GET IN TOUCH

- Please wait...

Nearly 45% of Bangladesh’s labor force depends on agriculture, and over 70% of rural households rely on it as their primary source of income, anchoring the sector’s role as the national livelihood backbone even as its share of GDP has fallen from 38% in the 1970s to 11.2% today.

Despite this declining GDP share, production value has grown at a steady 3.5% annually over the past two decades, a record of resilience that now confronts a more urgent question: does the FY 2026-27 budget meaningfully rebalance the sector’s financing realities, or does it simply add a development layer atop an unchanged subsidy core?

The headline number suggests momentum. Within the BDT 9.38 trillion total national budget (an 18.7% year-on-year increase), the Ministry of Agriculture’s (MoA) grant stands at BDT 288.8 billion, within a broad BDT 433.4 billion cluster allocation (0.63% of GDP) spanning agriculture, food, fisheries, and livestock [1][2].

Understanding what this allocation signals requires looking at how the composition of agricultural spending is changing, a distinction that enables an assessment of genuine structural reform versus a simply larger budget envelope.

The most-cited signal of this shift is the MoA development budget’s 96.5% surge, from BDT 40.4 billion (FY 2026 revised) to BDT 79.5 billion in FY 2027 [1][2]. In ratio terms, this lifts development spending from roughly 14% to over 27% of the total MoA grant.

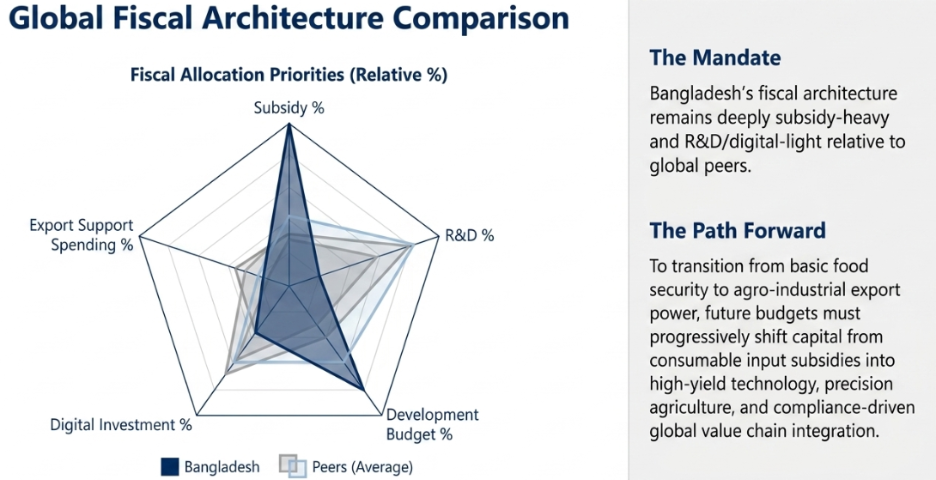

This shift matters beyond percentage point gain: it signals a maturing fiscal posture, one where public capital is increasingly directed toward productivity-enabling infrastructure rather than recurring input support, even as the development envelope remains the smaller half of the overall ledger.

Assessing the composition further, fertilizer subsidy remains BDT 170.01 billion, effectively flat in nominal terms [2]. The Farmer Card cash transfer, the Agri-Loan Waiver, and continued machinery subsidies taken together, recurrent and transfer-based support still constitutes the dominant share of agricultural spending. In FY 2027, the development envelope grew faster than the subsidy base for the first time in years, without displacing that base.

With this increased focus on development allocation, the more relevant lens is implementation efficiency and outcome quality, rather than allocation size alone. A BDT 79.5 billion figure encompasses: canal rehabilitation, irrigation modernization, and research and extension carry high long-term productivity returns; digital registries carry medium returns; administrative infrastructure and office construction carry comparatively little. The quality of this year’s development spending, more than its size, will determine whether the 96.5% increase translates into productivity gains or simply into a larger capital budget line.

The more important question, however, is “Why did such rebalancing become necessary in the first place?” The answer lies in a series of structural shifts to increasing focus on the sustainability of Bangladesh’s agricultural growth model [4][7]. This naturally extends to the global supply chain shocks and attempts by nations to secure supply lines.

Arable land has contracted from 8.11 million hectares (2021) to 7.88 million hectares (2023), a 0.52% annual shrinkage against 1.3% population growth [4]. Import dependency remains acute: 80% of fertilizer and 90–95% of maize seed are imported, while 60% of domestic urea capacity sits idle due to gas shortages [2][7].

This exposure is compounded by an increasingly fragmented global trade environment, escalating tariff disputes among major economies and supply-corridor disruptions linked to Middle East tensions, including Iran-related shipping risk, have added volatility to global fertilizer and grain logistics that Bangladesh, as a major net importer, cannot fully insulate against.

Post-harvest infrastructure gaps compound the problem, with an estimated USD 2.4 billion lost annually; 90% of cold storage capacity is locked into potatoes alone, and refrigerated transport accounts for under 1% of total freight [7]. Climate volatility adds a fourth layer: USD 800 million in average annual crop losses, with the August 2024 floods alone affecting over 400,000 hectares [4].

“Cold chain cannot be developed in a scattered manner. It must be designed across the full value chain, from production areas to consumers and beyond with proper backward and forward linkages.” – Mr. Ataus Sopan Malik, Managing Director, AR Malik Seeds

Against this, the resilience record is real. Rice self-sufficiency holds at 95%, cereal production rose 7.5% between FY 2022 and FY 2024, and 127 BRRI varieties, 39 of them stress-tolerant, now underpin over 80% of rice acreage [5]. Variety releases, however, is not the same as research investment. Funding for BRRI, BARI, BJRI, BINA, and university-led agricultural research has yet to scale in proportion to the productivity demands placed on these institutions, a gap that matters given how heavily future yield growth, climate resilience, and export competitiveness depend on sustained R&D output [5][6].

Everything considered: land pressure, import dependency, climate exposure, and evolving productivity demands, the FY 2027 budget advances three principal intervention areas intended to strengthen sector resilience and competitiveness [1][2].

“The Farmer Card should not be viewed only as a subsidy delivery tool. It can also be used to crowd in private investment, improve targeting, and support broader modernization of agriculture.” – Mr. Osman Haruni, Senior Policy Advisor, Embassy of the Kingdom of the Netherlands in Bangladesh

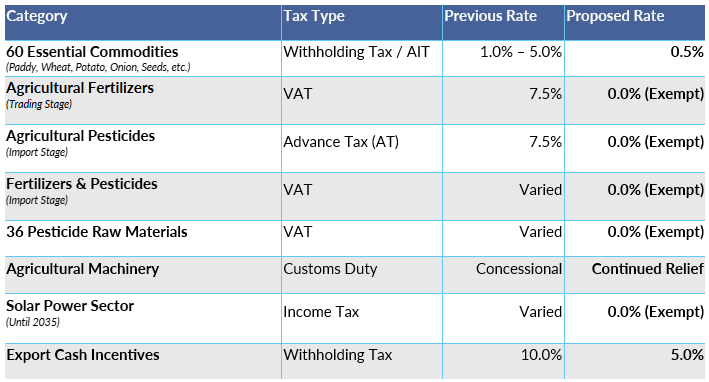

“The reduction of duties on essential commodities, fertilizer-related tariffs, and the introduction of the Farmer Card are positive signals. But the real test will be whether these measures translate into direct benefits for farmers at the field level.” – Mr. Anwar Faruque, Board of Director, Bangladesh Krishi Bank

Well-designed interventions ultimately depend on implementation quality. Bangladesh’s agricultural policy challenge has historically been less about identifying priorities and more about converting allocations into measurable outcomes [2][3].

Annual Development Program (ADP) execution fell from 95% in FY 2024 to 60% in FY 2025, and irrigation-linked projects have historically underperformed crop-production projects by close to 40% [2][3]. Mechanization allocations (BDT 30.2 billion) remain skewed toward rice combine harvesters, which absorbed 84% of past machinery subsidies [2].

The deeper issue lies with farm structure rather than equipment distribution: with fragmented smallholdings, individual farmers cannot independently justify harvesters or cold-chain investment. The more transformative question is whether allocations finance service-provider models, such as custom hiring centers and shared machinery enterprises, rather than individual ownership subsidies.

The budget also remains production-centric at a point where Bangladesh’s binding constraint is increasingly market access rather than output volume. Rice yields are relatively mature; future value capture depends on aggregation, storage, logistics, standards compliance, and traceability. The BDT 3.21 billion cold-chain allocation against a USD 2.4 billion annual loss illustrates the scale gap [7].

Wholesale market reform, contract farming, and farmer aggregation mechanisms, the channels that would let smallholders reach higher-value horticulture and export markets, receive little attention in current allocations.

Agricultural transformation also remains an institutional coordination challenge. While the Ministry of Agriculture leads sector policy, outcomes increasingly depend on alignment across agencies responsible for irrigation, water management, transport infrastructure, local government, commerce, and export facilitation.

As development allocations expand, coordination quality across these agencies will play a decisive role in determining whether higher capital expenditure produces systemic gains or fragmented ones [2][3][7].

“Moving forward, close coordination among ministries, departments, and relevant agencies will be essential to ensure effective monitoring and timely implementation of these measures at the field level.” – Mohammad Habibullah, Director, Admin and Finance Wing, DAE

FY 2026-27 represents an important transition from a subsidy-dominated agricultural support model toward a more investment-oriented framework, one that has yet to realize its full structural potential. The increase in development expenditure signals a policy recognition that future competitiveness will depend on productivity, climate resilience, post-harvest systems, and market connectivity. Whether this transition becomes structural rather than cyclical will depend on three factors:

This article was authored by M. Rakinul Islam, a Business Consultant working in the Development & Management Consulting department at LightCastle Partners. For further clarifications, contact us here: info@lightcastlepartners.com

Ainan Tajrian, Senior Business Consultant and Naziba Ali, Business Consultant provided editorial and insight support, leveraging the roundtable for action-oriented discussions and policy perspectives.

[1] Ministry of Finance (MoF), Budget Speech FY 2026-27

[2] Ministry of Agriculture, Demand for Grants (Grant No. 41)

[3] Medium-Term Expenditure Framework (MTEF) 2026-29

[4] Bangladesh Bureau of Statistics (BBS)

[5] Bangladesh Rice Research Institute (BRRI)

[6] Bangladesh Agricultural Research Institute (BARI)

[7] LightCastle Analytics Wing, Field Surveys, Key Informant Interviews, and Sector Analysis

[8] A Roundtable on National Budget FY 2026–27: Strategic Discussion on Crop Agriculture Hosted by LightCastle and SAF Bangladesh

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights