic backbone. However, there is a vast gap in MSME financing in Bangladesh. The World Bank states that 40 percent of the workforce constitutes formal SMEs, contributing about a quarter of GDP1 . Yet the sector is starving for affordable, formal finance. A press release by the IFC estimates an MSME financing gap of roughly USD 2.8 billion. 60 percent of the firms owned by women [2].

Structural frictions like informality, weak or non-existent credit histories, scarce collateral, high documentation costs and thin distribution for refinance schemes keep millions of viable enterprises on the margins of the formal financial system.

These are clearly not distant statistics that capture the reality of a few. Rather, they paint the everyday stories of a village grocery, a peri-urban garment upcycler, or a woman-led food stall living on modest daily receipts and no audited books. This often forces them to seek loans from mohajons. They are local lenders charging as high as 100% interest rates in a short cycle.

Unable to adhere to these unrealistic conditions, the MSME owners forcefully borrow from another mohajon. They operate in a perpetual debt cycle. MSME empowerment demands an imminent solution, and the best starting point would be closing the USD 2.8 billion gap [2]. And that requires two moves at once:

Creating an objective criterion that helps capture and benchmark real economic behavior and building the digital rails that let lenders safely use those signals at scale.

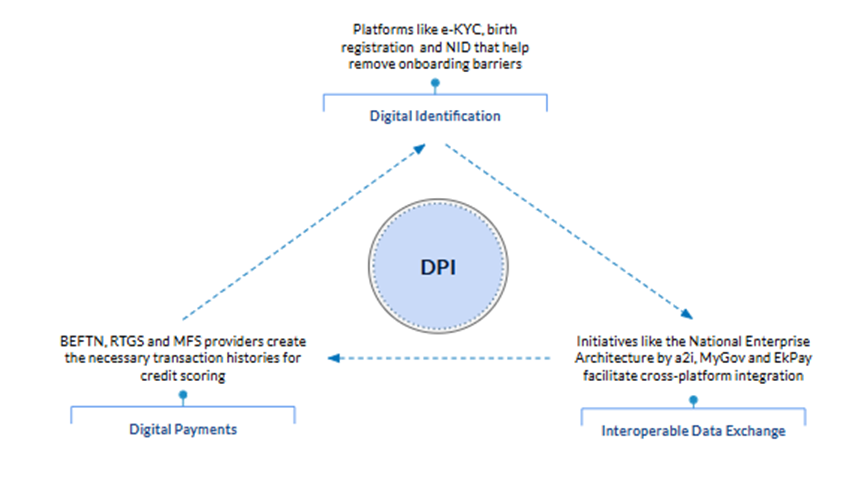

That is where Digital Public Infrastructure (DPI) becomes relevant. DPI consists of digital identity and e-KYC, interoperable payment rails, consented data exchange and portable registries. This addresses the exact frictions the MSME market faces. Identity removes onboarding barriers, payments create persistent transaction histories, a consent layer governs safe sharing, and a portable MSME registry ties the pieces together.

Bangladesh already has the raw ingredients. A National ID system, an active e-KYC regime, large mobile financial services players and national payment initiatives. But their real power is unlocked only when they work as an integrated ecosystem, i.e. they are interoperable.

Case studies from regional peers who stood at similar crossroads as Bangladesh today show how Digital Public Infrastructure (DPI) can close MSME financing gaps.

Aadhaar, UPI, and the Account Aggregator/OCEN frameworks spearheaded India’s digital stack. Allowing lenders to underwrite microloans as small as USD 60, which reduced friction and scaled last-mile reach [3]. India enabled over 40 million MSMEs to access formal credit in 2023, with total MSME credit volumes surpassing USD 480 billion and growing nearly 20% annually [4].

Similarly, Pakistan’s Raast instant payment system processed over USD 3.5 billion in just 16 days by late 2024. Creating transaction data trails that fintechs and microfinance banks leveraged to expand MSME credit access [5].

Sri Lanka also integrated its national digital ID (e-NIC) with the LankaPay payment switch. And it streamlined e-KYC and SME onboarding. While still emerging, these reforms are already reducing barriers and improving formal credit flows. and mark the first steps towards closing the MSME financing gap [6].

The examples show that when digital ID, interoperable payments, and consented data exchange are paired with regulation, MSME credit access can expand rapidly, even in economies with high informality.

Bangladesh’s private sector has been making progress concerning last-mile financial inclusion. The aim being to make credit accessible to all. BKash alone now supports tens of millions of customers and processes hundreds of millions of transactions every year. Its transaction footprint is a raw data asset for underwriting [7]. Recent reporting shows that City Bank’s digital nano-loan programmes, distributed through bKash, have scaled rapidly, disbursing around USD 190 million to roughly 950,000 users as of April 2025, demonstrating how payment footprints can be converted into credit at scale with low default rates [8].

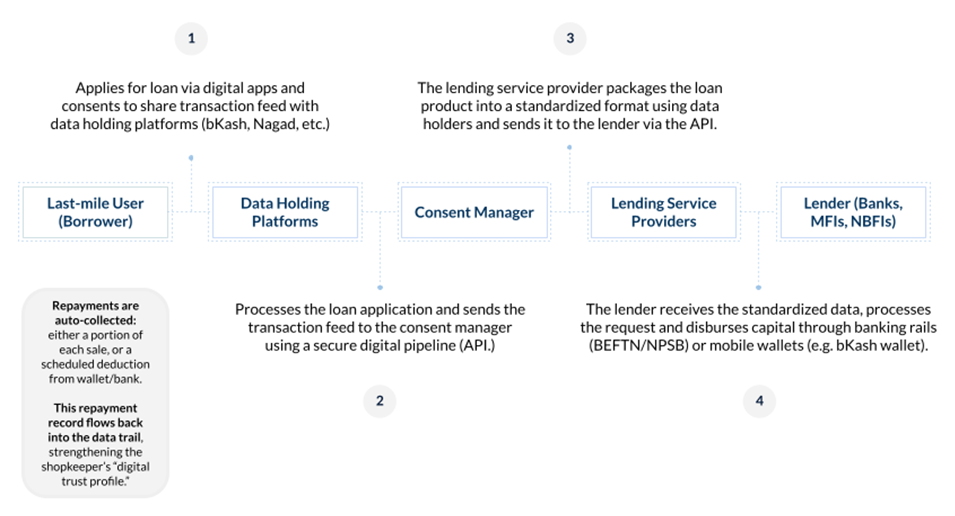

This demands the crux of the issue: what exactly must happen for a micro retailer who takes bKash and pays utility bills to be scored and funded within hours? The architecture consists five practical layers. Explanation is best using the following diagram:

As consent and standards sit at the centre of the architecture, the retailer’s data does not have to be “open.” It is shared only with permission, in a standardised format and with auditable trails. The end-to-end flow, from digital sale to consented payload to lender decision to disbursement, is facilitated through the same MFS rail, reducing paperwork and costs, speeding decisions, and preserving consumer control. Auto-collected repayments also bolster the creditworthiness of the MSMEs, generating more and more transaction feeds as time goes by.

But technology is only half the problem. Targeted onboarding support is the practical next step that makes DPI useful for the smallest, least digital enterprises. It is a sequence that comprises:

If implemented, these steps will create a virtuous loop: better data leads to cheaper underwriting, which leads to wider lending and a stronger business case for more merchants to onboard.

Bangladesh already holds a comparative advantage: huge MFS activity, broad NID coverage and active public actors. The path is therefore feasible, but it has to be deliberate.

The policy task is visible: formalising consented data frameworks, mandating common payload standards for payments and transaction data, using regulatory sandboxes to validate hybrid scoring models, and funding targeted, agent-led onboarding pilots that prioritise women-owned firms.

The prize of this is large; an infrastructure of trust that converts everyday digital behaviour into verifiable credit histories. That is how USD 2.8 billion of unmet MSME demand becomes not merely a policy problem but an opportunity to bring millions of small enterprises into formal finance and to unlock inclusive, durable growth.

This article was authored by Wasif Mahmud, Business Analyst at LightCastle Partners. For further clarifications, contact here: [email protected].

[1] Small and Medium Enterprises (SMEs) Finance — World Bank.

[2] IFC and Bangladesh Bank host a conference to ramp up SME financing. IFC press release.

[3] UPI product overview — NPCI.

[4] MSME credit surges threefold in a decade — Livemint.

[5] Pakistan’s Raast instant payment system success 2024.

[6] Sri Lanka e-NIC and LankaPay integration reforms.

[7] Bangladesh leads South Asia in mobile money growth — The Business Standard.

[8] How mobile wallets are driving the rise of digital nano loans — The Business Standard.

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights