GET IN TOUCH

- Please wait...

Energy security is a cornerstone of any nation’s economic and social development. For Bangladesh, natural gas value chain has long been the lifeblood of its energy sector, powering industries, generating electricity, and fueling households. However, the country’s energy landscape is at a critical juncture.

As domestic gas reserves shrink and dependence on Liquefied Natural Gas (LNG) imports grows, Bangladesh faces a worsening energy deficit. With foreign exchange reserves standing at $20.59 billion as of August, concerns are mounting about the country’s ability to sustain LNG imports for the long term.

Even though global spot market prices for LNG have eased recently, continued reliance on imports is neither financially sustainable nor supportive of long-term energy security. This situation calls for a comprehensive reassessment of Bangladesh’s natural gas value chain, with a focus on enhancing infrastructure and improving operational efficiency to close supply gaps and ensure stable energy access in a volatile global market.

This article delves deep into the complexities within Bangladesh’s natural gas value chain, highlighting the crucial interventions needed to secure a sustainable energy future.

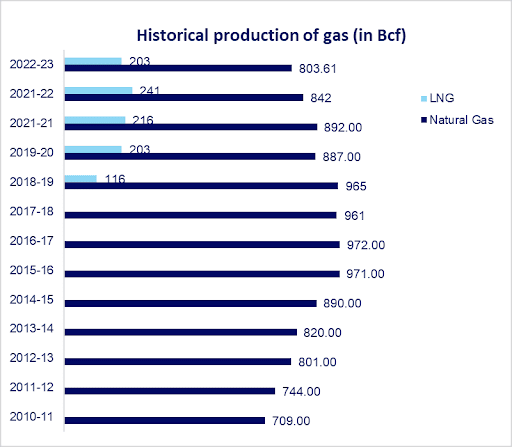

In the 1960s, when Shell Oil discovered five major gas fields in Bangladesh, the country secured its spot on the world gas map. Later, in 1997, Chevron discovered the Bibiyana gas field in Habiganj. Today, Bangladesh has 29 gas fields, with Chevron operating three of them. As of 2023, the Bibiyana, Titas, Jalalabad, and Habiganj gas fields together accounted for 84% of the total daily gas supply.

However, the reserves are dwindling at an alarming pace. For instance, Titas, the largest gas field, initially held reserves of 6.36 trillion cubic feet, but by 2023, only 1.14 trillion cubic feet remained. Likewise, Bibiyana’s reserves, despite its substantial production levels, fell from 5.75 trillion cubic feet to merely 0.33 trillion cubic feet.

To address the growing gap between domestic production and increasing energy demand, the country commenced LNG imports in 2018. Initially seen as a prudent decision due to the affordability of LNG at the time, this strategy began to falter just a year later due to the supply chain disruptions caused by the COVID-19 pandemic. Further complications arose with the global fuel price shocks triggered by Russia’s invasion of Ukraine in 2022.

In light of the current demand of approximately 4,000 mmcfd (million cubic feet per day) of gas in the country, the supply stands at 2,900 mmcfd. Of this supply, domestic production provides 78%, while imports account for the remaining 22%.

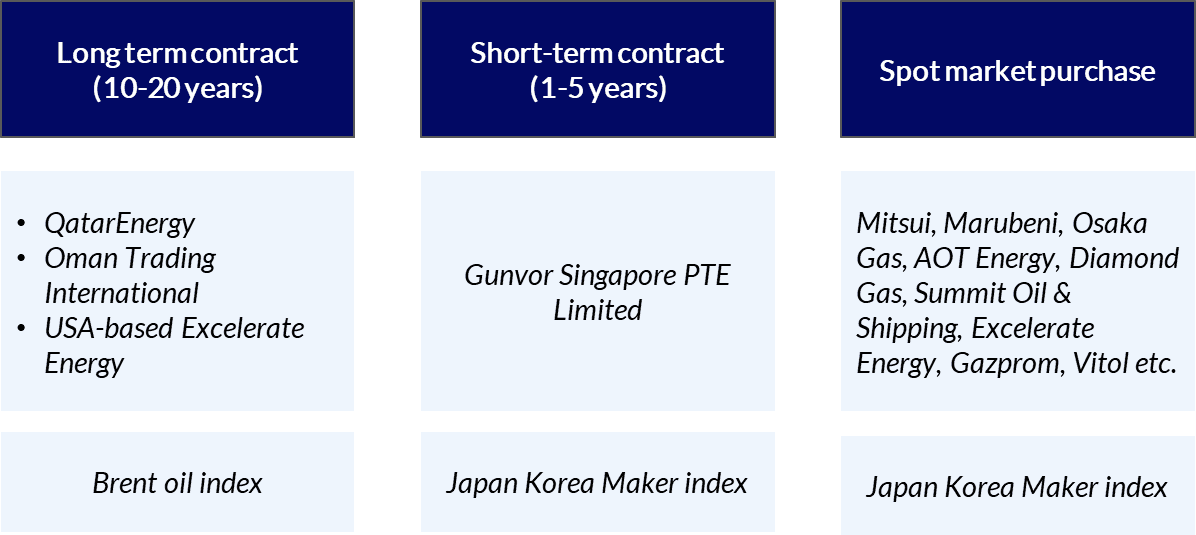

Since 2018, Qatar has been the leading supplier of LNG to Bangladesh, with export volumes ranging from 1.82-2.5 million tonnes per annum (MTPA), while Oman has been providing an additional 1-1.5 MTPA. At present, three Floating Storage and Regasification Units (FSRUs) are in operation at Maheshkhali to regasify the imported LNG. Excelerate Energy, a U.S.-based company, owns two of these terminals, while Summit owns the remaining one. Presently, the two FSRUs operated by Excelerate contribute approximately 25% of the gas supply while the FSRU owned by Summit has a regasification capacity of 500 mmcfd.

In 2023, Qatar, Oman, and Excelerate Energy signed three new 15-year Sales and Purchase Agreements (SPAs). Gas supply under these agreements will begin in 2026. Under the new deals, Qatar will supply an additional about 1.5 MTPA of LNG per year from 2026 to 2040 while Oman will supply 0.25-1.5 MTPA.

Under its 15-year deal with Qatar, Bangladesh will pay 12.65% of the 3-month average price of Brent oil plus a constant of 50 cents per mmBtu (million British thermal units). The Brent oil index, reflects the price of crude oil extracted from the North Sea and serves as a reference price for buyers and sellers of crude oil globally.

For Oman, LNG pricing follows a formula of 11.9% of the three-month average Brent crude oil price plus a fixed charge of 40 cents per million British thermal units (mmBtu). In addition to long-term contracts, buyers acquire LNG through short-term agreements and the spot market.

Over the next two years, until the long-term LNG contracts start in 2026, Bangladesh plans to import a total of 24 LNG cargoes from Gunvor Singapore. The deal will be Bangladesh’s first short-term LNG contract with pricing determined by the JKM (Japan Korea Maker) index.

The index plays a key role in Northeast Asian LNG deals, where prices typically rise in winter due to higher demand for heating. In the summer, demand drops, leading to lower prices. Since Bangladesh needs more LNG during the summer, linking its contract to JKM allows the country to take advantage of these lower prices during its peak demand season.

The deal not only minimizes exposure to the spot market but is also more advantageous than long-term contracts, which are about $1.2/MMBtu above JKM prices. In addition, the interim government will adhere to the Public Procurement Rules 2008 to purchase LNG from the international spot market.

The natural gas value chain in Bangladesh operates through three main segments: upstream, midstream, and downstream.

Similarly, the LNG value chain in Bangladesh encompasses several critical stages, from importation to end-user distribution.

1. Upstream Segment: Bangladesh imports LNG mainly from Qatar and Oman under long-term contracts. Buyers also rely on spot market purchases to manage demand fluctuations.

2. Midstream Segment: The midstream segment includes transportation, storage, regasification, and transmission of LNG.

3. Downstream Segment: The gas is then injected into the national pipeline network managed by Petrobangla and its subsidiary companies like Titas Gas Transmission and Distribution Company Limited.

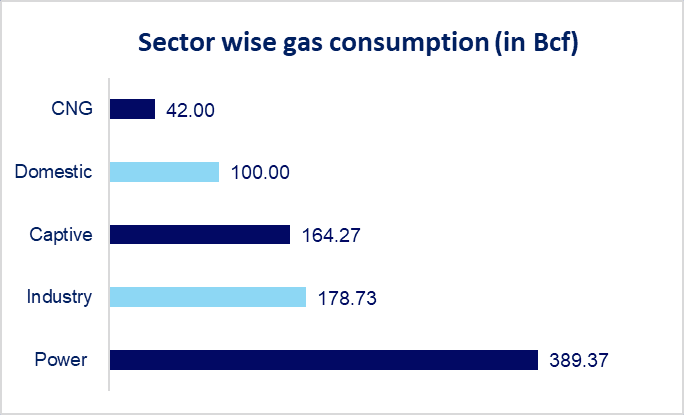

Given the current demand for approximately 4,000 mmcfd of gas in the country, the supply is currently at 2,900 mmcfd. This reflects a shortage of 27.5%. Similarly, while daily LNG demand stands at 800 million cubic feet, suppliers currently provide only 600 million cubic feet. Because of the ongoing scarcity, businesses across different sectors have struggled from time to time. Due to the demand-supply mismatch and resulting power shortages, large RMGs must purchase diesel for generators, incurring daily costs between BDT 50,000 and BDT 70,000.

Over the past 15 years, the capacity for power generation has increased by fivefold, whereas natural gas production has risen by only 3.6 times. This disparity indicates that power generation growth may not align with a proportional increase in natural gas supply, potentially leading to greater reliance on alternative energy sources or worsening existing shortages. As of 2023, the power sector consumed the most natural gas, followed by and captive power generation.

Given the significant gap between demand and supply, operational bottlenecks in the natural gas sector have become increasingly pronounced. These constraints limit the effective utilization of existing resources and hinder the sector’s ability to meet the growing energy needs.

The Government of Bangladesh established the Gas Development Fund in 2012 to support large-scale exploration in both onshore and offshore regions. Despite Bapex’s current logistical and technical capacity to drill three wells annually, the country has only drilled 26 exploratory wells since 2000, averaging just one well per year. Recently, authorities discovered a 2 trillion cubic feet (TcF) reserve in Bhola, while untapped potential remains in the Chittagong Hill Tracts and offshore areas.

The production facilities in local gas fields exhibit various weaknesses, including inefficient production as compared to International Oil Companies (IOCs). For instance, both the state-owned Titas gas field and the Bibiyana field, managed by a foreign operator, each have 26 wells. However, the average production per well at Titas is only 15 million cubic feet of gas, whereas Bibiyana’s wells produce 42 million cubic feet per well. Despite Titas having larger gas reserves, its production is only one-third of that of Bibiyana.

The existing infrastructure coverage is insufficient to adequately serve the country’s critical market areas, as the majority of gas supply points are located in the northeast and central regions, while delivery points are situated in the central, southern, and western regions. By 2025, a 65-kilometer pipeline will connect Satkhira to Khulna, transporting 300 million cubic feet of gas from India. This supply will power ongoing and future plants in Khulna, bringing gas to the western region for the first time.

While gas-fired captive generators have a capacity exceeding 3,000MW, the majority of them have an average efficiency of 35.38%. According to a report by the Institute for Energy Economics and Financial Analysis (IEEFA), this figure could increase to 45.2%. Factories seldom harness the waste heat from generators or the jacket cooling water for productive use. However, implementing these measures could result in significant gas savings, potentially reducing annual LNG import costs by US$460 million.

As natural gas travels through pipelines over long distances, it loses pressure due to friction and changes in elevation. To address the issue, the government built compressor stations, but insufficient gas flow has led to their underutilization. Between FY 2019-20 and 2022-23, Gas Transmission Company Limited (GTCL) paid BDT 3000 Mn to five foreign firms for the operation, maintenance, and servicing of these compressors. This situation is akin to power plants receiving capacity payments without generating electricity.

As we stand today, there is a need for policy-level intervention to assess the benefits of improving energy efficiency to contain increasing LNG demand in the short- to medium-term instead of only enhancing regasification capacity and increasing imports. There is also concern about the inefficient use of gas, for example, in captive power generation, which provides an uninterrupted electricity supply to industries amid the lack of reliable grid electricity. Bangladesh is unlikely to abandon LNG imports in the foreseeable future. However, to curb demand growth, it will need to draw on all available avenues, such as enhancing energy efficiency in captive power generation.

As estimated by Petrobangla, the nation’s LNG imports will more than double, increasing from the current 3.5 million metric tons per year to 7.5 million metric tons per year, starting in early 2026, following the new contracts. The move to a stricter tendering system under the PPR-2008 rules could influence the future strategies of market players. By ensuring a more predictable and transparent environment, the government hopes to attract new suppliers and stabilize import costs. State-owned gas fields require prioritized technical management, including necessary repairs, adjustments, and additional equipment.

Bangladesh has the potential to save nearly half a billion dollars a year by reining in its import dependence on LNG. The solutions do not lie offshore but closer to home, such as in replacing the nation’s vast stock of aging, inefficient captive gas-fired power generators.

While the government should continue its efforts to boost local natural gas production, it appears that, for the time being, there is no halting LNG imports to address the ongoing crisis. However, considering the concurrent foreign reserve challenges, this could present significant difficulties. The original LNG import plan did not account for extreme volatility in the international fuel market, local currency depreciation, and weak fiscal conditions.

To enhance the throughput capabilities and facilitate transmission of additional gas, the gas transmission network must be expanded to accommodate the upcoming diversified gas supply sources from imports and offshore discoveries into the national gas network.

Therefore, the government should prioritize reducing non-essential expenditures that are depleting the country’s reserves and concentrate on securing favorable agreements with other nations to enhance LNG imports. The success of Bangladesh’s exploration endeavors will depend on various factors, including technological implementation, regulatory capability, trade negotiation expertise, professionalism, transparency, and geopolitical influence.

Naziba Ali, a Business Analyst, at LightCastle Partners has prepared the write-up. For further clarification, please contact: [email protected]

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights