GET IN TOUCH

- Please wait...

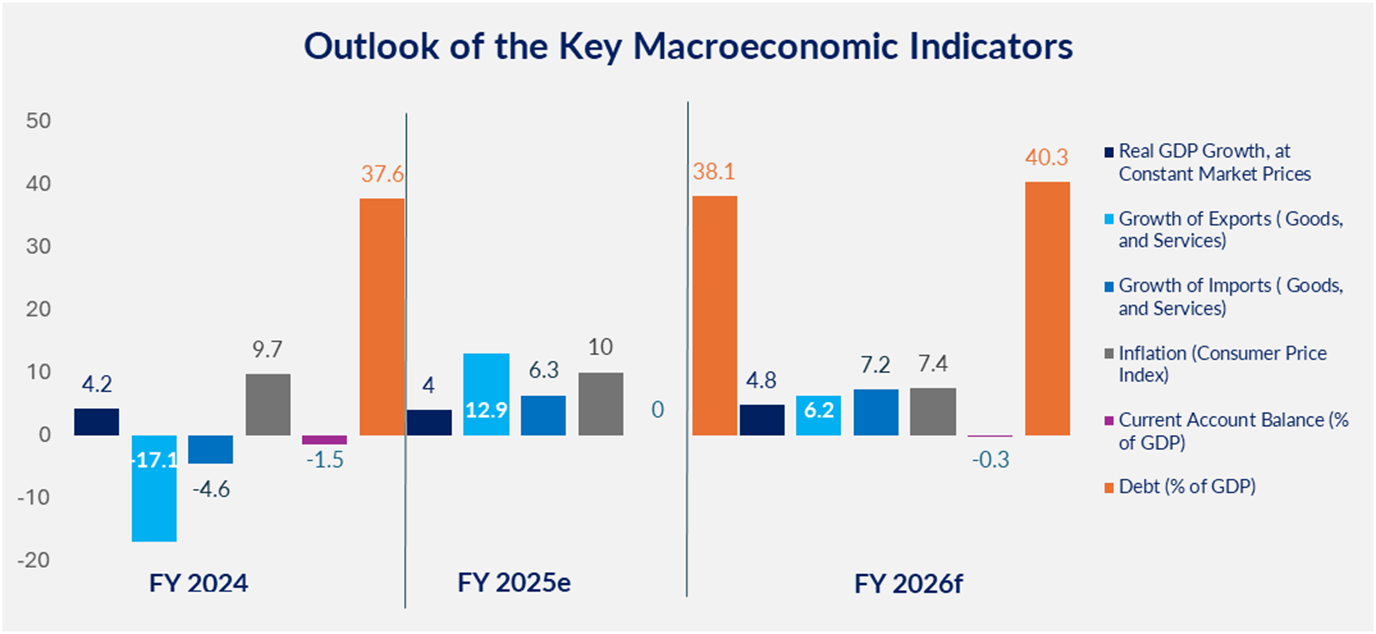

Bangladesh macroeconomic stability and growth outlook shows important signs of resilience amid an ongoing political transition ahead of the 2026 national election. In Fiscal Year 2025 (FY 25), the current account recorded a surplus of USD 149 million, improving sharply from a deficit of USD 6.6 billion in FY24, supported by strong growth in remittances (27.6 percent) and exports (11.0 percent). Foreign exchange reserves have also strengthened, reflecting improved balance of payments conditions, continued engagement from development partners, and steps to strengthen governance within the banking sector, ashighlighted in the World Bank (2025), Macro Poverty Outlook. Yet, investment conditions remain weak. Private investment and the industrial growth index continue to be highly sensitive to external shocks, leading to uneven performance.

This recent economic slowdown is not only a matter of external shocks or cyclical adjustment but also increasingly the outcome of a political transition that has imposed quite a bit of delay on growth. World Bank projections show that real GDP growth fell to 4.0 percent in FY25, marking the third consecutive year of deceleration despite strong export and remittance performance.[1] Indicating that the slowdown is occurring due to lower private investment and restrained public capital spending ahead of the upcoming election in 2026. At the same time, persistent inflation of 8.29 percent in November 2025, compared with wage rate index growth of only 8.04 percent, has continued to erode real incomes and living standards, further hampering domestic demand.[2] In effect, Bangladesh has entered a low-momentum equilibrium where macroeconomic stability is preserved, but growth remains structurally suppressed by uncertainty, deferred reforms, and a political economy that incentivizes caution rather than expansion.

Private investment growth has slowed to 0.8 percent in FY 2025 compared to 3.3 percent in FY 24, reflecting the combined pressure of high interest rates, rising production costs, and prolonged political uncertainty. [3]

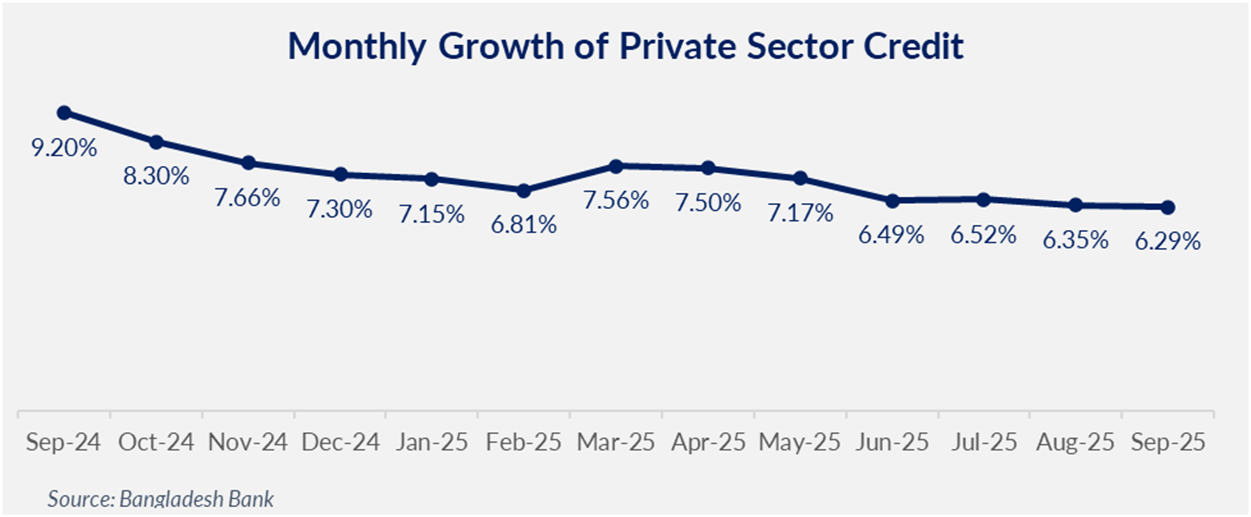

As confidence weakened, private sector credit growth fell to a historic low of 6.29 percent in September 2025, signaling that businesses are postponing borrowing and expansion decisions. The declining trend highlights the high cost of credit and ongoing structural weaknesses in the banking sector, including the merger of underperforming Islamic banks into the newly formed United Islami Bank, as Bangladesh Bank works to strengthen governance and stability.[4] At the same time, political uncertainty and the broader wait for a stable democratic transition in 2026 have reinforced a wait-and-see approach among investors. Together, tighter financial conditions and political caution are weighing on investment decisions, even as reforms in the banking sector gradually take shape.

Public investment has also weakened during this period. In FY25, public investment declined by 25.5 percent, as the government took a cautious approach to approving new projects amid the political transition.[5] This slowdown in public spending has further reduced momentum in infrastructure development projects, delaying economic activity.

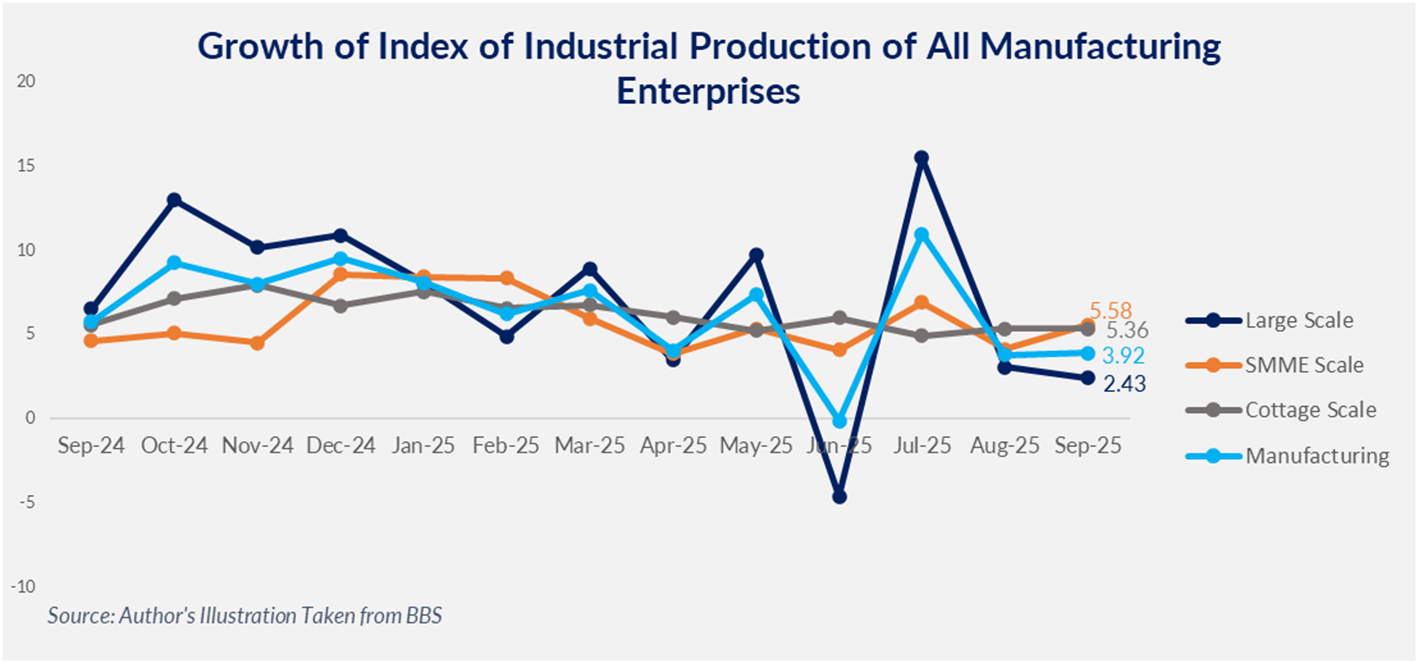

The weakening of investment confidence is also reflected in industrial performance. While large–scale, small, medium, micro, and cottage manufacturing enterprises continued to record positive year-on-year growth in early FY26, the industrial growth index shows a clear declining trend in recent months. This pattern suggests growing hesitation among large manufacturers to commit to long-term production and capacity expansion decisions. Part of this volatility is also linked to renewed global trade policy uncertainty during 2024–25,[6] including concerns around potential tariff escalation under the Trump administration, which has disproportionately affected export-oriented large-scale manufacturing, especially the garments sector. In contrast, SMME and cottage industries have maintained comparatively steadier, albeit slower, growth. While this stability has helped cushion the downturn, it has not been sufficient to reverse the broader slowdown in industrial growth.

Despite weak investment confidence and pressure on domestic demand, Bangladesh’s external inflows continue to provide an important source of stability. Remittance inflow grew by 13.56 percent during July–October FY26 compared to the similar period of FY25, reflecting an increase in foreign exchange reserves as well, around USD 27.58 billion (39.07 per cent year-on-year growth) in October 2025. This sustained growth in remittance inflows has translated directly into a stronger external buffer for the economy.[7]

While external inflows have helped stabilize the macroeconomic position, pressures on the domestic fiscal and investment environment are becoming increasingly visible. Fiscal adjustment in the pre-election period has increasingly relied on domestic borrowing, intensifying pressure on Bangladesh’s banking system. Total net borrowings rose almost sevenfold in July–September, FY26 compared to the same period last year.[8] On top of that, public investment has also slowed sharply. The government has spent just 11.75 percent of the Annual Development Programme (ADP) allocation in the first five months of the current fiscal year which marks one of the weakest early-year implementation performances in at least 15 years. 6[9], signaling project delays, administrative bottlenecks, and pre-election spending restraints. Together, rising domestic borrowing and weak public investment execution have compounded the growth slowdown, suppressing aggregate demand at a time when private investment remains hesitant. At the sector and enterprise levels, the impact is visible through tighter credit, project delays, rising costs, and weaker employment growth.

Global trade tensions and rising tariff barriers are weighing on external demand, particularly as contractions in key EU markets affect export momentum. At the same time, elevated inflation continues to erode real incomes and compress domestic demand. Against this backdrop, Bangladesh’s growth outlook remains closely tied to the political cycle.

Downside risks include prolonged election-related instability, continued stress in the banking sector, and delayed structural reforms. On the other hand, a credible election followed by effective policy prioritization could unlock deferred investment, accelerate public project execution, and restore credit flows. The post-election period will therefore be decisive in determining whether growth remains constrained or reverts to a stronger medium-term trajectory, at a time when Bangladesh’s LDC graduation is approaching amid intensifying global economic pressures and rising competition.

By late 2025, Bangladesh’s economy appears stable but constrained. External balances have improved, and inflation has moderated, but internal growth drivers, such as, investment, credit, and public spending, remain weak. Political uncertainty has preserved macro stability at the cost of momentum, resulting in a low-growth equilibrium rather than a crisis. This cautious equilibrium is also reflected in the IMF’s decision to defer the next USD 800 million tranche until after the election, highlighting the importance of policy continuity to sustain reform momentum.[10]

The upcoming national election represents a clear inflection point. A credible and business-conducive transition, anchored in political stability, improved governance, and a reset of relations with key neighbours, could restore investor confidence, revive FDI inflows, and accelerate infrastructure spending. Failure to restore confidence, however, risks causing prolonged stagnation and delaying Bangladesh’s return to a higher-growth path, even if macro stability is preserved.

Author

This article was co-authored by Shoumik Shahriar, a Project Manager and Senior Business Consultant and Sadia Karim, a Business Consultant, working in the Development & Management Consulting department at LightCastle Partners. For further clarifications, contact us here: [email protected]

[1] World Bank. (2021, August 24). mpo-bgd.pdf.

[2] Bangladesh Bureau of Statistics. (2025). Monthly release on Consumer Price Index (CPI), inflation rate and wage rate index (WRI) in Bangladesh: October 2025. Price & Wage Statistics Section, National Accounting Wing, BBS

[3] World Bank. (2021, August 24). mpo-bgd.pdf.

[4] The Business Standard. (n.d.). BB includes “United Islami Bank” in scheduled banks list.

[5] World Bank. (2025, October). Bangladesh development update: Special focus – Urbanization as a pathway to boost job growth.

[6] UNCTAD. (2025). Global trade update: September 2025 – Trade policy uncertainty looms over global markets.

[7] Kamal, M., & Nazir, M. I. (2025, October). Bangladesh macroeconomic pulse: October 2025. Centre for Policy Dialogue (CPD)

[8]Bangladesh Bank. (2025a). Major economic indicators: Monthly update (October 2025).

[9]The Daily Star. (2024). Govt spends only 11.7% of ADP fund in five months.

[10] Dhaka Tribune. (n.d.). Bangladesh’s $5.5bn IMF loan tranche postponed.

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights