GET IN TOUCH

- Please wait...

Globally, electric vehicles have gained momentum as major economies aim for carbon neutrality by 2060. Despite economic and technical challenges, the global drive towards a green transition helped EV sales surpass 17 million in 2024, capturing 20% of the market share.1

The concept of electric vehicles (EVs) dates back to the late 19th century in the US and Europe, with inventors like Robert Anderson experimenting with electric motors. In recent times, EV adoption accelerated after Tesla introduced the Roadster in 2008, offering over 200 miles per charge with lithium-ion batteries.2,3 Looking at the global west, EV sales in the United States reached about 10%, while United Kingdom reached a sales share of nearly 20%.

In Latin America, Brazil doubled its EV sales in 2024, achieving a six percent market share followed by Costa Rica, Uruguay and Colombia reaching a sales share of 15%, 13% and 7.5%, respectively. Africa also saw a doubling of sales, primarily in Egypt and Morocco, although EVs still represent less than one percent of total car sales across the continent.4

Meanwhile, China now dominates the EV market, selling over 11 million electric cars in 2024 alone, nearly half of all global sales. Emerging markets are also catching up to this electric fever. In Asia and Latin America, EV sales jumped more than 60% in 2024 to nearly 600,000 units, matching Europe’s market size from five years earlier.5

Southeast Asia saw a 50 % growth, with notable adoption in Thailand and Vietnam6. Nepal’s market is remarkable, with 76 % of new car sales electric, aided by subsidies, hydroelectric power, and proximity to a neighboring manufacturing hub.7

The Bangladesh EV market is small, unevenly distributed, and dominated by informal three-wheeler fleets. Estimates suggest 25,000–30,000 EVs are on the roads, yet official BRTA registration records show just over 400 as of April 2024.8 In the four wheelers (4W) market BYD is leading, which has sold around 300 units at an average of 50 per month.

Mercedes-Benz averages 12 units per month, BMW offers a single fully electric model through Executive Motors with unspecified sales, and nearly 20 Teslas have been imported, with 12 reported sold.9 In the low-cost segment, more than 5.5 million unregulated three-wheelers dominate, creating one of the largest informal EV ecosystems in the region.10 This highlights a market that is growing but remains largely unauthorized and dependent on policy support for formalization.11

The status across different vehicle segments can be further assessed to better understand the EV market and adoption in Bangladesh:

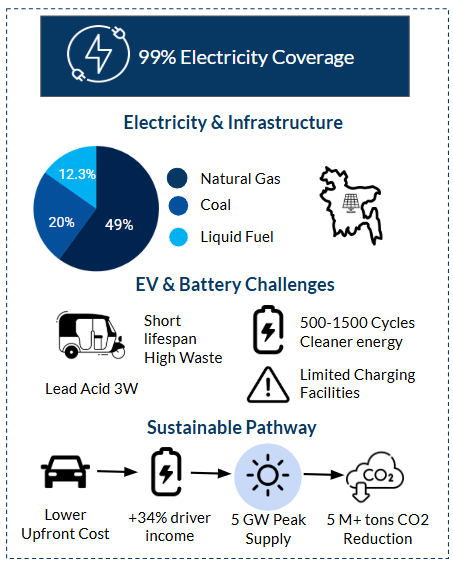

Bangladesh’s electricity sector has ensured maximum coverage with 99%16 of the population now having access to power. In terms of the energy mix, natural gas accounted for nearly 40% of electricity generation in 2025.17 In FY 2023-24, total electricity production reached 95,996 MkWh, up from 88,450 MkWh in FY 2022-23.

Peak generation hit 16,477 MW on April 30, 2024, rising from 10,958 MW in FY 2017-18, while total installed capacity, including off-grid sources, reached 31,452 MW, of which 28,098 MW is grid-based and partly supplemented by imports from India. Generation is divided among the public (36.8%), private (34.6%), joint venture (11.1%), and imports (17.4%). Natural gas (48.5%), coal (19.9%), and liquid fuel (12.3%) dominate the energy mix. Contributions from hydro and renewables remain minimal at 0.86% and 0.98% respectively, highlighting reliance on fossil fuels with limited low-carbon integration.18

The main challenge is not generation but distribution networks, which often causes load shedding. Strengthening infrastructure will be essential to support EV adoption over the next five years. The Roop-pur Nuclear Power Plant may provide a temporary surplus, helping meet early EV demand.19 With the transport sector consuming 54% of total oil products and contributing 14.1% of emissions, the urgency for electrification becomes even clearer.20

While expanding renewable energy will be crucial to support EV charging in the long term, reliance on the national grid is unavoidable in the short to medium term due to high real estate costs that make solar-based charging economically challenging.21

Bangladesh’s EV landscape contrasts sharply with global trends. While global battery demand is expected to surge from 700 GWh in 2022 to 4.7 TWh by 2030, driven by lithium-ion technology22, the country remains dominated by nearly 5 million unregulated lead-acid three-wheelers. These batteries have short lifespans of 150 to 250 cycles and generate roughly 3,000 tons of hazardous waste daily, two-thirds of which are processed in unsafe informal furnaces.

Despite policies mandating a shift to lithium-ion batteries and incentives for local manufacturing, component import, and battery-swapping models, The country lacks lithium-ion recycling, imposes high import duties on four-wheel EVs, and has officially approved only 14 EV charging stations, mostly in major cities.23 Upcoming domestic lithium-ion production, including a planned 1 GWh plant24, offers an opportunity to meet demand, reduce import dependence, and build an export-oriented industry.

Leasing or swapping lithium-ion batteries provides the most practical path for EV adoption. This approach removes high upfront costs, lowers operating expenses, and can increase daily income for drivers by up to 34%.25 Lithium-ion batteries deliver 500 to 1,500 charge cycles over three to five years, far outperforming lead-acid alternatives.26

They can also integrate with the grid through Virtual Power Plant (VPP) systems, tapping into unused energy from up to five million EVs to supply roughly five gigawatts during peak demand. Combined with solar-powered charging stations, this model reduces carbon emissions by over five million metric tons of CO₂ while creating a resilient, efficient, and environmentally responsible EV ecosystem.27 Leasing and swapping lithium-ion batteries therefore provide the most practical and sustainable pathway for Bangladesh’s EV transition.

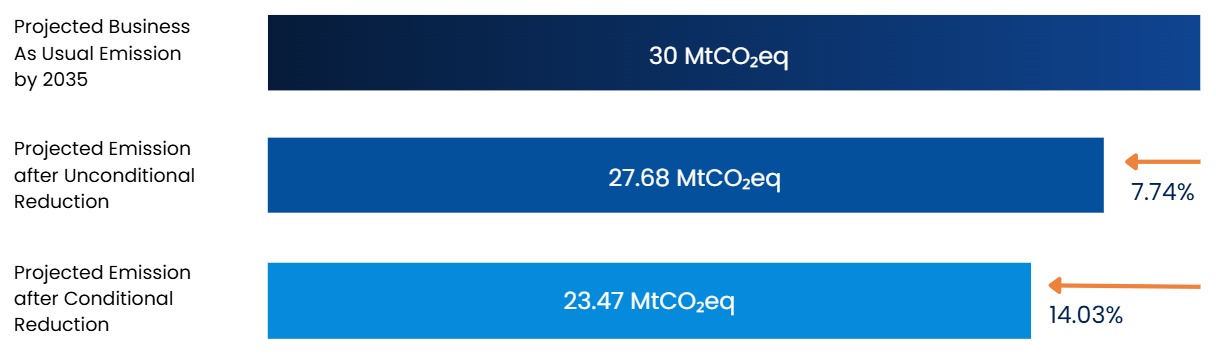

Bangladesh’s transport sector, contributing 18.74 MtCO₂eq in 2022, is projected to reach 30 MtCO₂eq by 2035 under a business-as-usual scenario, making the shift to electric mobility both an environmental necessity and an industrial opportunity. To curb this growth, the NDC 3.0 targets a 21.77% reduction (6.53 MtCO₂eq), 7.74% unconditional and 14.03% conditional.

Mitigation strategies focus on modal shifts to mass rapid transit and bus rapid transit, electrification of 30% of passenger cars and 25% of buses in Dhaka, rail electrification of 348 km, and deployment of solar-powered railway infrastructure. Additionally, complementary policies include national e-mobility roadmaps, EV standards, fiscal incentives, and expanded charging networks, alongside promoting low-emission inland waterways and active transport integration. Together, these measures aim to decarbonize transport sector, promote sustainable mobility, and align Bangladesh’s climate commitments with industrial and urban development goals.28

Previously, the 2021 Automobile Industry Development Policy targeted emission reductions across passenger and commercial vehicles. It promoted local EV production and localization through incentives such as dedicated production funds, 10-year tax holidays, purchase incentives, and road tax waivers. The policy also specified national automobile standards, skill development centers, and multi-agency coordination bodies to ensure a coherent and sustainable EV ecosystem.

Regulatory measures, including revisions to the Motor Vehicle Act, the creation of a dedicated EV cell within BRTA, and steps toward aligning with international safety standards, were introduced to strengthen oversight of vehicle quality and safety. Taken together, these provisions set the foundation for a lower-emission and more sustainable automotive development pathway.29

By 2030, Bangladesh targets 15 to 30 % EV penetration of the national vehicle stock, 30 % electrification of government and semi-government fleets, and 80 % of public transit in Dhaka to be electric, alongside 10 % of private cars.30

These ambitious targets are set with the intent to cut emissions, expand infrastructure, stimulate demand, and establish EVs as a central element of the country’s climate and industrial strategy. An urgent shift is required by accelerating EV adoption that offers reduced fuel imports, lower emissions, and new jobs across assembly, component manufacturing, charging services, and after-sales maintenance.

The Draft Electric Vehicle Industry Development Policy 2025 emerges as a timely step, aiming to provide a roadmap to achieve these goals by boosting domestic production and establishing a national charging network.

It introduces incentives such as concessional bank financing, lower customs duties, tax exemptions, and reduced registration fees, alongside stricter safety and battery recycling standards and formal registration of all EVs by 2030. The policy also aims to encourage local manufacturing, reduce reliance on imported fossil fuels, and support export competitiveness through EV components and backward linkages.31

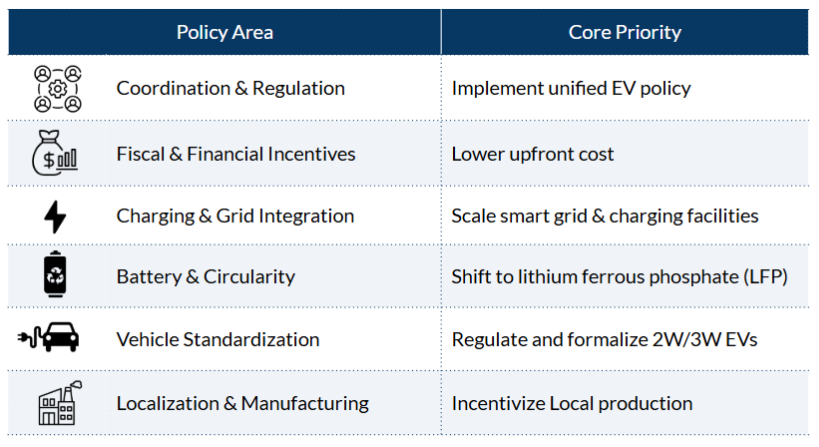

I. Institutional Coordination and Regulatory Framework

The EV transition in Bangladesh is slow-paced due to fragmented regulation across multiple ministries and agencies. A more efficient way to expedite the transition is through a collaborative approach by establishing a multi-agency task force including BRTA, SREDA, NBR, MPEMR, the Ministry of Industries, BERC, BSTI, BIDA, BEZA, and local governments.

This would allow them to remain on the same page, supported by a single, comprehensive, and coherent EV policy that provides clear implementation guidance to align efforts and ensure cross-sectoral integration among transportation, energy, and finance so that the transition does not happen in silos. Strengthened collaboration, coupled with national EV standards and certifications for vehicle approval, testing, and grid interface, can bolster investor confidence and enforce compliance.

II. Financial and Fiscal Incentives

High upfront costs remain the primary barrier for EV adoption. Current registration calculations for four-wheelers (1 kW = 20 cc) inflate fees up to four times, discouraging buyers33. Reformation is required to change the conversion ratio, and a significant reduction in registration fees should be prioritized until 2030 to ensure affordability.

Complementary fiscal incentives, including 5% tax and duty relaxations, exemptions on lithium accessories, and targeted green funds focused solely on EVs, can stimulate demand. Additional incentives like waiving environmental surcharges for ICE-to-EV conversions and enabling battery leasing or swapping models to reduce upfront CAPEX, particularly for micro-mobility, can expedite market uptake. Furthermore, mandating bank financing for EVs, with mechanism to mitigation for foreign exchange risk, can boost private sector investment support.

III. Infrastructure Development and Grid Integration

To address range anxiety caused by limited charging infrastructure and weak grid readiness, the policy must mandate the deployment of charging networks with realistic technical standards, avoiding impractical requirements such as 90 kW minimum commercial chargers in urban areas. The current charging utilization is very low, at 0–5%; hence, a data-driven rollout is imperative, with GIS-based identification of viable sites in Dhaka and along national highways.

Parallelly, coordinated deployment of EVs in high-impact corridors and high-demand areas, including the planned 400 electric buses, should be prioritized.34 To ensure predictable access to charging infrastructure, allocation across home, workplace, and public charging networks should be included in the implementation plan. Infrastructure typologies, on the other hand, should align with usage patterns; for example, fast DC chargers (60–360 kW) on highways and depots to support long-distance and commercial vehicles, mid-range AC chargers (7–22 kW) across residential and urban hubs, and low-level charging and battery-swapping solutions for two- and three-wheelers that make up the majority of daily trips.

Grid readiness policies should adjust to ensure smart grids, AI-driven load forecasting, separate EV metering, Time-of-Use (ToU) tariffs to shift demand to off-peak hours to leverage the estimated 9,000–12,000 MW of unused generation capacity35, and reduced VAT/demand charges to optimize consumption. Side by side, a national standard for payment systems, data and safety protocols, and battery management should be established to ensure interoperability and minimize safety risks.

Finally, to ensure a sustainable business model, key considerations should be placed on lowering commercial charging costs, provision of early-stage subsidies, green finance mechanisms, and incentivizing solar-plus-storage systems for operators to shorten payback periods, which are currently 8–12 years.

IV. Battery Technology and Circularity

The transition from lead-acid (LA) batteries to lithium ferrous phosphate (LFP) batteries is the way forward to mitigate environmental risks and ensure efficiency, as LFP batteries offer 1,200–1,500 cycles compared to 200–250 cycles for LA. To ensure rapid uptake, a strict and time-bound policy is the call of the hour.

To address challenges such as the high upfront cost of LFP batteries, a service-based model should be integrated, for example, the Battery-as-a-Service (BaaS) leasing model, allowing drivers to pay small daily or weekly fees, leading to eventual ownership. Complementary policies should further enforce battery standardization, quality control, and traceability through a centralized platform tracking the lifecycle from manufacturer to end-user and maintenance personnel.

A circular model can be implemented by institutionalizing end-of-life management through centralized recycling and second-life applications, preventing toxic waste disposal currently associated with lead-acid batteries.

V. Formalization and Standardization of Vehicle Segments

At present, Bangladesh’s EV ecosystem is dominated by the electric three-wheeler (3W) segments, which is unregulated and unauthorized. Thess segment’s high popularity, affordability, and short life cycle makes it impractical to disband; rather, a dedicated effort toward formalization is essential36. To achieve this, a dedicated policy must ensure structural standardization, battery transition, grid integration, defined operational areas, safety standards, and registration procedures. Further, by ensuring BRTA oversight, the central policy will help resolve the historical legal ambiguity. Formalization also enables access to bank financing and strengthens social legitimacy.

Additionally, this segment bears an environmental cost due to the high usage of lead-acid batteries; hence, a battery transition mandate should be implemented within a stipulated timeline to shift from lead-acid to lithium-ion batteries. This would further enable circularity through battery traceability and recycling frameworks. Additionally, policy must focus on regulating two wheelers (2Ws) to address the issue of most 2W EVs being imported as electronic parts (using different HS codes) and locally manufactured (CKD), effectively bypassing the official vehicle import duty structure and creating unfair competition for registered brands.

VI. Localization and Manufacturing Development

Developing a globally competitive EV industry demands localized production and robust backward linkages. Policy must prioritize localization and formalization of manufacturing for high-volume segments like three and two wheelers. Incentive mechanisms should discourage fully built imports with higher tariffs on them, encourage local production by prioritizing domestic battery and vehicle assembly, complemented by green financing.

Simultaneously, capacity building of local resources by collaborating with original equipment manufacturers (OEMs) is necessary for knowledge transfer and sustainability of the sector. Finally, strict adherence to global safety and environmental standards is required for both domestic reliability and export-readiness.

This article was authored by Ismat Ara Shimi, Business Analyst at LightCastle Partners. For further clarifications, contact here: [email protected].

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights