GET IN TOUCH

- Please wait...

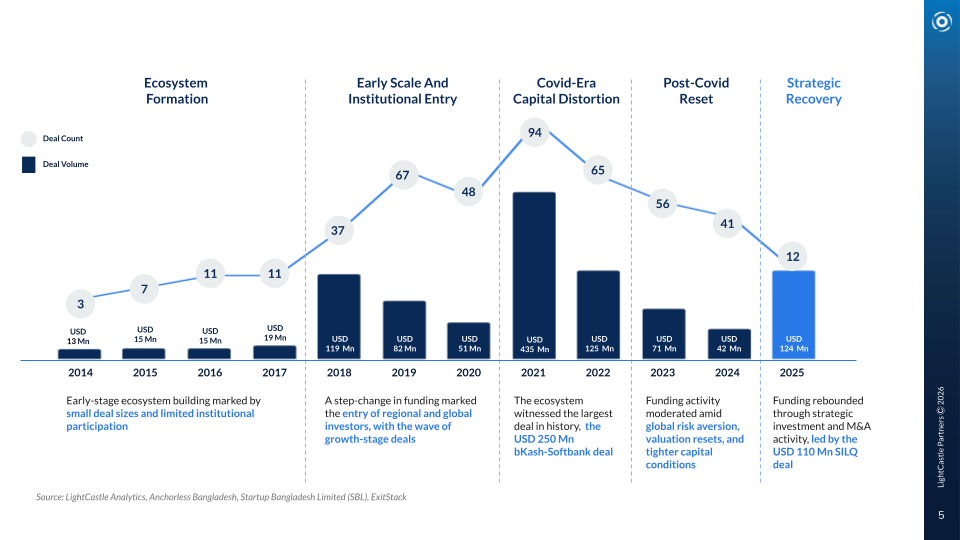

Between 2010 and 2025, Bangladesh’s startup ecosystem raised approximately USD 1 Bn across 450+ deals, marking a clear transition from sporadic early activity to a recognisable investment landscape. Yet the distribution of capital over time suggests that growth has not followed a steady upward trajectory. Instead, the ecosystem has witnessed periods of rapid inflows, with funding repeatedly concentrating around a small number of large transactions.

The early 2010s were marked by experimentation, with low and uneven funding volumes. Between 2013 and 2016, annual funding stabilised at modest levels while deal counts increased, reflecting a growing base of early-stage ventures. A structural shift occurred in 2018, when funding rose sharply, followed by broader participation at smaller ticket sizes in 2019. Momentum slowed during the COVID period, before peaking in 2021, which alone accounted for close to 40% of all startup funding since 2010, driven by large late-stage rounds in a small number of mature companies. The years that followed saw a sustained correction, with funding declining through 2024 despite continued deal activity. In 2025, funding rebounded, but through a small number of large transactions, indicating a selective return of capital.

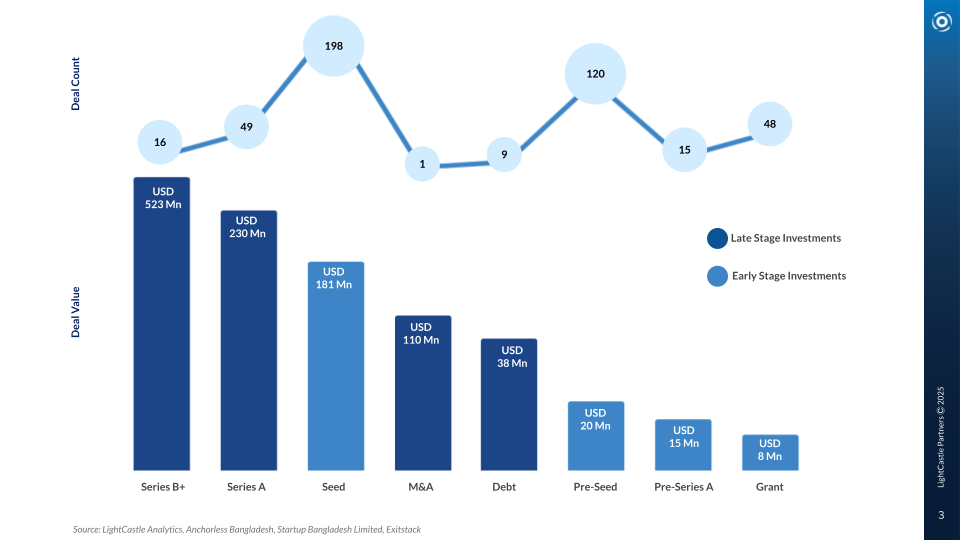

Early-stage rounds dominate deal volume but remain capital-light. Pre-seed and seed rounds together account for nearly 70% of transactions but less than 20% of total funding. At the other end of the spectrum, Series B captures nearly half of all startup funding and more than half of VC deployment, despite representing only a small fraction of deals. Debt and grant instruments have played a modest role in aggregate terms, though they remain important for specific sectors and early-stage experimentation. From an investor perspective, venture capital accounts for close to four-fifths of total funding. Angels and accelerators contribute heavily, while corporates, financial institutions, DFIs, and impact investors participate selectively, often tied to specific instruments or sectors rather than broad-based allocation.

Of the approximately USD 877 Mn deployed by VC investors, 57% flowed into Series B rounds, concentrated in the same small set of late-stage transactions. Series A absorbed around 15% of VC capital, while seed-stage VC accounted for roughly 12%, despite representing the largest share of deal volume. This pattern indicates that venture capital in Bangladesh has functioned primarily as a growth and scale-stage allocator, rather than as a broad early-stage risk capital provider. Early-stage layers have therefore relied more heavily on angels, accelerators, corporates, DFIs, and grant capital, particularly in sectors where commercial models take longer to mature.

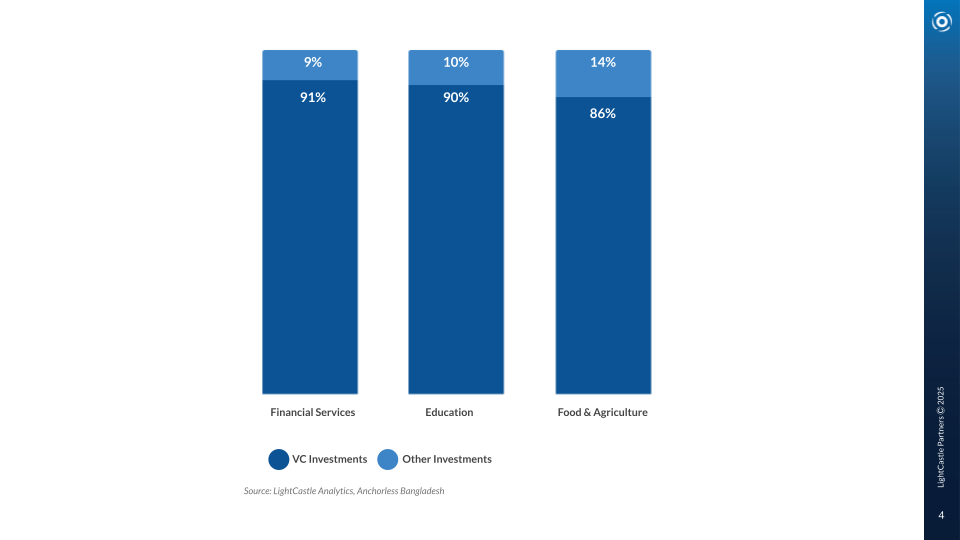

Venture capital deployment in Bangladesh has been notably concentrated in a small set of mass-market sectors, particularly financial services, education, and healthcare. In financial services, VC accounts for over 90% of total capital deployed, while education and healthcare show similarly high VC participation, each with around nine out of every ten dollars coming from venture investors. Even in food and agriculture, a sector often associated with concessional or impact capital, VC represents more than 85% of total investments.

These sectors share three defining characteristics: i) large addressable markets, ii) recurring demand, and iii) the potential for platform-led scale. Financial services benefit from transaction volumes and network effects, education and healthcare address persistent gaps in access and quality for large populations, and food and agriculture increasingly leverage technology to aggregate fragmented value chains. High VC participation suggests that investors view these sectors as capable of supporting venture-style outcomes once product–market fit and operational discipline are established.

Across most sectors, a single firm or a very small cluster of firms absorbs a greater share of overall sectoral funding. In education, two edtech firms alone have accounted for 86% of sectoral investments. In financial services, a handful of firms absorb nearly half of all funding, despite dozens of startups operating in the space. From an ecosystem perspective, it can be seen that capital does not diffuse evenly across firms. Instead, it consolidates rapidly around perceived category leaders, often after those firms demonstrate the ability to raise multiple rounds. Firms that have raised more than three rounds consistently command greater shares of sectoral funding, even when they are few in number. This suggests strong path dependence in capital allocation, where credibility compounds and follow-on capital concentrates.

Looking at capital recycling across sectors helps explain how investment decisions have evolved beyond first cheques. Rather than being distributed evenly across many startups, funding has tended to accumulate around a small number of companies that raise repeatedly, gradually increasing their share of total sectoral capital.

In several sectors, a single firm accounts for 40% of cumulative funding, while in more narrowly defined verticals, the share is higher. This is visible in education, financial services, logistics, e-Commerce, healthcare, and energy and climate, where one or two companies have progressed through multiple rounds and now anchor sector-level funding totals. What stands out is not the number of companies raising capital, but the sequence of follow-on rounds. Firms that have moved from seed to Series A and, in some cases, to Series B, have absorbed a growing share of investment over time. This pattern suggests that investors have placed increasing weight on operating track record, governance, and execution, rather than on initial market entry alone.

Startup investment trends suggest that Bangladesh has moved beyond a purely experimental startup phase. The ecosystem has demonstrated its ability to support scaled, venture-backed companies and attract large institutional rounds. At the same time, the pathway from early-stage experimentation to growth capital remains narrow.

The implications differ across stakeholders. Founders face a bottleneck not in early access to capital, but in progressing through the middle of the funding funnel. From an investor perspective, the data points to concentration risk at the top and a shallow opportunity set between seed and Series B. Meanwhile, for policymakers and ecosystem builders, the evidence establishes a clear baseline: over USD 1 billion has already flowed into Bangladeshi startups. The challenge now is to deepen pathways to scale rather than simply expanding entry.

This article was authored by Ameera Fairooz, a Senior Business Consultant at LightCastle Partners. For further clarifications, contact here: [email protected]

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights