GET IN TOUCH

- Please wait...

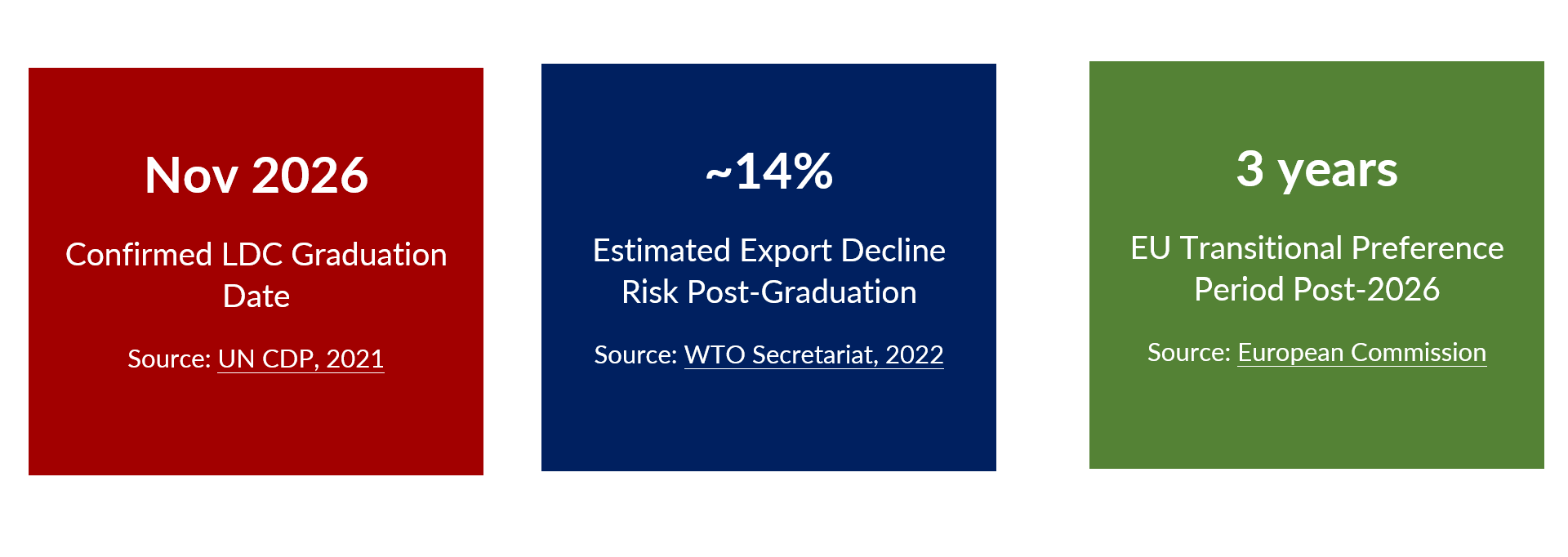

In November 2026, Bangladesh will formally graduate from the United Nations’ Least Developed Country (LDC) category, a milestone that recognizes more than five decades of hard-won economic transformation. For over four decades, LDC status provided Bangladesh with a suite of trade preferences that acted as a structural subsidy to its export-oriented industries, particularly ready-made garments (RMG), which account for roughly 86% of total merchandise exports.1 Preferential market access through mechanisms such as the EU’s Everything But Arms (EBA) scheme, Canada’s Least Developed Country Tariff, and the UK’s Developing Countries Trading Scheme (DCTS) enabled Bangladeshi exporters to undercut competitors on price despite underlying structural inefficiencies in energy, logistics, and regulatory compliance.

Four structural shifts will define Bangladesh’s post-LDC environment. First, the gradual loss of preferential tariff access exposes exporters to higher MFN tariffs in key markets unless alternative arrangements such as GSP+ or FTAs are secured.

Second, stricter compliance and policy constraints will emerge, including the phase-out of export subsidies under WTO rules, which will limit existing incentive mechanisms.

Third, reduced intellectual property flexibility, particularly in the pharmaceutical sector, may increase costs and constrain export strategies.

Finally, the transition will require a shift from preference-driven competitiveness to productivity-driven growth, where sustained export performance will depend on efficiency, technology adoption, and integration into global value chains.

FDI operates through two complementary channels in the post-LDC context. The first is domestic transformation: technology transfer, industrial upgrading, and productivity spillovers that reduce the underlying cost structure of Bangladeshi industry. The second is export competitiveness: foreign firms bring buyer relationships, compliance certifications, and GVC linkages that substitute for some of the market access advantages Bangladesh will lose. Empirical evidence from LDC graduates shows mixed results in order for FDI to drive industrial competitiveness primarily by structural factors. For instance, Cabo Verde’s FDI inflows declined sharply from approximately USD 210 million in 2008 to around USD 89 million in 2013, reflecting the impact of the global financial crisis and its dependence on tourism-led investment.2 In contrast, the Maldives experienced a surge in FDI to nearly USD 1 billion by 2019, driven by tourism expansion.3 Similarly, Botswana’s investment trajectory has historically been anchored in its diamond sector, which further indicates that post-graduation economic trends largely reflect pre-existing structural dynamics rather than being caused by graduation itself.

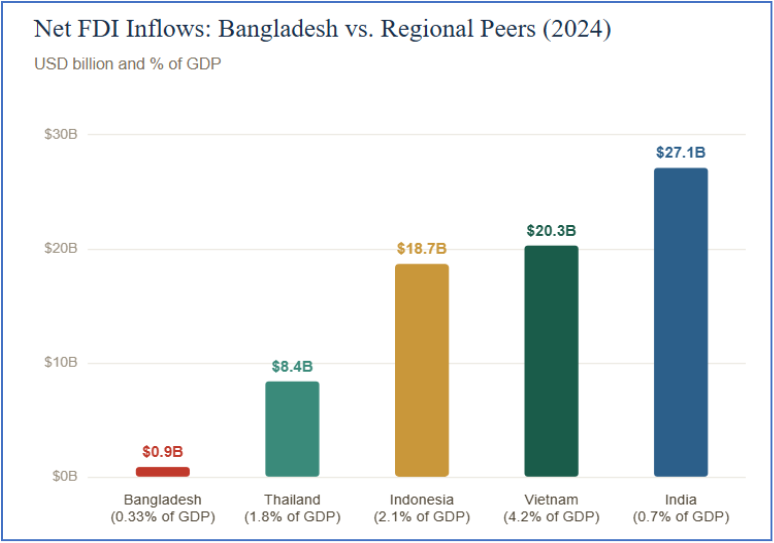

Yet Bangladesh’s current FDI performance is structurally weak. Net FDI fell to a five-year low of USD 1.27 billion in 2024 before recovering 20% to USD 1.71 billion in FY2024–25.4 At just ~0.3% of GDP, Bangladesh’s FDI inflows remain significantly lower than peer economies such as Vietnam (~4.3%), highlighting a persistent investment gap. This underperformance reflects structural constraints, including regulatory inefficiencies, infrastructure limitations, and weaker integration into global trade and investment networks.5

International investors apply a multi-dimensional assessment framework when choosing FDI destinations. Understanding where Bangladesh stands on each dimension is essential to identifying both its competitive advantages and the structural gaps that require policy intervention.

Table: Bangladesh’s Position on Key FDI Determinants

| Determinant | Bangladesh’s Position | Key Metric / Evidence | Assessment |

| Market Size | Large domestic market (~170M population); sustained economic growth | Strong GDP growth trajectory; population scale supports demand | Strong |

| Global Market Access | Limited trade integration; dependence on preferential schemes | Low FDI-to-GDP ratio (~0.3%) compared to peers like Vietnam (~4.3%) | Weak |

| Regulatory Predictability | Moderate progress in business environment reforms, but still evolving | B-READY Index 2024: Ranked 29th out of 50 economies | Below Average |

| Infrastructure & Logistics | Ongoing infrastructure development; logistics inefficiencies persist | Need for improved infrastructure, logistics, and investment climate highlighted | Improving |

| Energy Reliability | Energy demand rising; reliability challenges remain | Energy investment and diversification (including renewables) are needed to support growth | Constrained |

| Labor Availability | Large, cost-competitive workforce; skills upgrading needed | Cost competitiveness and a large labor base are highlighted as key investor advantages | Cost Advantage |

| FDI Stock & Confidence | Low FDI penetration; declining relative attractiveness compared to peers | FDI remains low as % of GDP (~0.3%), indicating underperformance | Weak / Underperforming |

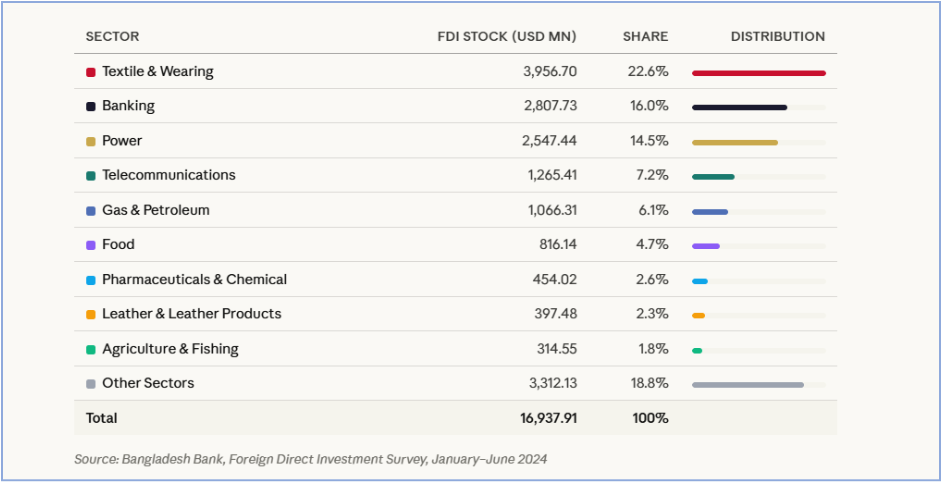

Understanding the sectoral distribution of both FDI stock and recent flows is essential for evaluating where investment is likely to accelerate, stabilize, or retreat in the post-LDC environment.

Textiles and the energy sectors — power, gas, and petroleum — together command over 43% of Bangladesh’s total FDI stock, reflecting an investment base still anchored in labor-intensive manufacturing and resource infrastructure. As Bangladesh navigates its post-LDC transition, broadening this concentration toward higher-value sectors such as pharmaceuticals, ICT, and agro-processing will be critical to building a more resilient and competitive investment landscape.

Bangladesh’s LDC graduation is not the closing of a door; it is the opening of a harder, more honest test of competitiveness. The trade preferences that cushioned decades of industrial growth are fading, but the demographic dividend, the manufacturing base, and the growing domestic market remain. Whether FDI becomes the engine of Bangladesh’s next chapter depends on a single variable: the speed and seriousness of reform. The window is open. The question is not whether Bangladesh can attract the investment it needs; it is whether it will build the country that investors choose.

This article was authored by Faiza Tahiya, Business Analyst at LightCastle Partners

For further clarifications, contact here: [email protected]

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights