GET IN TOUCH

- Please wait...

Bangladesh’s next growth chapter will depend not only on sustaining external-sector momentum, but also on how effectively the country converts trade relationships into long-term US–Bangladesh economic investment partnership.

In FY2024–25, export earnings rose by 8.58 percent to USD 48.28 billion, while remittance inflows reached a record USD 30.33 billion, up 26.8 percent from the previous fiscal year.[1,2] With a labor force of around 74 million as of 2025, Bangladesh continues to offer a sizeable workforce, a growing domestic market, and a strategic position for international trade and investment.[3]

At the same time, the country is entering a more complex phase of economic diplomacy. Bangladesh is strengthening its trade architecture through engagements such as the Agreement on Reciprocal Trade (ART) with the United States, the Bangladesh–Japan Economic Partnership Agreement (EPA), and the Partnership and Cooperation Agreement (PCA) process with the European Union. These developments point to a gradual shift from preference-led trade toward more reciprocal, rules-based, and investment-oriented partnerships. [4,5,6]

Yet beneath this momentum lies a set of structural challenges. Bangladesh’s export base remains heavily concentrated in readymade garments, while gaps in the regulatory environment, energy security, logistics systems, and financial sector governance continue to weigh on investor confidence. Foreign Direct Investment stood at only 0.4 percent of nominal GDP as of June 2025, underscoring the need to translate commercial interest into long-term capital commitments.[7]

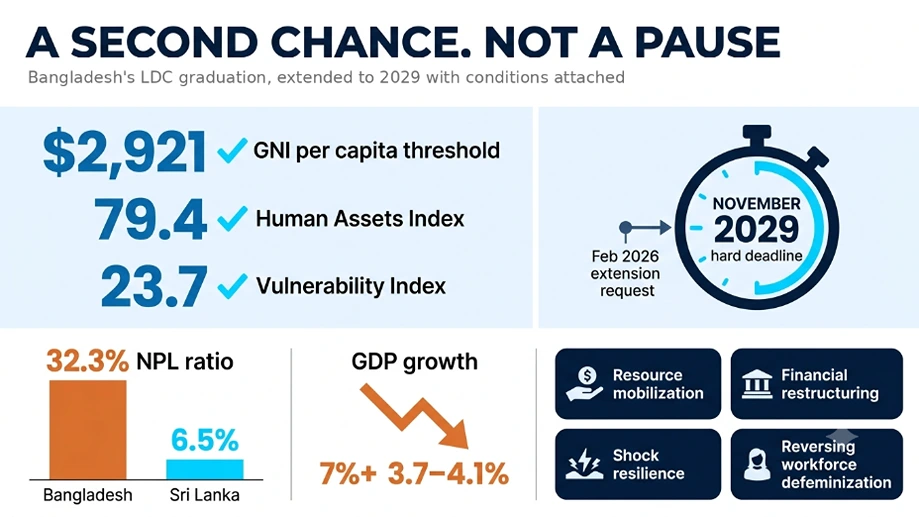

The country’s delayed graduation from Least Developed Country status to November 2029 provides Bangladesh with additional preparation time. However, this extension should not be treated as a pause in reform. Rather, it creates a narrow window to accelerate export diversification, improve regulatory predictability, strengthen energy infrastructure, and prepare the economy for a more competitive post-graduation trade environment.

The US–Bangladesh trade relationship remains commercially significant, but it is still driven overwhelmingly in apparel. In FY2024–25, readymade garments accounted for around 81.5 percent of Bangladesh’s total export income, with RMG exports reaching USD 39.35 billion.[8] The United States remained the largest destination for Bangladesh’s RMG exports, accounting for 19.2 percent of total RMG exports.[9]

This concentration reflects Bangladesh’s strong competitiveness in apparel, but it also exposes the economy to risks from demand shifts, compliance requirements, and tariff-related pressures in a single dominant sector. The need for export diversification is therefore not a long-term aspiration; it is an immediate competitiveness challenge.

Pharmaceuticals, leather, agro-products, and ICT have all been identified as priority sectors for diversification. However, each faces a different set of constraints. Pharmaceuticals, for example, already represent one of Bangladesh’s strongest non-RMG export opportunities, with local firms exporting to around 150 countries.

Yet entry into the US market remains constrained by expensive, time-consuming regulatory processes. Compliance with Food and Drug Administration approval, quality assurance, and documentation requirements will require targeted support if pharmaceuticals are to become a meaningful pillar of Bangladesh’s US export strategy.

ICT and digital services also remain underutilized in the bilateral trade relationship. Bangladesh has over 100 million internet users, and US firms such as Starlink, Google Pay, Oracle, and Microsoft are beginning to scale digital infrastructure and services in the country.

However, the sector has yet to convert this digital base into a stronger export relationship with the United States. For technology investment to expand, Bangladesh will need clearer regulatory pathways, faster approvals, and a digital business environment aligned with international standards.

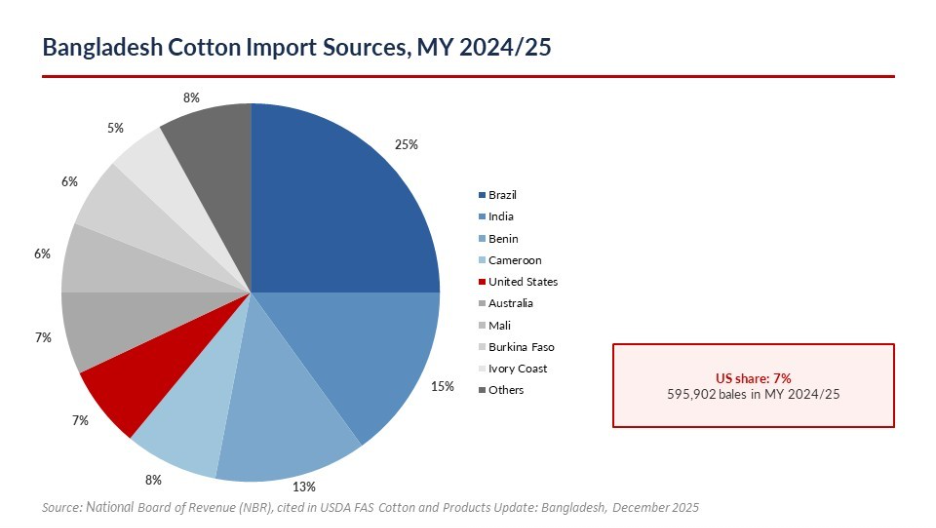

Even within RMG, a value-addition gap persists. A large share of Bangladesh’s US-bound apparel is cotton-based, yet US-origin cotton accounted for only 7% of Bangladesh’s raw cotton imports in MY 2024/25, ranking fifth behind Brazil, India, Benin, and Cameroon.[10]

Note: MY stands for Marketing Year, the 12-month reporting period used for agricultural production, trade, and consumption data.

The Agreement on Reciprocal Trade (ART) contains an explicit incentive to close this gap: preferential tariff treatment for products manufactured using US-origin cotton. The 30.5% growth in US cotton imports to 0.77 million bales in calendar year 2025suggests rising commercial interest among Bangladeshi spinners drawn to high-grade, contamination-free US cotton, but higher freight costs and longer lead times continue to favour West African and South American suppliers.[11] ‘

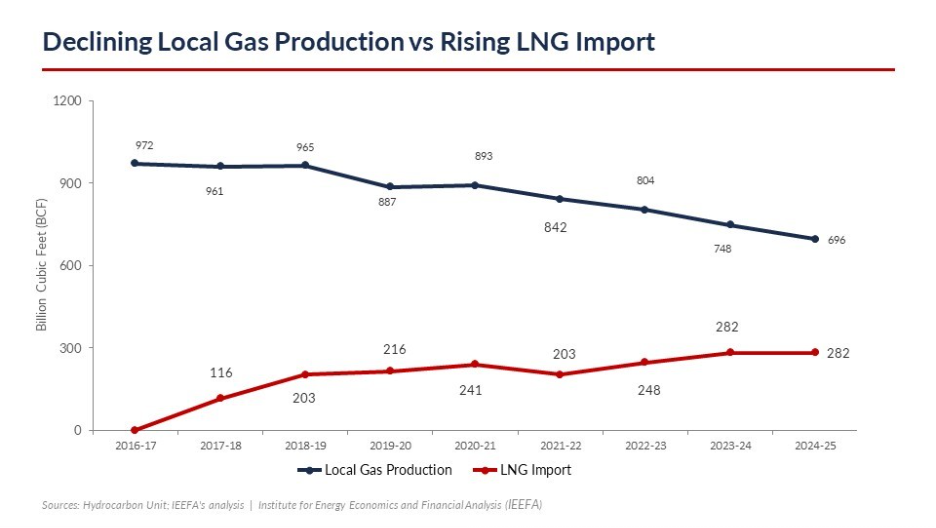

No discussion of Bangladesh’s investment climate can sidestep energy. For US companies evaluating Bangladesh as a manufacturing or investment destination, reliable and competitively priced energy is not a secondary consideration; it is a prerequisite. Disruptions in energy supply directly affect manufacturing output, erode margins, and undermine the investor confidence that Bangladesh urgently needs to build ahead of LDC graduation.

The data underscores the severity of the challenge. In FY2024–25, Bangladesh’s average gas supply was approximately 2,679 million cubic feet per day (mmcfd), against a demand of around 4,000 mmcfd, a shortfall of over 1,300 mmcfd.[12] This gap is not uniformly shared: the industrial sector bears a disproportionate burden, with factories operating on rationed supplies that curtail production capacity. Demand is projected to climb further to approximately 4,762 mmcfd by FY2027–28, driven primarily by the power and industrial sectors, with no commensurate increase in domestic production in sight.[13]

LNG imports have partially plugged the supply gap. US-based Excelerate Energy has played a central role through its floating storage and regasification infrastructure at Moheshkhali, expanding its terminal’s send-out capacity by 20% to 600 mmcfd in January 2024.[14] The Summit LNG terminal supplied around 13% of national gas demand in FY2024–25.[15]

But growing dependence on spot LNG cargoes, 35 procured between January and August 2025, compared with 21 in the same period the prior year, exposes Bangladesh to price volatility, foreign-exchange pressure, and supply disruption risks.[16] Cyclone Remal in 2024, which damaged FSRU operations and contributed to an acute gas crisis, offered a stark illustration of this vulnerability.

The pressure is also visible in the power sector. Petrobangla reportedly supplies around 850–900 mmcfd to power plants, against a sector requirement of more than 2,500 mmcfd, putting reliable electricity generation under pressure.[17] This reinforces the urgency of expanding gas supply, accelerating LNG infrastructure development, and structuring long-term energy partnerships to support both industrial production and power generation.

US companies already play a significant role in Bangladesh’s power sector. For Bangladesh, realizing the full potential of this partnership will require a more predictable, transparent, and contract-honoring investment environment, the foundational conditions that large-scale, long-horizon energy partnerships demand.

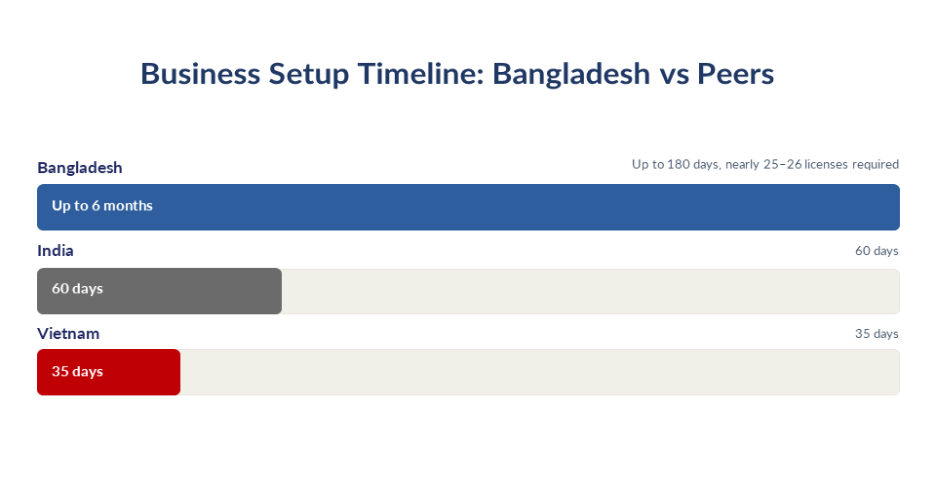

Bangladesh’s business start-up process takes up to 6 months and requires approximately 25–26 separate licenses, against 60 days in India and 35 days in Vietnam. [18] For US firms evaluating regional investment options, this is not a minor administrative hurdle; it is a competitive disadvantage that shapes capital allocation decisions before a single contract is signed.

Within that headline gap lie more specific structural rigidities. Import Registration Certificates (IRC) present practical difficulties for firms seeking to move from commercial to industrial operations, reflecting a registration architecture that does not accommodate how modern businesses scale across trading, manufacturing, and distribution. For companies considering a transition from importing to local production, this inflexibility translates directly into avoidable delays and compliance burden. Restrictions on foreign investment in warehousing similarly constrain international logistics firms, contributing to logistics costs estimated at around 16% of GDP, well above the global benchmark of 10%.[19] Process automation gaps compound both problems: regulatory workflows remain unevenly digitized, with manual documentation, repeated submissions, and fragmented approval chains persisting across agencies. The absence of integrated cross-agency clearance and paperless approvals keeps trade transactions slower and costlier than in competing destinations.

The cumulative effect is visible in investment figures: US FDI fell to USD 89 million in FY2023–24, a figure that reflects not only the global investment environment but a persistent gap between Bangladesh’s stated reform commitments and their on-the-ground implementation. [20] The challenge for prospective investors is less the existence of reform plans than whether rules are applied consistently, transparently, and within predictable timelines.

Bangladesh’s LDC graduation, now deferred to November 2029, represents one of the most consequential inflection points in the country’s economic history. The deferral buys time, but it does not eliminate the structural adjustment that graduation demands. Without a clear and credible transition strategy, Bangladesh risks managing the erosion of preferences and sectoral vulnerabilities without the policy architecture needed to sustain post-graduation growth.

The stakes are significant. UNCTAD estimates potential export losses of up to USD 17.5 billion, concentrated largely in apparel and footwear, while the WTO estimates annual export losses could reach USD 8 billion, equivalent to around 14% of total export earnings. [21,22] If Bangladesh fails to qualify for the EU’s GSP+ scheme, tariffs on apparel could rise from 0% to around 12%, while competing exporters such as Vietnam continue to benefit from preferential access under existing trade agreements. Bangladesh’s exposure is heightened by its narrow export base: as long as RMG dominates, the buffer against erosion of post-graduation preferences remains dangerously thin.

Compounding the graduation challenge is a financial sector that has yet to fully align with the requirements of a post-LDC economy. Non-performing loans, weak exit mechanisms for businesses, and inefficient state-owned enterprises continue to weigh on investor confidence. For US and other foreign investors, predictable rules for both market entry and exit are essential. Without stronger credibility in the financial sector and legal certainty, Bangladesh’s graduation strategy will remain incomplete regardless of what is achieved on the trade front.

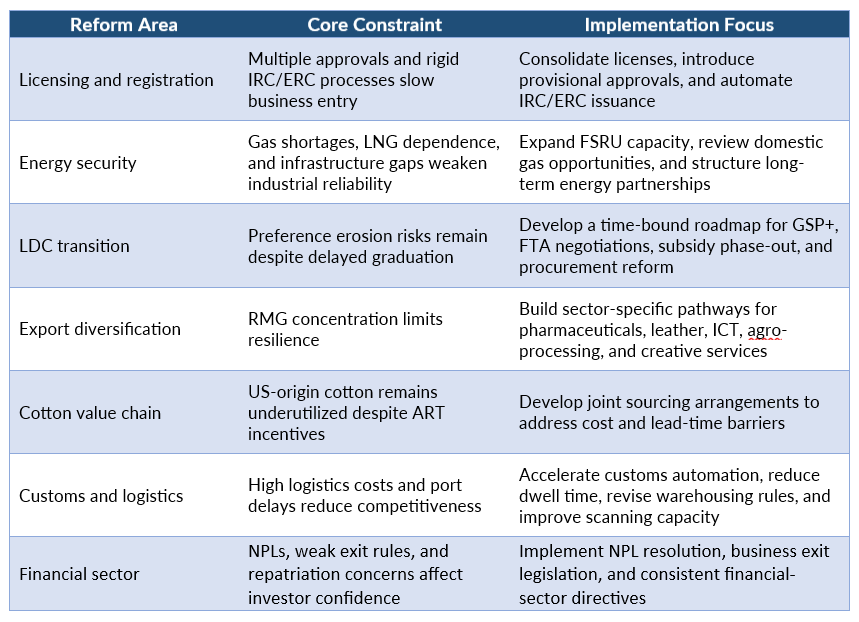

Table 1: Reform Priorities for Strengthening the US–Bangladesh Economic Partnership

Moving from opportunity scoping to implementation requires coordinated action across two fronts: structural reforms that only government can enable, and market-level decisions that industry leaders must drive. The following priorities reflect what both sides must now deliver.

Licensing reform is the most immediate unlock for investor confidence. Reducing the current 25–26 licensing requirements to a time-bound, consolidated framework, with provisional licenses issuable within days, would directly address one of the most-cited barriers to business entry. The Import Registration Certificate (IRC) policy should be reviewed to allow businesses to register for multiple activities, especially when they are moving from trading to manufacturing. At the same time, the issuance of the Import Registration Certificate (IRC) and Export Registration Certificate (ERC) should be fully automated through the Office of the Chief Controller of Imports and Exports (CCI&E). This system should also be integrated with the Registrar of Joint Stock Companies and Firms (RJSC) company registration process, so that businesses do not have to submit the same information multiple times. These reforms would help move the agenda from planning to implementation and reduce barriers that discourage investment in Bangladesh.

On energy, the priority is both infrastructure and partnerships. The government should prioritize competitive tenders for new Floating Storage and Regasification Unit (FSRU) infrastructure, enable greater private-sector participation in state-owned energy assets, and expand domestic gas production where commercially viable. Chevron Bangladesh’s proposal to the Energy and Mineral Resources Division (EMRD) to increase low-cost domestic gas production deserves priority review as an opportunity to reduce dependence on high-cost LNG imports. The USD 15 billion energy commitment under the ART should be operationalized through structured long-term off-take agreements with US energy firms, while Bangladesh accelerates private-sector participation in renewable energy, including the proposed 10,000 MW solar expansion ,to diversify the energy mix and strengthen the foundation for industrial growth.

Bangladesh also needs a clear, time-bound transition plan for its delayed LDC graduation. This should cover GSP+ eligibility, FTA negotiations, export subsidy phase-out, and transparent procurement for major infrastructure projects. A credible roadmap would help Bangladesh manage preference erosion while strengthening investor confidence in government decision-making.

Export diversification requires a sector-by-sector roadmap, not a general aspiration. A government-backed roadmap to help pharmaceutical companies meet US FDA standards and access the US market would move the sector from promise to pipeline. Sector-specific incentive frameworks for leather, light manufacturing, ICT, and agro-processing, combined with formal recognition of the advertising and creative services sector under the Ministry of Commerce, would broaden the commercial base that Bangladesh will need after graduation. At the industry level, BGMEA and spinning mills should actively expand procurement of US-origin cotton, progressively raising the current 7 percent share toward a commercially competitive level, and develop joint sourcing arrangements with US cotton exporters to address the lead-time and freight-cost barriers that currently limit wider adoption.

Customs, logistics, and digital adoption must move in parallel. Accelerating customs automation and reducing cargo dwell times at key ports are prerequisites for trade competitiveness. Revising the foreign investment cap on warehousing and investing in advanced cargo-scanning equipment would reduce logistics costs from the current 16 percent of GDP to the global benchmark of 10 percent. Corporations should promote cashless transactions and adopt digital compliance tools across their operations, and industry associations should advocate consistently for the removal of barriers that prevent international logistics firms from scaling in Bangladesh.

Banking sector reform is the foundation beneath everything else. Implementing a credible Non-Performing Loan resolution programme, enacting business exit legislation modelled on international frameworks, and guaranteeing the unrestricted repatriation of profit and capital would signal to long-horizon investors that Bangladesh is serious about the rule of law. Ensuring that Bangladesh Bank directives are consistently implemented across all financial institutions is not a technical matter; it is a credibility matter.

Bringing these priorities together is a bilateral framework built on six foundational principles: trust and honored agreements, policy predictability, transparency, a clear regulatory framework, digitized procedures, and alignment with global standards. These are not aspirational values, they are the operational conditions that investors require before committing capital at scale. Bangladesh’s reform agenda, if delivered consistently and at pace, can position the country as a more competitive, diversified, and credible trade and investment partner in South Asia.

This article was authored by Faiza Tahiya, a Business Analyst at LightCastle Partners. For further clarifications, contact us here: [email protected]

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights