GET IN TOUCH

- Please wait...

“When the last tree is cut, the last fish eaten, and the last stream poisoned, you will realize you can’t eat money.” The old Cree Indian warning feels more relevant than ever, especially in a world that keeps chasing quarterly gains while ignoring the long-term costs of climate and social neglect. For Bangladesh, the message hits close to home. Rising sea levels, floods, and resource stress are no longer distant risks; they are economic realities that shape investment, production, and livelihoods. Across industries and financial institutions, a new question is emerging: Can growth be sustained if it destroys the very foundations that support it?

This is where ESG investing steps in. It reframes the idea of return, linking financial performance with environmental stewardship, social equity, and governance integrity. The real test for Bangladesh now is whether it can show that future cash flows can grow without exhausting the future itself.

ESG investing refers to an investment approach that integrates environmental, social, and governance factors into financial analysis and decision-making, alongside traditional measures of risk and return. It shifts financial decision-making from a purely cost-benefit analysis model to one that integrates various non-financial factors that has short- and long-term impact on business and community.

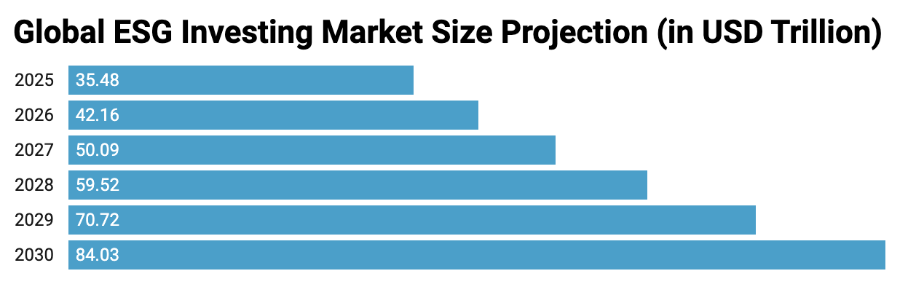

The concept originated in a 2004 UN Global Compact report, Who Cares Wins, which argued that better environmental and social management leads to stronger financial performance.i Since then, ESG has evolved from a voluntary ethical preference to a mainstream investment mandate, now projected to grow to USD 40 trillion by 2030.ii

What began as a niche movement led by ethical investors has now transformed into a defining force in global finance. As of December 2024, the global ESG investing market size has already reached USD 29.86 trillion.iii In Europe, a total of EUR 169 billion of ESG bonds, sustainability-linked, and green bonds were issued in Q1 2025.iv In Sept 2025, US ESG mutual funds and Exchange Traded Funds held assets worth approximately USD 617.44 billion.v

While the US & European markets are showcasing consistent progress, Asia is emerging as the next growth engine. Over the past decade, the region accounted for 29 percent of global corporate sustainable bond issuance, emphasising its growing role in ESG capital flows. Asia-domiciled funds, focused on ESG, or sustainability, contain roughly USD 83 billion in Assets Under Management (AUM).vii Globally, the cumulative volume of ESG-themed bonds like green, social, sustainability, and sustainability-linked has now surpassed USD 6 trillionviii

96 percent of the world’s 250 largest companies (the G250) now report on sustainability or ESG matters.ix

Over the past decade, a diverse set of tools has emerged to channel funds toward responsible and resilient growth. In this growth journey, the key instruments driving the ESG investment landscape are:

These are some of the most prominent ESG investing instruments but the universe of ESG investments is not limited to these instruments only.

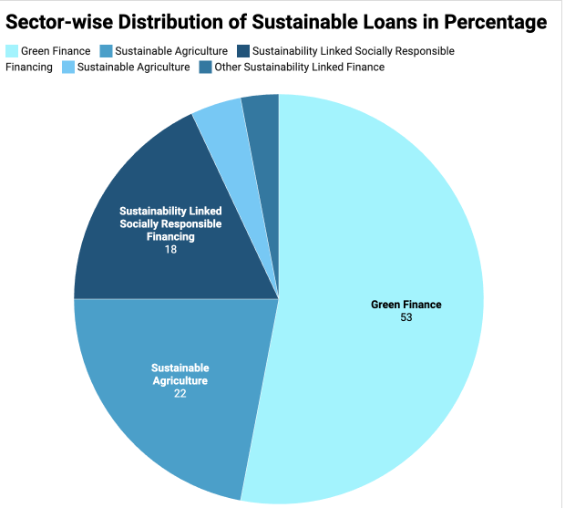

Even though the Bangladesh ESG ecosystem is at a nascent stage, it has started taking steps in the right direction. What began as a central bank mandate has evolved into meaningful capital flows toward greener and more inclusive growth. In Q1 2025, banks and financial institutions disbursed BDT 1,49,819 crore in sustainable finance, which is up BDT 1,703 crore from the previous quarter.x Ready-made garments, renewable energy, and sustainable agriculture are among the leading sectors in getting ESG financing. In 2021, sustainable lending accounted for 8 percent of total credit; in 2025, it represents 40 percent.xi

Seven Bangladeshi firms now appear on Bloomberg’s global sustainability index.xii Bangladesh Bank now requires banks and NBFIs to report on sustainability performance, aligning domestic regulation with international norms such as IFRS S1/S2 and GRI Standards.

Innovation is emerging in corporate debt instruments along with scale. Standard Chartered Bangladesh’s corporate green bond for PRAN Limited marked the country’s first green bond (with a face value of BDT 1.5 Billonxiv). In 2025, BRAC Bank secured approval from the Bangladesh Securities and Exchange Commission and Bangladesh Bank to issue the country’s first-ever Social Subordinated Bond, which is valued at BDT 1,000.xv Together, these instruments signal that Bangladesh is beginning to embed sustainability into its allocation of capital.

Along with the supply side, a major driver of Bangladesh’s ESG finance momentum is now emerging from the demand side, led by the country’s export-oriented RMG sector. With the European Union’s Green Deal and the Corporate Sustainability Reporting Directive (CSRD), global buyers are raising the bar on environmental and social performance across their supply chains. To retain access to key markets, RMG factories are under pressure to invest in energy-efficient technologies, rooftop solar, wastewater treatment, and cleaner production systems. This shift is accelerating the need for green loans, transition finance, and blended finance to fund compliance and competitiveness. This is a strong reminder that ESG finance is no longer just a policy mandate; it is becoming a commercial necessity driven by international market access and supply chain resilience.

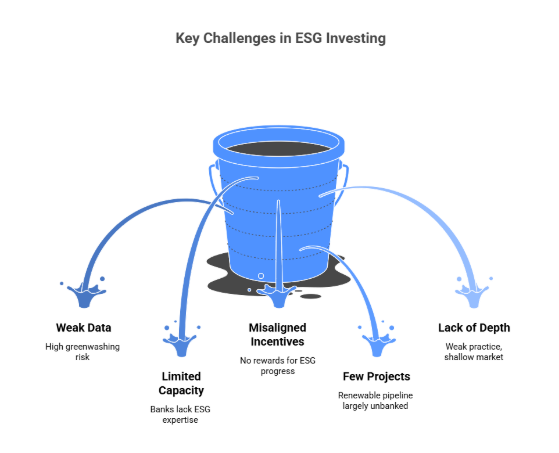

While Bangladesh’s ESG finance momentum is growing, the foundation remains fragile. Beneath the progress lie structural barriers in data, capacity, incentives, and governance that could slow the transition from policy ambition to market reality.

1. Weak Data and Verification Systems: Every credible ESG system starts with reliable data, and that remains Bangladesh’s weakest link. Most financial institutions depend on self-reported borrower data, often without independent validation. SMEs, which account for 87 percent of the active labour force,xvi rarely maintain ESG records or disclosure frameworks. As a result, banks struggle to assess ESG performance, compare risks across borrowers, or verify the real impact of their “green” portfolios, leaving the system vulnerable to inconsistency and greenwashing.

2. Limited Capacity and Technical Expertise: Policy has outpaced practice in Bangladesh. While Bangladesh Bank has Sustainable Finance Policy and Guidelines on Environmental & Social Risk Management (ESRM), implementation depends on people who often lack the training to operationalize them. Without proper training in climate risk modelling, carbon accounting, and ESG-linked financial analysis, institutional capacity will remain a bottleneck.

3. Misaligned Incentives: Sustainable financing has yet to be a profitability strategy for most banks, rather it is a quota to fulfil. Interest rates rarely reward ESG improvements, meaning borrowers who invest in green upgrades face the same financing costs as those who don’t. In contrast, sustainability-linked loans (SLLs) globally reduce margins when companies meet ESG targets, creating tangible motivation. Until capital costs reflect sustainability performance, ESG lending will struggle to compete with higher-yield sectors like trade or consumer finance.

4. Limited Pipeline of Bankable Projects: The gap between ESG ambition and investment readiness remains wide. Many adaptation projects fall outside conventional lending models and are often viewed as too small or too risky for banks. As a result, ESG financing in Bangladesh is still largely driven by government entities and development finance institutions, while private investment plays only a limited role.

5. Lack of Market Depth: The bond market, representing 11.63 percent of GDP, limits access to long-term green capital.xvii This bond market is largely government treasury bond driven, which represents 11.44 percent of this 11.63 percent, and only 0.19 percent comes from corporate bonds. In India, the bond-to-GDP ratio is 70 percent.xviii Only a few ESG debt instruments, ike Standard Chartered Bank‘s Green Bond have emerged in our ESG ecosystem, while Green Sukuk and ESG ETFs remain untapped. Without stronger regulatory enforcement, assurance mechanisms, and deeper capital markets, ESG integration risks losing momentum.

The next phase for Bangladesh’s ESG investment ecosystem requires credible data infrastructure, skilled professionals, aligned incentive mechanisms, and stronger market infrastructure. Success will depend on whether Bangladesh can transform ESG finance from a compliance exercise into a competitive advantage.

Bangladesh has made some progress so far as one of the first developing nations to issue green banking guidelines to now disbursing significant credit through sustainable finance channels. But progress built on policy needs the next ingredient: execution that scales.

The good news is Bangladesh doesn’t have to start from scratch. Peers like Malaysia, Kenya, and Indonesia have already tested models that bridge data gaps, attract investors, and build trust in ESG systems.

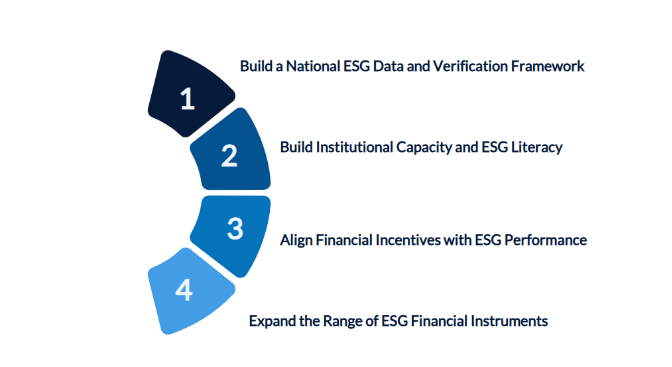

1. Build a National ESG Data and Verification Framework: Bangladesh’s ESG ecosystem currently lacks a standardized, verifiable data infrastructure. The dependency of most banks and corporates on self-reported ESG information, with limited third-party assurance, weakens comparability and increases the risk of greenwashing.

To strengthen credibility, a National ESG Data Repository should be established under Bangladesh Bank and the Financial Reporting Council (FRC). This platform would store sector-level indicators, emission benchmarks, and climate exposure data. Third-party assurance should be made mandatory for ESG reports, while domestic ESG rating agencies should be accredited to enhance transparency.

Lessons from Malaysia: Malaysia’s Climate Change and Principle-Based Taxonomy (CCPT) require financial institutions to classify assets by environmental impact and disclose portfolio xix Within a short time since the launch in 2019, it has significantly improved data quality and investor confidence in ESG disclosure.

2. Build Institutional Capacity and ESG Literacy: Policy progress in Bangladesh has outpaced institutional capacity. Many banks and corporates still lack trained ESG specialists capable of assessing climate risk, social impact, or governance performance.

To close this gap, Bangladesh should launch a National ESG Training Program for bankers, regulators, auditors, and listed companies. Partnerships with IFC, ADB, and UNDP can provide modules on climate risk analysis, ESG integration in lending, and disclosure best practices. ESG Centres of Excellence in leading universities can further develop local expertise and certification pathways.

Lessons from Kenya: The Kenya Bankers Association’s Sustainable Finance Initiative (SFI) has trained over 50,000 professionals from banks and microfinance institutions, helping integrate sustainability principles into credit and risk management decisions.xx The Central Bank of Kenya also launched the Green Finance Taxonomy and Climate Risk Disclosure Framework in 2025 to guide financial institutions in classifying green activities and aligning with global standards.xxi

3. Align Financial Incentives with ESG Performance: ESG finance in Bangladesh is often seen as a compliance requirement rather than a business opportunity. Loan pricing, refinancing, and tax structures rarely reward firms for strong ESG performance.

To change this, Bangladesh Bank can introduce ESG-linked loan pricing that offers lower interest rates for verified sustainability achievements. ESG metrics can also be integrated into public procurement and PPP evaluations, while high-performing borrowers may access tax rebates or refinancing incentives for meeting ESG targets.

Lessons from Chile: Chile’s Sovereign Sustainability-Linked Bond (USD 2 billion, 2022) directly ties the government’s borrowing cost to national emissions and renewable energy targets,xxii a model where sustainability excellence reduces financing cost.

4. Expand the Range of ESG Financial Instruments: Bangladesh’s capital markets remain narrow, limiting opportunities for ESG-oriented investors. The bond market accounts for just 12 per cent of GDP,xxiii and few ESG-linked debt products exist.

To diversify instruments, Bangladesh should develop a Sovereign Green and Sustainability Bond Framework, endorsed by Bangladesh Bank and the Ministry of Finance, to standardize ESG-linked issuances. The country’s Islamic finance base can be leveraged to popularise and scale Green Sukuk and Transition Bonds for renewable energy, waste management, and green industry upgrades.

Lessons from Indonesia: Indonesia’s Sovereign Green Sukuk, first issued in 2018, has raised over USD 9.6 billion for climate-aligned projects, demonstrating how Islamic finance can drive sustainability at scale while appealing to global investors.xxiv

ESG finance is no longer a moral choice; it is an economic necessity. In a world reshaped by climate shocks, shifting trade regimes, and sustainability-driven capital markets, Bangladesh’s prosperity now depends on how effectively it can integrate purpose into profit. With its young workforce, and growing investor interest, Bangladesh has the potential to lead South Asia’s ESG transformation. If regulators, private investors, and development partners act together, Bangladesh can evolve into a regional ESG finance hub, one that channels capital toward financial growth without compromising the future.

This article was authored by Shoumik Shahriar, Senior Business Consultant & Project Manager at LightCastle Partners. For further clarifications, contact here: [email protected].

Ii. Gaining a broader perspective – a guide to ESG investment approaches

Iii. ESG Investing Market Size and Forecast 2025 to 2034

Iv. Q1 2025 ESG Finance Report

v. Release: ESG Investing, August 2025

vi. ESG Investing Market (2024 – 2030)

vii. Asia Capital Markets Report 2025

viii. Labeled Sustainable Bonds – The World Bank

ix. The move to mandatory reporting – KPMG

x. Why future lies in sustainable finance

xi. Why future lies in sustainable finance

xii. 7 Bangladeshi firms on Bloomberg’s sustainability list

xiii. Banking on Sustainability: How Bangladesh is building a greener future

xiv. Issuing Bangladesh’s first corporate green bond

xv. BRAC Bank gets approval to issue country’s first social bond

xvi. Bangladesh: Unlocking the potential of cottage, micro, small and medium enterprises

xvii. Bond market largely remains untapped

xviii. Indian Bond Market 2025: Trends, Size & Corporate Bond Issuance Growth

xix. Climate Change and Principle-based Taxonomy

xx. Sustainable Finance Initiative Drives Best Practice in Kenya

xxi. Issuance of the Kenyan Green Finance Taxonomy and Climate Risk Disclosure Framework

xxii. World’s 1st sovereign sustainability linked bond issued by Chile

xxiii. Bond market largely remains untapped

xxiv. How Indonesia Is Using Its Green Sukuk

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights