GET IN TOUCH

- Please wait...

Over the past few years, corporate Bangladesh’s ESG scores has entered global datasets at an accelerating pace, expanding from seven mentions in 20231 to a cohort of sixteen listed firms spanning telecom, banking, manufacturing, and consumer sectors2. Yet, despite this expanded visibility, reported scores remain modest relative to developed market benchmarks.

At face value, this gap is often interpreted as a proxy for weak sustainability performance. However, such a conclusion risks oversimplifying a far more structural reality. In many cases, the discrepancy reflects asymmetries in disclosure systems, measurement standards, and data maturity rather than deficit in on-ground sustainability practices. Much like broader narratives around climate and environmental systems, prevailing assumptions here tend to conflate visibility with performance, and absence of data with absence of action.

ESG metrics do not evaluate sustainability in isolation. They measure the visibility, consistency, and comparability of risk. Capital markets do not have price intent; they price uncertainty. From this perspective, Bangladesh’s ESG profile is not a failure signal, it is rather a transition signal, reflecting a shift from opaque production systems to measurable, verifiable enterprises – foreshadowing the era of the Digital Product Passports (DPP).

The confusion originates in how ESG scores, in our reference the one by Bloomberg, are constructed.

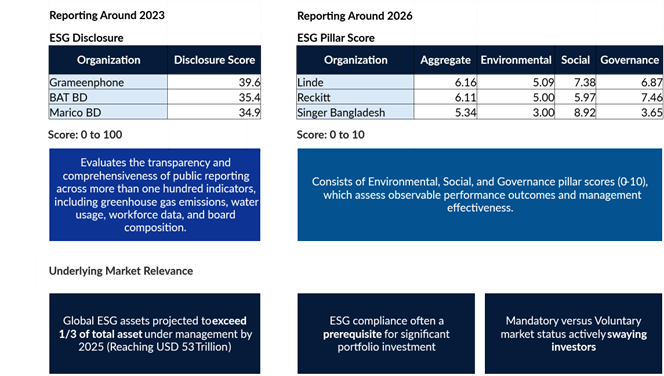

At a structural level, the system operates across two layers. The first is a Disclosure Score (0–100), which evaluates how comprehensively firms report data across more than 120 indicators, including emissions, workforce composition, and governance structures. This score captures transparency, not sustainable performance.

The second layer consists of Performance Pillar Scores (0–10) across Environmental, Social, and Governance dimensions. However, these are not independent measures. They are mechanically constrained by disclosure completeness. When firms fail to report quantitative data, the maximum achievable performance score is reduced, regardless of actual operational outcomes.

This creates structural asymmetry. Firms that do not disclose are not treated as neutral; they are treated as unverifiable. In the absence of reported data, Bloomberg applies model-based estimates using sectoral and regional proxies3. While this ensures baseline comparability, it takes firm-level nuance. As a result, unreported performance is systematically discounted, and companies are penalized not just for poor practice but for a lack of measurable evidence.

At the organizational level, the data reinforces uneven visibility. It is not that Bangladesh is uniformly underperforming, rather that even within industries, the scores can drastically vary depending on what (and in turn how) the organization discloses ESG activities.

Firms that have invested in structured measurement and disclosure systems achieve significantly higher scores4:

Comparatively higher scores around social and governance infer early focus and development initiatives in labor rights and wellbeing reporting. An example being the ILO’s member factory inspection as a standardized benchmark. They demonstrate that when measurement infrastructure exists, Bangladeshi firms can perform competitively within global ESG frameworks.

In contrast, several large domestic industrial players, despite their scale and operational significance, score markedly lower. LafargeHolcim Bangladesh records an aggregate score of 2.07, while other major industrial peers languish at 1.83 and 1.45. This is despite the major cement producer structuring operations and manufacturing sustainability efforts aiming towards net-zero emissions.

Even within heavy industries, visibility dictates the ceiling of success. While power and cement inherently face steep environmental penalties, a lack of quantitative disclosure artificially caps their maximum possible scores. Firms with embedded systems convert operational activity into recognized ESG performance. Those without are algorithmically estimated using punitive regional proxies. This drags them to the bottom of global benchmarks regardless of their on-ground sustainable practices.

Across a long spreadsheet of disclosures, these proxies and low rank make the organization invisible to the investor immediately. Even if spotted, this unverifiable disclosure increases the investor’s risk and makes their capital costlier.

Global capital is rapidly embedding ESG into investment decision-making. ESG-linked assets should have already surpassed USD 50 trillion by 20255, and institutional investors, particularly in Europe and North America, now treat ESG compliance as a baseline requirement rather than a differentiator.

At the same time, regional competitors are moving decisively. India has implemented its mandatory Business Responsibility and Sustainability Report (BRSR) framework6, while other Southeast Asian markets are formalizing ESG disclosure requirements for listed firms7. These shifts are reducing information asymmetry and enhancing investor confidence across peer markets. Bangladesh remains largely voluntary8.

This divergence creates what can be termed as an auditability premium. Investors and lenders cannot physically verify operations; they rely on structured disclosures to assess risk remotely. In the absence of data, the risk assumptions increase, and so do the cost of capital.

The implications are immediate and material. Firms without standardized ESG disclosures face higher borrowing costs, restricted access to ESG-screened funds, and growing exclusion from global supply chains that increasingly require traceability and compliance documentation. Competitiveness is therefore shifting from cost efficiency to verifiability.

The country is home to the highest number of green apparel factories globally (268 facilities), and exporters are rapidly adopting sustainable practices. This is evidence of extensive on-the-ground compliance. However, these efforts exist as parallel mechanisms rather than a unified reporting architecture.

Due to this voluntary nature, even sectors under strict regulatory oversight like banking and telecom only provide comprehensive ESG disclosure if requested by primary regulators, foreign investors, or international clients. This lack of standardization leads to sectors creating custom reports as required exhausting resources. The constraint is not a lack of regulation.

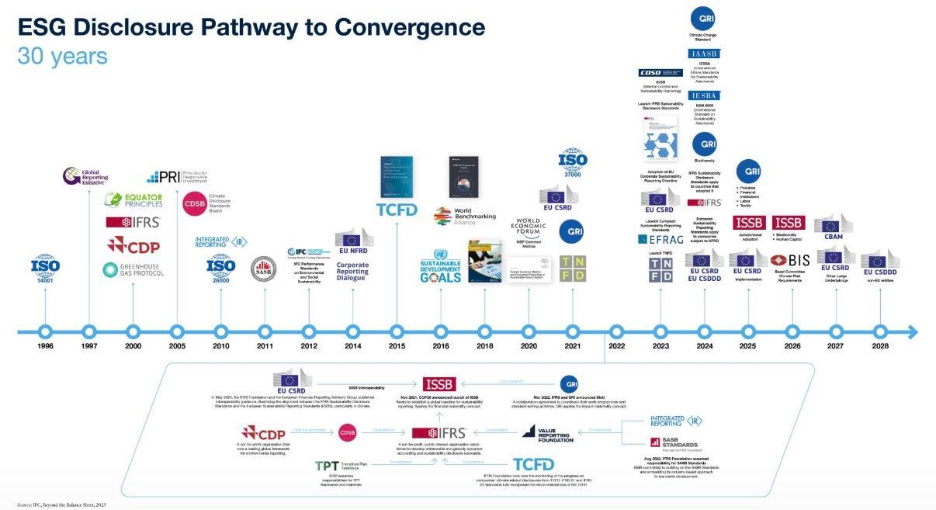

The gap lies in translation. Local compliance frameworks do not automatically align with global reporting standards such as the Global Reporting Initiative (GRI), the Sustainability Accounting Standards Board (SASB), or the International Sustainability Standards Board (ISSB)2. These frameworks are not simply reporting tools; they are data architectures that enable machine-readable, cross-country comparability.

Global capital allocation is increasingly algorithm driven. Investors rely on standardized datasets that allow them to benchmark firms across geographies in real time. A textile manufacturer in Dhaka must be interpretable within the same analytical framework as a peer in Vietnam or Turkey. Without this interoperability, performance remains economically unrecognized. The requirement is therefore standardized reporting in a globally accepted language, not more reporting.

Closing this visibility gap requires coordinated action across corporate, regulatory, and ecosystem levels:

Bangladesh’s ESG scores should not be solely read as a verdict on sustainability performance. They are a measure of system readiness for global capital integration.

The country has already built its production base, scaled its export industries, and integrated into global value chains. The next phase of competitiveness is different. It requires institutionalized transparency, where performance is not only achieved but continuously measured, verified, and communicated in a comparable format.

In a global economy increasingly defined by traceability, compliance, and data-driven decision-making, value accrues to what can be proven. The strategic question for Bangladeshi firms now is whether they are legible to capital.

Bangladesh has built the factories – the next competitive frontier is auditability.

This article has been largely based on Bloomberg’s ESG rating, widely reported by the news media and organizations in Bangladesh. It is best to mention that no consolidated, Bloomberg-published report collates these ratings. They are accessible for businesses to review in the Bloomberg Corporate Web Portal. The article in no way intends to comment on the rating systems and only uses Bloomberg as a reference due to its relevance/popularity amongst Bangladeshi organizations. The intention is to highlight how these ratings can be multi-fold and focused for a specific audience requirement.

This article was authored by M. Rakinul Islam, a Business Consultant working in the Development & Management Consulting department at LightCastle Partners.

For further clarifications, contact us here: [email protected]

[1] 7 Bangladeshi firms make it into Bloomberg’s sustainability list, The Business Standard

[2] Sixteen Bangladesh Companies Featured in Bloomberg ESG Universe, Markedium (Feb 2026)

[3] Bloomberg ESG Scores Methodology, Bloomberg (Dec 2025)

[4] Bloomberg ESG Score of Bangladeshi Firms, BRAC EPL (Jan 2026)

[5] ESG assets may hit $53 trillion by 2025, a third of global AUM, Bloomberg Professional Services (Feb 2021)

[6] Business Responsibility and Sustainability Report (BRSR) Framework, EY (2023)

[7] Thailand Securities and Exchange Commission Sustainability Reporting Requirements, IFRS Sustainability (Jun 2025)

[8] Sustainability Reporting and Integration of SDGs – The Bangladesh Status, GRI (Jan 2024)

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights