GET IN TOUCH

- Please wait...

Globally, the concept of circularity, guided by the 3Rs—Reduce, Reuse, and Recycle—is reshaping how we think about waste and sustainability. Circular financing plays a key role in this shift, providing the funds to help businesses embrace circular practices and reinvent their operations. This type of financing is not only essential for fostering innovation and sustainability, but also for ensuring that these practices can be scaled and integrated into mainstream economic activities.

However, to truly accelerate circular financing, comprehensive policy reforms are needed. By implementing strategic policies, governments can create a favorable investment climate, mitigate financial risks for businesses, and ensure that circular economy initiatives receive the support they need to thrive.

In Bangladesh, financing for the circular economy falls under the broader category of Sustainable Finance. According to Bangladesh Bank, sustainable finance means providing financial services that consider environmental, social, and governance (ESG) factors to support businesses and benefit society as a whole.

Green finance is a smaller piece of this puzzle, focusing specifically on funding projects that help reduce environmental damage. This includes funding for green technologies, activities, products that meet any of the 6 environmental objectives mentioned in the EU Taxonomy Regulation:

1) Climate change mitigation

2) Climate change adaptation

3) Sustainable protection of water and marine resources

4) Transition to a circular economy, waste prevention and recycling

5) Pollution prevention and control

6) Protection and restoration of biodiversity and healthy ecosystems

There are several green finance avenues, such as the Refinance Scheme for Green Finance, Green Transformation Fund (GTF), Technology Development Fund (TDF), Green Climate Fund, and many other international funds available to support the green revolution in our industry. Some of the sectors prioritized in the green finance landscape include RMG, renewable energy, green infrastructure, energy and resource efficiency, liquid and solid waste management, recycling, environmentally friendly brick production, green agriculture, and green CMSMEs (Cottage, Micro, Small, and Medium Enterprises).

However, most of these funds are primarily targeted at large corporations. Ironically, it is SMEs that often require green funding the most. This is because their facilities tend to be inefficient, employ outdated, carbon-intensive technologies, and are more likely to contribute to pollution and other environmental concerns.

| Policies and Guidelines | Financing schemes |

| Green Banking Policy (2011) | Refinance Scheme for Environment Friendly Products/Projects/Initiatives |

| Sustainable Finance Policy (2016): | Green Transformation Fund (GTF) |

| Guidelines on Environmental and Social Risk Management (ESRM) (2017 and 2022) | Technology Development/Up-gradation Fund |

| Green Bond guidelines | |

| SME Policy 2019; Bangladesh Bank Policies on MSME Financing; Bangladesh Bank’s provisions for women-led/owned SMEs | SME Refinance Scheme |

2. Guidelines on Environmental and Social Risk Management (ESRM) (2017 and 2022): Bangladesh Bank issued updated Environmental and Social Risk Management (ESRM) Guidelines for banks and financial institutions in 2017. These updated guidelines include social issues and measurement tools, including an Environmental and Social Risk Assessment Tool. The 2022 update includes a comprehensive list of product/initiatives of Green Finance for banks and FIs.

| Textile & Apparel | Cement Manufacturing | Tanning & Leather | Ceramic Tile & Sanitary Ware | Pharmaceutical |

| Power | Fertilizer Manufacturing | Pulp & Paper | Steel Re-rolling | Shipbreaking |

3. Refinance Scheme for Green Products, Initiatives, and Projects: Bangladesh Bank has introduced a revolving fund of BDT 4 Bn for 94 green products with an aspiration of building a sustainable future for the country. The Central Bank will charge commercial banks an interest rate of 1% on loans issued under this scheme, with the possibility of adjusting this rate periodically. Banks will use the 1% as a base rate when setting interest rates for clients and can add a maximum margin of 4% to this base rate.

4. Green Transformation Fund (GTF): The scheme allows all export-oriented industries to import machinery belonging to (i) Water use efficiency in wet processing (ii) Water conservation and management (iii) Waste management (iv) Resource efficiency and recycling (v) Renewable energy and Energy efficiency (vi) Heat and temperature management and (vii) Air ventilation and circulation efficiency category. The tenure of the loan will be 5- 10 years with a one-year grace period.

| Major funds for financing sustainable/green projects | |||

| Name | Year of impl. | Disbursed amount | Allocated amount |

| Refinance Scheme for Islamic Banks & Financial Institutions for Investment in Green Products/Initiatives | 2018 | – | BDT 1.25Bn |

| Green Transformation Fund (GTF) | 2016 | USD 141 Mn + EUR 71 Mn + BDT 4.56 Bn | USD 200Mn + EUR 200Mn + BDT 50Bn |

| Technology Development/Up-gradation Fund | 2021 | BDT 4.16 Bn | BDT 10 Bn |

5. SME Refinance Scheme: In 2023, BB doubled the size of the refinance scheme for SMEs to BDT 30 Bn. Men will be subject to an interest rate of 7%, while women will benefit from a reduced interest rate of only 5%. Additionally, banks can access funds from the central bank at rates of 0.5% for women and 3% for men.

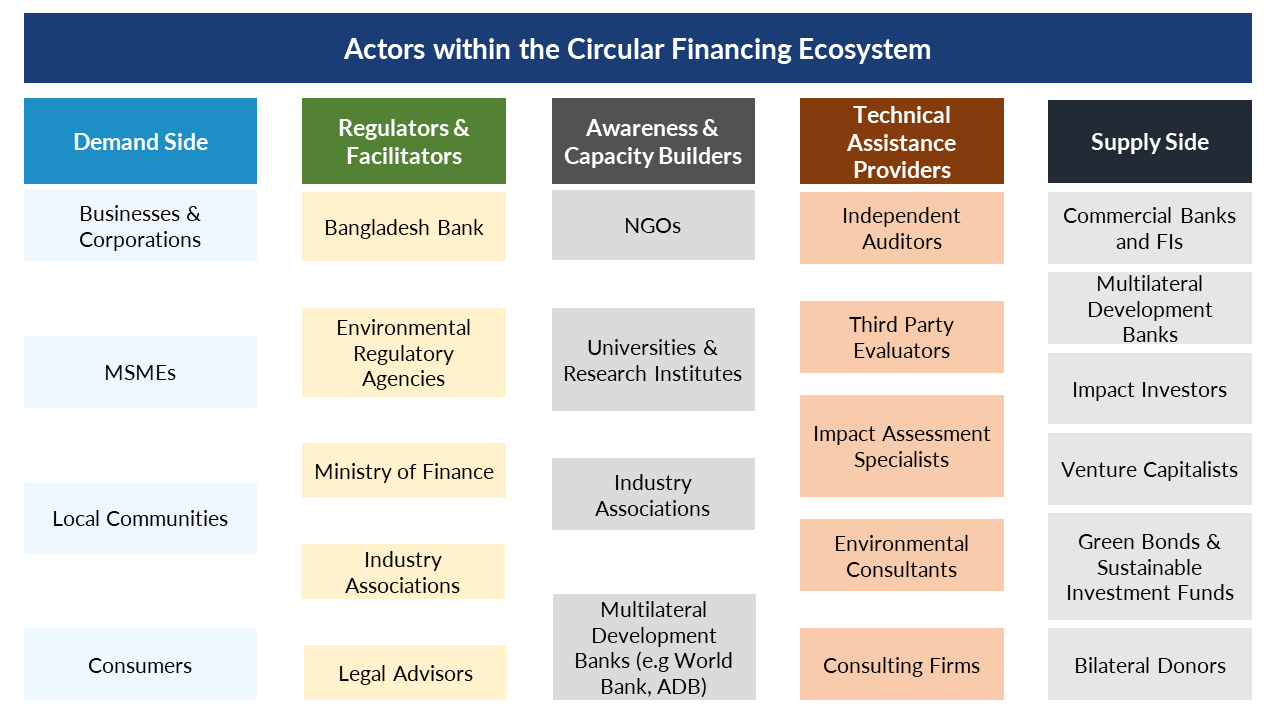

Businesses and corporations implement circular economy practices and apply for financing to support sustainable projects, while small and medium enterprises (SMEs) engage in innovative circular economy practices and seek funding to scale their operations. Local communities participate in and benefit from circular economy projects, especially in rural and underserved areas. Consumers drive demand for sustainably produced goods and services.

The Bangladesh Bank (BB) sets guidelines and policies for sustainable and green financing, ensuring regulatory compliance, and the Ministry of Finance develops and implements fiscal policies that support circular financing. Environmental regulatory agencies oversee environmental compliance and promote sustainable practices, while industry associations advocate for the industry-wide adoption of circular economy principles and support members in accessing financing. Legal advisors ensure all legal aspects of the financing agreement are clear and complied with.

Commercial banks provide loans and financing for circular economy projects, and development banks offer funding and technical support for large-scale sustainable projects. Impact investors provide funding for projects that deliver both financial returns and positive environmental impact, while venture capitalists invest in startups and innovative companies focusing on circular economy solutions.

Green bonds and sustainable investment funds offer alternative financing mechanisms for large-scale circular economy projects. Multilateral development banks (e.g., World Bank, ADB) offer financing and capacity-building support for sustainable projects, and bilateral donors provide grants and funding for specific circular economy programs.

Independent auditors conduct pre-approval assessments, ensuring the project’s feasibility and alignment with circular economy principles. Third-party evaluators perform mid-term evaluations to assess the project’s progress and compliance with financing conditions, while impact assessment specialists carry out impact assessments to evaluate the long-term benefits and sustainability of the project. Environmental consultants provide expertise in assessing the environmental impact of the project and ensuring compliance with regulatory standards. United Nations agencies (e.g., UNDP, UNEP) provide technical assistance, funding, and policy support for circular economy initiatives.

Non-governmental organizations (NGOs) advocate for sustainable practices and provide support for community-based circular economy projects. Universities and research institutes conduct research on circular economy practices and develop innovative solutions. Industry associations advocate for the industry-wide adoption of circular economy principles and support members in accessing financing. Multilateral development banks (e.g., World Bank, ADB) offer capacity-building support for sustainable projects.

In Bangladesh, green projects face hurdles due to their perceived risk and inadequate profitable track record, deterring investors and banks. Such projects typically have longer payback periods, creating a maturity gap from lenders’ perspective. Specifically, MSMEs necessitate tailored green finance assistance, potentially encountering challenges associated with inadequate collateral or historical instances of non-performing loans. While large corporations can afford to finance the circular transition through their retained earnings or other internal sources, SMEs are often dependent on external financing to adopt circularity.

As per Sustainable Development Goals (SDGs) and Nationally Determined Contributions (NDCs), the finance of such enterprises has to be a sustainable one with its lion’s share being green finance. However, until 2022, only 5.1% of Green Finance was allocated to Green CMSMEs. In addition, most of the green funds in Bangladesh are only for purchasing machines or tangible assets while SMEs might require other support as well. Overall, the barriers to accessing finance include stiff lending policies with high collateral security requirements, small project ticket sizes, and high transaction costs.

Next, there is quite a deficit in the technical expertise required to evaluate and manage green financing projects. Financial institutions often lack the necessary skilled personnel to assess environmental impacts and the viability of green projects effectively. Besides, the supporting infrastructure, such as renewable energy installations or waste management systems, is underdeveloped. Coupled with a market that is not fully ready to transition to greener alternatives due to cost concerns or lack of availability, this creates a significant barrier to the uptake of green finance.

The foremost obstacle in advancing circular finance is the issue of greenwashing. For instance, green bonds may be issued with the stated purpose of funding environmentally beneficial products, yet some of the proceeds might end up financing projects that do not meet environmental standards. In other words, there needs to be a robust mechanism in place to monitor the actual environmental impact of financed projects.

The financial sector can capitalize on the circular economy opportunity by leveraging or adapting existing products and services. Currently, developing countries represent only $1.6 Bn of the estimated $33 Bn in outstanding green loans. However, this segment of the market is expected to surpass the growth rate of the green bond market in the short term.

Currently, Bangladesh’s bond market is dominated by government bonds, with corporate debt relatively underdeveloped. But Pran Agro Limited (PAL) issued their first green bond with a face value of BDT1.5 billion to finance their agro-recycling, organic farming alongside environmental improvements in its manufacturing operations.

Case study 1: Intesa Sanpaolo – a top banking group in Europe – has long been committed to circular economy (CE), as manifested by its distinctive partnership with the Ellen MacArthur foundation. Together, they have identified criteria for assessing the level of circularity of the initiatives proposed by companies.

With a view to supporting businesses active in circular transition, the group allocated 8 Bn Euro as part of their 2022-2025 Business Plan. They offer five distinct products tailored for SMEs, covering areas such as ESG, Climate Change, and Agribusiness. In 2023, the group introduced a product specifically for businesses opting to invest in renewable energies. This loan features a subsidized rate and offers an extra incentive if the business directs a portion of the energy generated, which isn’t self-consumed, to the Renewable Energy and Communities (CER).

Case study 2: India has adopted a sector-specific financial institution (FI) strategy to meet its net zero commitment by 2070. For instance, REC Limited and Power Finance Corporation (PFC) leverage their deep understanding of the Indian power sector to develop innovative financial products tailored to the specific needs of transition projects. REC has successfully raised USD 450 Mn from international markets through green bonds. These funds are directed towards financing solar, wind, and meeting renewable purchase obligations. Furthermore, these FIs contribute to the implementation of green initiatives by offering technical assistance and training to project developers.

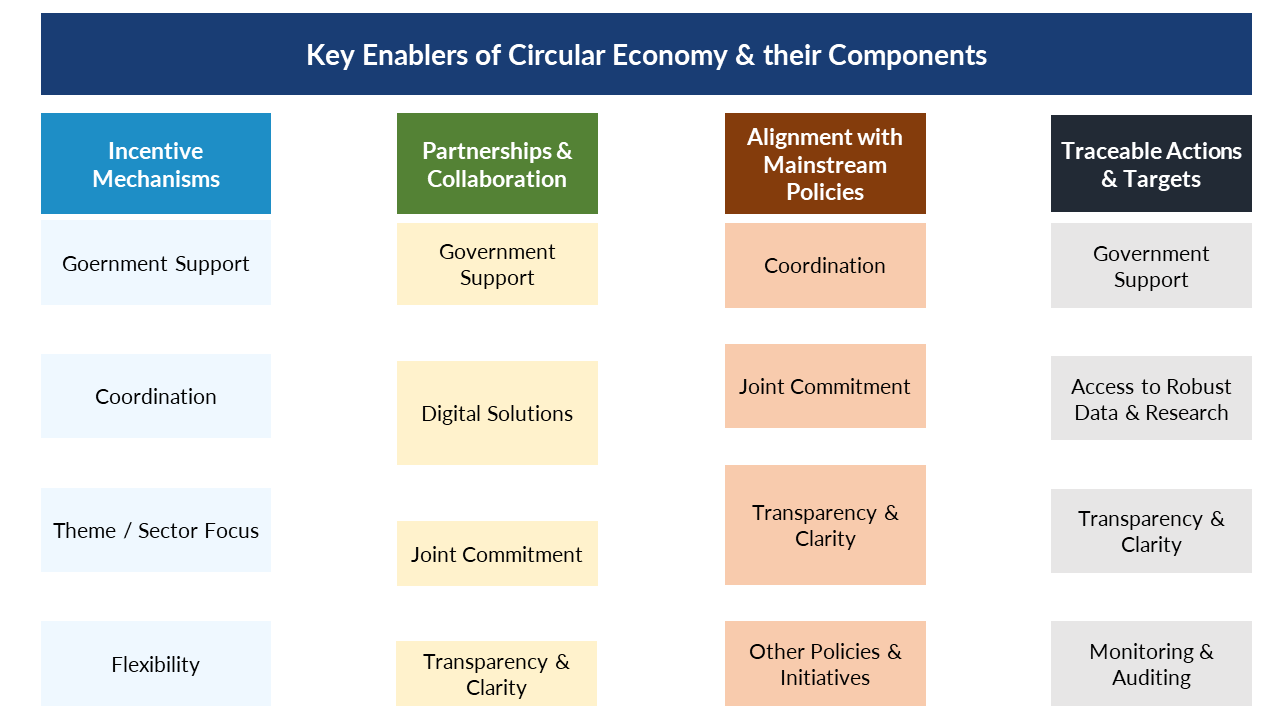

The World Business Council for Sustainable Development identifies 4 key policy enablers after an in-depth review of the circular economy policies. By identifying these key enablers, policymakers and businesses can better understand how and why these enablers are effective in expanding circular economy implementation.

Both the Bangladesh Sustainable Finance and Bangladesh Green Refinance policies specify particular technologies and products, deviating from a more comprehensive taxonomy. This targeted approach may pose challenges in financing cutting-edge technologies like energy storage or emerging renewable sources such as geothermal or tidal energy.

Notably, Bangladesh’s policies lack explicit references to substantial impact measurements on emissions, a stark contrast to the MDB Taxonomy’s stringent criteria. In addition, while green finance definitions are similar in sectors like renewable energy and eco-friendly buildings, they vary for sectors such as nuclear power, noise reduction, and carbon capture, which depend on the country-specific context.

MSMEs play a crucial role in the domestic economy, serving as vital backward linkage players for larger industries. Sectors such as light engineering, shipbuilding, and footwear are prime examples. To fully close the loop, these enterprises need to be integrated within the circular ecosystem, which necessitates both technical and financial support.

Current financial policies backing up MSMEs include a credit guarantee scheme facility, a loan facility at a maximum of 7% for male entrepreneurs, a loan facility at a maximum of 5% for women entrepreneurs, among others. In 2004, the Central Bank introduced a refinancing scheme named the “Small Enterprise Refinance Scheme” which started off with 1 Bn and currently stands at BDT 30 Bn. While 100% of refinancing is provided against disbursement of both working capital and term loans under this scheme, there is no particular green finance fund in place for SMEs.

Regulators and financial institutions need to adopt a different approach toward financing circular initiatives. Traditional evaluation criteria such as financial return, risk, and profitability might not be sufficient. To accelerate circular financing, the evaluation of projects must incorporate the environmental and social impacts they generate. This approach incentivizes circular initiatives, encouraging enterprises to adopt more sustainable practices. Capacity development is crucial for both financial institutions and enterprises to successfully transition to a circular economy.

Financial institutions need training on assessing the long-term value and sustainability of circular projects, which involves understanding new business models and evaluating non-financial metrics. Enterprises, on the other hand, require education on circular economy principles, access to innovative technologies, and guidance on integrating sustainable practices into their operations. Enhanced capacity in these areas will enable financial institutions to make more informed lending decisions and help enterprises adopt practices that align with circular economy goals, ultimately fostering a more sustainable economic landscape.

This article was jointly authored by Senior Business Consultant Priyo Pranto and Business Analyst Naziba Ali, at LightCastle Partners. For further clarifications, contact here: [email protected]

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights