Unlocking Climate Finance in Bangladesh: From Ambition to Execution

LightCastle Partners

March 4, 2026

Climate change is no longer a distant environmental concern for Bangladesh; it is an immediate macroeconomic and financial risk. Recurrent floods, cyclones, salinity intrusion, and erratic rainfall are already disrupting production, damaging infrastructure, and weakening livelihoods. As these impacts intensify, the need for effective climate finance in Bangladesh to support adaptation and mitigation is becoming increasingly urgent. The country already incurs an estimated USD 6.5 billion in annual economic losses due to environmental degradation.1

Bangladesh contributes less than 0.5 percent of global greenhouse gas emissions, yet among the most climate-vulnerable countries globally.2 According to the ADB forecast, Climate change could reduce Bangladesh’s GDP by 24.5 percent to as much as 77.9 percent3, while IOM estimates that one in seven Bangladeshis could be displaced by 2050.4

Addressing this challenge requires sustained, large-scale investment. Bangladesh is estimated to need over USD 200 billion in climate financing over the next two decades. Climate-related spending will need to rise to 3 percent of GDP by 2031 and 3.5 percent by 2041 to remain aligned with national targets.5 The immediate challenge in front of Bangladesh is translating targets into bankable pipelines and investable projects, and more importantly, managing the required financing.

What Is Climate Finance?

According to the United Nations Framework Convention on Climate Change, “Climate finance refers to local, national or transnational financing, drawn from public, private and alternative sources of financing, that seeks to support mitigation and adaptation actions that will address climate change.”6

In practical terms, climate finance spans a wide range of instruments, including grants, concessional loans, commercial debt, equity, guarantees, and risk-sharing mechanisms, deployed across both public and private sectors. Its defining feature is not the instrument itself, but the intent: reallocating capital toward activities that remain viable and competitive in a climate-constrained world.

The Global Climate Finance Landscape

Global climate finance has expanded significantly over the past decade, yet delivery continues to lag ambition. The USD 100 billion per year commitment first made in 2009 and reaffirmed under the Paris Agreement through 2025 marked an important political milestone.7 Subsequent announcements at COP26 and new pledges under G20 and EU frameworks reinforced global intent. However, while commitments have multiplied, financing to developing countries has remained inconsistent.

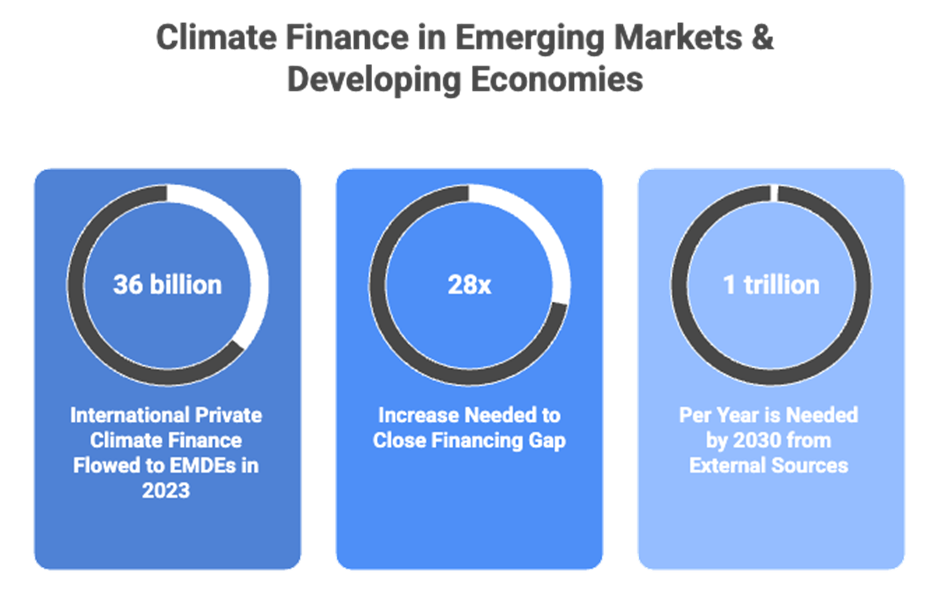

Figure 1: Climate Finance in EMDEs

According to the Climate Policy Initiative, global climate finance reached approximately USD 1.3 trillion per year in 2021–22.8 This represents more than a twofold increase over the past decade. Yet it remains far below the estimated USD 4–6 trillion required annually by 2030 to remain aligned with global climate goals.9 The composition of finance is also uneven. More than 90 percent of total flows are directed toward mitigation activities such as renewable energy, low-carbon transport, and energy efficiency, while less than 10 percent supports adaptation.10 This imbalance persists despite rising physical climate risks and escalating losses in climate-vulnerable regions.

Geographic concentration further compounds the challenge. Advanced economies capture more than three-quarters of total climate finance, while emerging and developingeconomies (excluding China) receive less than 15 percent of global flows,11 despite bearing the highest exposure to climate impacts. Private finance is even more concentrated in low-risk markets characterized by policy certainty, deep capital markets, and large, standardi zed transactions. Countries with fragmented project pipelines, regulatory uncertainty, and higher perceived execution risk struggle to attract commercial capital at scale.

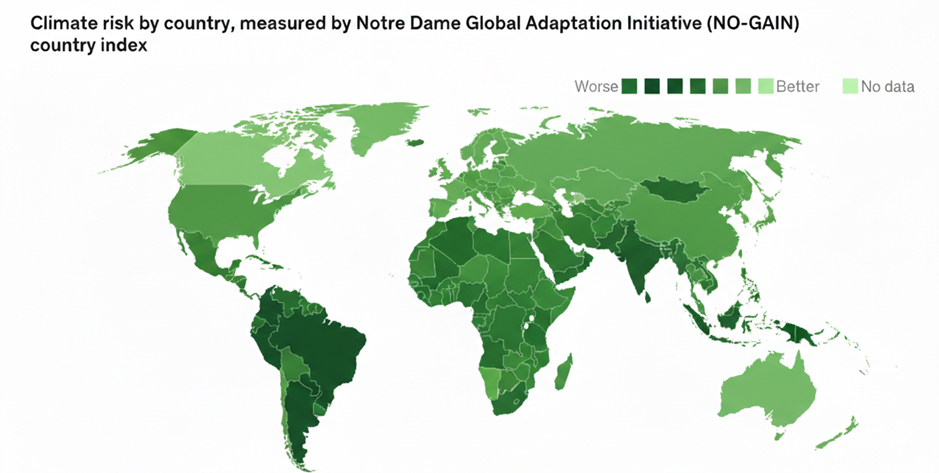

Figure 2: Climate Risk by Country12

At the same time, private sector commitments appear substantial on paper. The Glasgow Financial Alliance for Net Zero represents over USD 130 trillion in assets committed to net-zero alignment by 2050.13 However, much of this capital remains concentrated in developed markets or invested in lower-risk asset classes. The core constraint is the absence of bankable pipelines, credible policy frameworks, and effective risk-mitigation mechanisms in emerging economies. Large institutional investors require scale, standardization, and predictable returns, conditions that many climate-vulnerable markets have yet to systematically provide.

The global climate finance landscape, therefore, presents a paradox. Ambition has been institutionalized through international agreements and high-level commitments, yet deployment remains uneven and structurally constrained. Capital exists at an unprecedented scale. What remains unresolved is the translation of that capital into structured, de-risked, and investable opportunities in the regions that need it most.

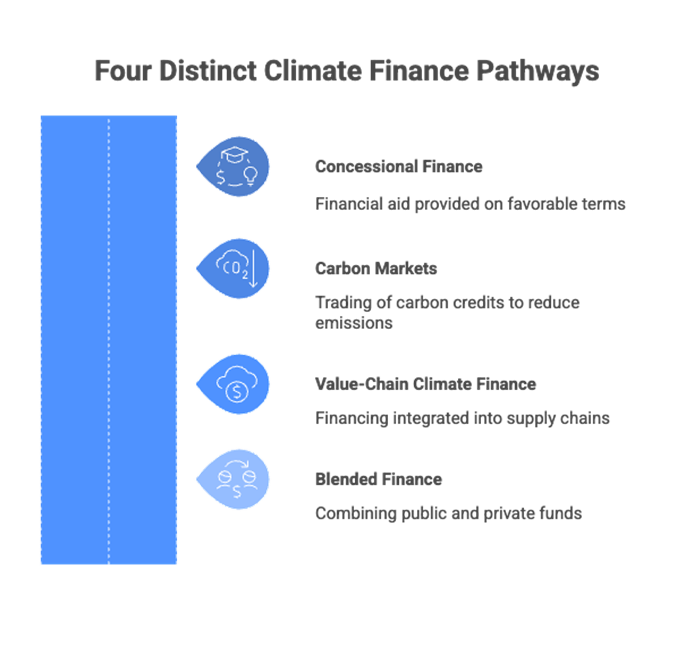

Four Distinct Climate Finance Pathways

Climate finance is often discussed as a single pool of capital, but in practice, it moves through distinct channels, each with its own incentives and constraints. Four pathways dominate today’s landscape: concessional finance, carbon markets, value-chain finance, and blended finance.

Each pathway emerged to solve a specific market gap, whether addressing high risk, pricing externalities, responding to commercial pressure, or crowding in private capital. Yet none, on its own, has delivered capital at the scale required.

Figure 3: Four Distinct Climate Finance Pathways

Concessional Finance

Concessional finance refers to public or donor funding provided on below-market terms. It includes grants, soft loans, and highly subsidized credit from multilateral climate funds and development partners. This form of finance is essential for adaptation, resilience, and early-stage mitigation projects that are too risky or not immediately profitable for private investors.

Carbon markets aim to mobilize private capital by placing a price on emissions reductions. Projects that reduce or avoid greenhouse gas emissions generate tradable carbon credits, which can be sold to governments or companies seeking to offset emissions.

In theory, this creates a market-based incentive for climate investment. In practice, the results have been mixed. Compliance markets have faced price volatility and uneven participation across countries. Voluntary carbon markets have struggled with credibility concerns and low prices, often insufficient to materially influence investment decisions. Carbon markets can complement climate finance, but they require strong regulatory frameworks and transparent monitoring systems to function effectively.

Value-Chain Climate Finance

Value-chain climate finance is driven by commercial relationships rather than public funding. Large global buyers, particularly in export sectors, increasingly require suppliers to meet environmental standards. To maintain market access, suppliers invest in cleaner technologies, energy efficiency, and sustainability upgrades.

In some cases, buyers support these upgrades directly through sustainability-linked financing, preferential contracts, or technical assistance. This pathway tends to move faster than public finance because it is tied to competitiveness and regulatory compliance. Where export pressure is strong, value-chain finance can become a powerful driver of climate investment.

Blended Finance

Blended finance combines concessional capital with private investment to improve the risk-return profile of climate projects. Public or donor funds are used strategically through instruments such as guarantees, first-loss capital, subordinated debt, or technical assistance to reduce perceived risks and enhance bankability.

The objective is to mobilize private capital that would not otherwise flow into high-risk or early-stage climate investments. Rather than substituting for commercial funding, concessional resources are deployed to catalyze it.

Blended finance has demonstrated its ability to unlock private capital, but its overall impact remains limited relative to the scale of climate investment required. Many structures are transaction-driven, which raises costs and slows replication. To meaningfully address large financing gaps, blended finance must shift from isolated deals to standardized, programmatic platforms capable of deploying capital at scale.

Bangladesh’s Climate Finance Architecture Today and Policy Framework

Bangladesh’s climate finance system remains predominantly public- and policy-led, with limited private capital mobilisation. Developing climate resilience will require USD 8.5 billion per year, with USD 6.0 billion per year from external sources or international climate funds and development partners.14 But unfortunately, actual public spending is far smaller. In FY2023–24, climate-relevant budget allocations were at USD 370 million.15

Multilateral and bilateral partners account for a significant share of deployed climate finance, particularly for adaptation and resilience. To date, approved funding includes USD 464 million from the Green Climate Fund,16 and USD 190 million from the Climate Investment Funds,17 . These flows are largely concessional and project-specific, with long preparation and disbursement cycles that limit speed and scale.

Policy/Framework

Key Purpose/Objective

Sustainable Finance Policy (2020; Updated in 2023)

Direct capital into green investments; encourage financial institutions to incorporate ESG considerations into operations

ESRM Guidelines (Environmental and Social Risk Management) (2022)

Establish risk management framework for banks assessing environmental and social impacts of lending activities

Green Bond Financing Policy (2022)

Attract private capital for clean energy, efficiency, and waste reduction through standardized bond instruments

Guideline on Sustainability and Climate-related Financial Disclosures (2023)

Mandate financial institutions to disclose sustainability performance and climate-related risks in their operations

Guideline on Climate Risk Management for Banks and Finance Companies (2025)

Integrate climate risk assessment into financial sector operations and lending decisions for enhanced resilience

Table 1: Key Climate Finance Policies/Frameworks

On the domestic financial side, Bangladesh Bank has been the primary policy driver. Its Sustainable Finance Policy and Environmental and Social Risk Management (ESRM) Guidelines require banks and NBFIs to screen environmental and social risks and report sustainable finance exposure.18

Financing Mechanism

Allocation

Green Transformation Fund (GTF)

USD 200m, EUR 200m, BDT 50b

Technology Development or Upgradation Fund (TDF or TUF)

BDT 10b

Environmental Refinance Scheme

BDT 4b

Table 2: Key Financing Mechanisms

The USD 200 million Green Transformation Fund provides concessional foreign-currency financing for cleaner production in export sectors, alongside smaller refinancing windows for renewable energy and green SMEs. While these facilities improve liquidity, they represent a small share of total credit and have not yet crowded in private capital at scale.

Capital market participation remains minimal. The bond market, representing 11.63 percent of GDP, limits access to long-term green capital.19 This bond market is largely government treasury bond driven, which represents 11.44 percent of this 11.63 percent, and only 0.19 percent comes from corporate bonds. In India, the bond-to-GDP ratio is 70 percent.20 As a result, long-term institutional investors play a negligible role in climate finance.

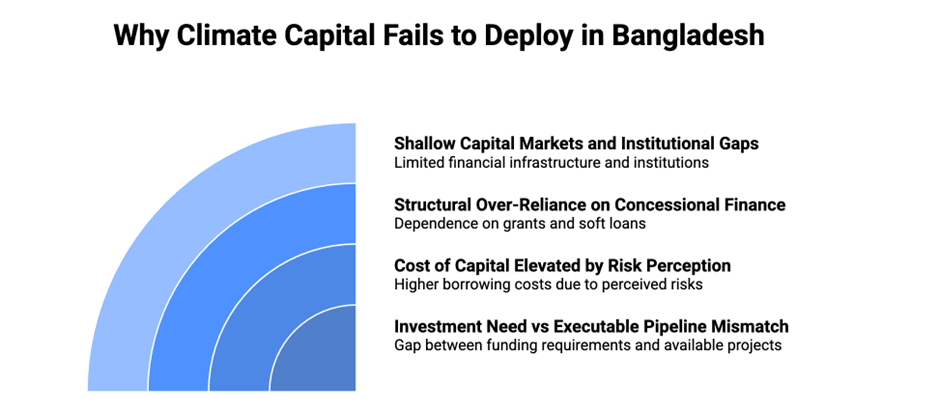

Why Climate Capital Fails to Deploy in Bangladesh

Figure 5: Why Climate Capital Fails to Deploy in Bangladesh

Investment Need vs Executable Pipeline Mismatch

Bangladesh’s climate strategies imply long-term investment needs of approximately USD 200 billion in the next two decades.21 Yet annual public climate allocations remain limited, and most interventions are structured as small, standalone projects. Many local climate initiatives lack the scale and structure required to attract large pools of private capital. This absence of effective aggregation mechanisms constrains scale and limits capital deployment.

Cost of Capital Elevated by Risk Perception

Climate assets generate long-term BDT-denominated cash flows, while much financing is USD-linked. Currency volatility and sovereign risk premiums increase financing costs significantly above global benchmarks. Limited climate data and inconsistent disclosure further raise perceived risk, leading to conservative pricing or outright exclusion. As a result, private climate finance remains marginal relative to concessional flows.

Structural Over-Reliance on Concessional Finance

Approved commitments from major global climate funds to Bangladesh run into the billions of dollars, but these flows remain largely project-based and slow-moving. Domestic facilities such as the Green Transformation Fund (USD 200 million) and refinancing windows have improved liquidity, yet they reinforce a refinancing-dependent model. As a result, private capital participation remains limited, and underlying risk-allocation dynamics remain largely unchanged.

Shallow Capital Markets and Institutional Gaps

Bangladesh’s bond market represents only 11–12 percent of GDP, compared to over 70 percent in peer economies like India.22 Corporate bonds account for less than 0.2 percent of GDP, limiting long-tenor financing. Sustainable finance disbursements have increased to BDT 149,819 crore in Q1 2025,23 but remain concentrated and largely compliance driven. Institutional capacity for aggregation, structuring, and climate risk pricing remains underdeveloped.

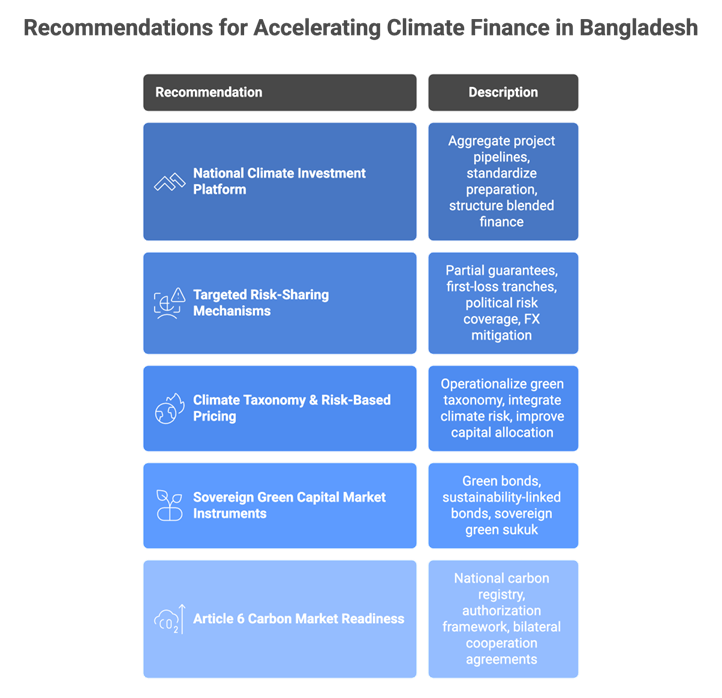

Recommendations for Accelerating Climate Finance in Bangladesh

Figure 6: Recommendations for Accelerating Climate Finance in Bangladesh

Establish a National Climate Investment Platform

Bangladesh’s climate strategies imply investment needs exceeding USD 200 billion over the next two decades, yet projects remain fragmented. A centralized Climate Investment Platform should aggregate renewable energy, industrial decarbonization, adaptation, and water infrastructure into standardized, finance-ready portfolios.Common documentation templates, risk frameworks, pipeline visibility, and blended finance windows would reduce transaction costs and improve scale. Aggregation is essential to attract institutional capital and move beyond project-by-project financing.

Comparative lesson: India’s SECI-led renewable auctions aggregated projects and standardized contracts, lowering costs and crowding in large-scale private investment.24

Deploy Targeted Risk-Sharing Mechanism to Reduce Risk

Currency volatility, sovereign risk premiums, and regulatory uncertainty elevate financing costs. Public resources should therefore prioritize catalytic de-risking rather than direct project substitution.

Partial guarantees, first-loss tranches, political risk coverage, and selective FX mitigation tools can materially improve bankability while preserving fiscal space. Risk-sharing should be targeted at early-stage and high-impact sectors.

Comparative lesson: Vietnam’s renewable energy expansion was catalyzed by sovereign-backed offtake through Vietnam Electricity (EVN), where long-term government-supported PPAs reduced counterparty and revenue risk, compressed financing spreads, and enabled rapid private capital mobilization without large-scale public project substitution.25

Operationalize Climate Taxonomy and Risk-Based Pricing

Bangladesh has sustainable finance policies in place, but climate risk is not yet systematically embedded in lending decisions or credit pricing. A national climate taxonomy aligned with international standards would guide asset classification, disclosure, and portfolio alignment.

More importantly, climate performance must influence cost of capital. Risk-based pricing mechanisms should reward transition-aligned investments and reflect exposure to climate-related risks.

Comparative lesson: Malaysia’s Climate Change and Principle-Based Taxonomy strengthened data consistency and investor confidence by requiring financial institutions to classify exposures based on environmental impact.26

Deepen Capital Market Participation Through Sovereign Green Instruments

Bangladesh’s bond market remains shallow relative to GDP, limiting long-term financing capacity. A Sovereign Green and Transition Bond Framework, endorsed by the Ministry of Finance and Bangladesh Bank, would anchor standards and create benchmarks for corporate issuances.

Islamic finance instruments such as green Sukuk can expand the domestic and regional investor base, while sustainability-linked bonds can align borrowing costs with climate performance targets.

Comparative lesson: Chile’s 2022 Sovereign Sustainability-Linked Bond (USD 2 billion) linked the country’s borrowing costs to the achievement of national emissions reduction and renewable energy targets, creating a structure where stronger sustainability performance translates into lower financing costs.27

Accelerate Readiness for Article 6 Carbon Markets

Article 6 of the Paris Agreement enables countries to trade verified emission reductions through internationally transferred mitigation outcomes. For Bangladesh, operationalizing Article 6 could unlock a new channel of private capital by monetizing emissions reductions from renewable energy, industrial efficiency, forestry, and blue carbon projects.

To participate effectively, Bangladesh must establish a clear national carbon registry, effective measurement and verification systems, and corresponding adjustment procedures to ensure environmental integrity. Policy clarity and transparent governance will be critical to attracting private developers and long-term buyers.

Comparative lesson: Ghana operationalized Article 6 through bilateral agreements and a national registry framework, providing regulatory certainty that enabled private sector participation.28

Climate finance is not constrained by a lack of global capital. Significant pools of capital are already earmarked for climate-aligned investments worldwide. Yet for Bangladesh, the challenge is twofold: limited access to affordable capital and an insufficient pipeline of bankable, risk-mitigated projects. The constraint is structural. Without stronger de-risking mechanisms, clearer risk pricing, and scalable investment platforms, global liquidity does not automatically translate into domestic flows. Bangladesh’s growth and competitiveness will depend on how effectively it can attract and deploy capital at scale.

Author

This article was authored by Shoumik Shahriar, Senior Business Consultant & Project Manager at LightCastle Partners. For further clarifications, contact here: [email protected].

References

The Business Standard. (2024, February 18). Bangladesh needs billions to go green, draft strategy says.

Climate Watch. (2023). Historical greenhouse gas emissions. World Resources Institute.

Asian Development Bank. (2024). Asia-Pacific climate report 2024. Asian Development Bank.

International Organization for Migration. (2023, November 30). Bangladesh redoubles efforts to include migration and human mobility in climate change discussions

The Business Standard. (2024, February 18). Bangladesh needs billions to go green, draft strategy says.

United Nations Framework Convention on Climate Change. (n.d.). Introduction to climate finance.

United Nations Framework Convention on Climate Change (UNFCCC). (2009). Report of the Conference of the Parties on its fifteenth session, held in Copenhagen from 7 to 19 December 2009 (Copenhagen Accord).

Climate Policy Initiative. (2023). Global landscape of climate finance 2023. Climate Policy Initiative.

Climate Policy Initiative. (2023). Global landscape of climate finance 2023. Climate Policy Initiative.

Climate Policy Initiative. (2025). Global landscape of climate finance 2025: Summary handout. Climate Policy Initiative.

Climate Policy Initiative. (2025). Global landscape of climate finance 2025: EMDE spotlight summary handout. Climate Policy Initiative.

McKinsey & Company. (2023). Solving the climate finance equation for developing countries.

Glasgow Financial Alliance for Net Zero. (2021). Amount of finance committed to achieving 1.5°C now at scale needed to deliver the transition.

Centre for Policy Dialogue. (2023, November). Review of climate budget and recommendations for climate public finance management in Bangladesh. Centre for Policy Dialogue.

The Business Standard. (2023, June 1). Climate-related allocation decreases slightly in budget for FY2024.

Green Climate Fund. (2024). Bangladesh country portfolio.

Climate Investment Funds. (2024). Bangladesh country profile.

The Business Standard. (2024). Why the future lies in sustainable finance.

The Financial Express. (2024, December 11). Bond market largely remains untapped.

Jiraaf. (2025). Indian bond market 2025 trends.

World Bank. (2024). Bangladesh country climate and development report. World Bank Group.

The Financial Express. (2024, December 11). Bond market largely remains untapped.

Alo, J. N. (2025, August 31). Why future lies in sustainable finance. The Business Standard.

Rouwenhorst, K. (2025, August 6). Renewable ammonia price discoveries: A closer look at the H2Global and SECI auctions. Ammonia Energy.

Vietnam: Solar competitive bidding strategy and framework. World Bank Group.

Bank Negara Malaysia. (2021). Climate change and principle-based taxonomy

Sy, R. J. (2022, March 4). World’s 1st sovereign sustainability-linked bond issued by Chile. S&P Global Market Intelligence.

Climate finance refers to funding from public, private, or international sources that supports activities aimed at addressing climate change, including both mitigation and adaptation efforts.

Why does Bangladesh need climate finance?

Bangladesh is highly vulnerable to climate change, facing floods, cyclones, and rising salinity, which damage infrastructure, disrupt livelihoods, and cause significant economic losses each year.

What are the main sources of climate finance?

Climate finance comes from public funds, private investment, and international sources such as multilateral climate funds and development partners, often through instruments like grants, loans, equity, and guarantees.

What challenges does Bangladesh face in accessing climate finance?

Key challenges include a lack of large, investable projects, high perceived risks, reliance on concessional funding, and underdeveloped capital markets, which limit the flow of private investment.

What are climate finance pathways?

Concessional finance, carbon markets, value-chain finance, and blended finance.