GET IN TOUCH

- Please wait...

The global fashion industry’s relentless pace of production has quietly generated one of the most pressing environmental crises of our time. An estimated 121 million metric tonnes of textile waste are generated annually, a figure projected to surge to 180 million metric tonnes by 2035. A prevailing lack of advancing circularity, with less than 1% of the waste recycled; the overwhelming majority is either incinerated or landfilled, leaving behind a trail of environmental harm across the world.1

Beneath these numbers lies a deeper depiction of the stagnation of circularity. The textile value chain, built on a fundamentally linear model of take, make, and dispose, has long treated waste as an inevitable by-product rather than a resource. As consumer demand for fashion clothing shows no sign of abating, the question is no longer whether circularity is desirable; it is whether the industry can afford to operate without it.

Closing this loop has, therefore, moved from aspiration to imperative. To deliberate on the pathways forward, LightCastle Partners hosted a 2nd closed-door roundtable on circularity as part of the Bunon 2030 initiative, under the ‘Oporajita: Just Transition for Women in the RMG Ecosystem’ initiative, supported by the H&M Foundation, Sweden, and COS, and managed by The Asia Foundation as the backbone organization, on 2nd April, 2026, at Six Seasons, Dhaka.

The session convened industry leaders, sustainability practitioners, and development partners, BGMEA, SMEF and other esteemed stakeholders to examine the structural, financial, and policy dimensions of embedding circularity within Bangladesh’s textile value chain.

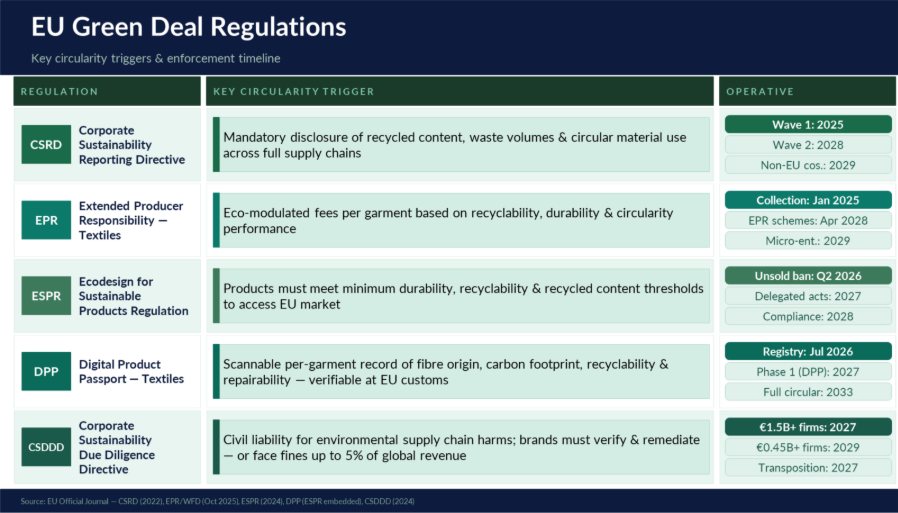

The regulatory landscape is shifting fast, and for Bangladesh’s RMG suppliers, the margin for inaction is narrowing. The European Union’s sweeping green policy agenda is no longer a distant horizon; it is arriving in successive, binding waves that are fundamentally rewriting the rules of market access.

The Corporate Sustainability Reporting Directive (CSRD) now mandates that companies disclose recycled content, waste volumes, and circular material use across their full supply chains, moving sustainability from voluntary commitment to verifiable obligation. Alongside it, Extended Producer Responsibility (EPR) frameworks introduce eco-modulated fees that tie the cost a brand pays directly to how circular, durable, and recyclable its products are. For the first time at EU-wide scale, non-circular sourcing carries a direct financial penalty, making circularity not merely an ethical preference, but a commercial calculation.

Perhaps most consequentially, the Digital Product Passport (DPP) under the Ecodesign for Sustainable Products Regulation (ESPR) is set to transform supply chain transparency. Planned across three progressive phases, once a product category’s delegated act is adopted, each product has to carry a passport, deepening required traceability from basic material origin all the way to full lifecycle circularity records. Compliance will be verifiable at the border, leaving little room for opaque sourcing or unsubstantiated green claims.

These converging regulatory imperatives have already begun reshaping buyer mandates. Leading global brands, including H&M, have integrated circularity as a core sourcing requirement, compelling suppliers across their value chains to align with these standards or risk losing access to one of the world’s most significant apparel markets.

Echoing this, during the roundtable, Mohammad Monower Hossain, Head of Sustainability at Team Group, underscored the unavoidable nature of this shift, noting that under EPR and ESPR frameworks, even the destruction of waste is no longer permissible. He argued that navigating these constraints demands nothing short of top-level political commitment to drive structural change from above.

Amid the urgency of regulatory compliance and market access, it is easy to overlook a quieter but equally consequential reality: Bangladesh already has a circular economy, and millions of workers are holding it together.

Research presented by Kumar Prashant, Research Analyst at Circle Economy, as part of the SWITCH2CE project, offered a revealing portrait of this largely invisible workforce. An estimated 3.8 million workers in Bangladesh are currently employed in circular activities, nearly double the global average rate of participation, excluding agriculture. Yet the overwhelming majority operate in the informal sector, without the protections, recognition, or investment that their role in the value chain warrants.

This finding carries an important implication for how the sector frames its transition agenda. As Prashant observed, “Scaling up circularity will not automatically lead to advancements in decent work without a deliberate attempt.” The jobs, in other words, already exist. The task is not creation, it is transformation: converting precarious, poorly documented informal livelihoods into decent, future-ready work.

Following Circle Economy’s key findings, the roundtable discussion turned to the actionable examination of the imperatives that Bangladesh’s textile and RMG factories urgently need to internalize to embed circularity at the core of their operations.

A foundational challenge surfaced early in the discussion: Bangladesh sits atop an abundance of jhoot (pre-consumer textile waste) yet is unable to harness it. The formal recyclers operating within the country are often compelled to import the very raw material that is being exported from their own backyard. Third-party intermediaries, incentivised by higher prices abroad, routinely channel jhoot to markets such as India, leaving domestic recyclers starved of supply and forced to source at a premium.

In addition, the lack of financial incentives for local jhoot recyclers also presents an obstacle. Without concessional financing, viable business cases, or policy support to make domestic utilization commercially attractive, the formal recycling ecosystem struggles to compete with informal export channels.

Rizvan Hasan, Country Head at Reverse Resources, captured the scale of this misalignment plainly, noting that Bangladesh loses an estimated $500 million annually by exporting or downcycling pre-consumer waste rather than retaining and upcycling it domestically. He further pointed to the tax structure as an additional barrier.

Furthermore, the discussion also highlighted that circularity cannot be reduced to waste recovery alone. The most impactful interventions, as several participants noted, begin long before a garment is made, at the fiber and yarn selection stage, where inefficient resource use quietly transforms into a larger waste burden downstream. True circularity demands a shift in orientation: from remediation after the fact to prevention by design.

The roundtable’s key insights extended well beyond textile recycling. As water scarcity intensifies globally, participants also turned their attention to a challenge closer to home, the urgent need to manage industrial wastewater and protect Bangladesh’s rapidly depleting groundwater reserves.

The textile sector’s water footprint is as consequential as its waste footprint, yet it receives a fraction of the policy’s attention. Yeasin Arafat, Technical Expert at WaterAid, brought this into sharp focus, highlighting how intensive groundwater extraction across Bangladesh’s industrial corridors has steadily depleted groundwater levels, creating a slow-moving environmental crisis that the sector has been too slow to confront.

Yet solutions are already being demonstrated on the ground. He further pointed to IoT-based wastewater monitoring systems as a proven and scalable technological response, stating WaterAid’s own operational case in Saidpur as evidence that real-time monitoring can meaningfully curb wasteful extraction and improve industrial water management. The challenge is that such innovations remain isolated pilots rather than sector-wide practice and should call for their nationwide adoption across textile and RMG clusters.

The roundtable closed with a forward-looking consensus: Bangladesh’s circularity transition is not a distant aspiration but an immediate necessity, and the building blocks, however imperfect, are already in place.

In response to this, the distinguished participants offered a perspective that reframed the regulatory pressure discussed throughout the session into a tangible opportunity. The European Union remains actively interested in deepening trade ties with Bangladesh, including the prospect of a Free Trade Agreement that could unlock preferential market access at a critical juncture. It is the entry ticket to a deeper trade relationship that could define Bangladesh’s export trajectory for decades.

Side by side, K. M. Asadun Noor, National Project Coordinator at UNIDO, pointed to the foundations that must be urgently strengthened. Learnings from SWTICH2CE pilots with leading brands have shown that while Tier 1 suppliers are increasingly capable of meeting circularity requirements, Tier 2 and Tier 3 SMEs remain underserved, often forgotten in policy conversations, despite being integral to the value chain. He further highlighted the absence of bankable business cases for textile waste recycling as a persistent barrier, noting that financial institutions cannot engage with a sector that cannot present credible, investable proposals. On a more encouraging note, a National Circular Economy Strategy, submitted to the Ministry of Commerce in late 2025, is expected to be published by year’s end, offering a long-overdue policy anchor for the sector’s transition.

Dr. Zaki Uz Zaman, Former Country Representative at UNIDO, echoed this call for institutional ambition, drawing attention to Bangladesh’s 2015 National Quality Policy, which has remained effectively dormant for a decade despite its potential to enable bilateral trade agreements and integrate circularity standards. Revisiting this policy, he argued, could unlock significant FTA opportunities while embedding circular economy principles into national trade architecture.

At the end, the roundtable painted a picture of a sector standing at an inflection point. The regulatory imperatives are arriving. The workforce is already there. The waste streams are abundant. The financing, however imperfect, exists. What remains is the collective will, across factories, policymakers, financiers, and development partners, to move from fragmented pilots to systemic transformation. Bangladesh has long sewn the world’s garments. The task now is to stitch together a circular economy worthy of that scale.

Sadia Karim, a Business Consultant at LightCastle Partners, has prepared the write-up. For more information, please contact at [email protected]

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights