GET IN TOUCH

- Please wait...

Bangladesh’s Ready-Made Garment (RMG) industry accounts for over 84% of national exports and employs more than 4 million workers. Most of whom are women (World Bank, 2023), making it the engine of the country’s economy. But this success did not happen by accident. Decades of targeted government support, including duty-free imports, bonded warehouse facilities, tax breaks, and preferential market access, deliberately channeled the country’s export energy into a single sector (ADB, 2024). The result is a remarkable industry, but also a risky one.

As Bangladesh prepares to graduate from its Least Developed Country (LDC) status, these long-enjoyed privileges will begin to fade. Making RMG exports more expensive and less competitive on the global stage. And leaving an economy that has put most of its eggs in one basket increasingly exposed to external shocks. The good news, however, is that the very policy tools that built the RMG sector can now be turned toward building the next one.

The leather and leather goods industry, recognized as a priority sector in Bangladesh’s Export Policy 2021–2024, sits on a foundation of raw material access, growing domestic demand, and strong employment potential (CPD, 2024). However, it lacks compliance standards, design capacity, and global market connections, are precisely what the RMG sector has spent decades developing. With the right policy push, the Bangladesh leather sector growth does not need to start from scratch. It can use the infrastructure, institutions, and lessons of its garment success story to write a new one.

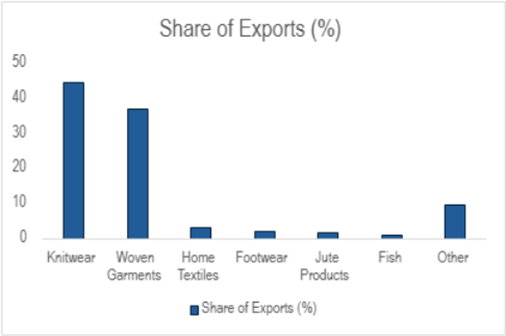

The data clearly depicts how the export of Bangladesh is concentrated only in RMG. It is evidential that we need to diversify our export basket to make our economy less volatile. Thus more resilient towards internal and external shocks like pandemics, geopolitical issues, and calamities.

Integrating Bangladesh’s leather and RMG sectors promises significant value chain synergies, but several challenges must be addressed to realize this potential.

As highlighted in the ADB (2024) report, a major demand-side issue is the informal export of raw leather to neighboring countries. This practice forces domestic manufacturers to import processed leather at higher costs, reducing local value addition and undermining competitiveness.

Bangladesh’s NBR Customs Tariff 2025–2026 reveals a critical structural gap. Raw hides and skins attract a Total Tax Incidence of just 7–10%, while finished leather goods face up to 89.32%, yet there is no export levy or duty on raw hides leaving the country. This shows that, Bangladesh is protecting its finished goods market from outside competition while leaving raw material free to exit unprocessed which is becoming a hindrance on the growth of the leather sector specially for finished goods.

Current infrastructure constraints limit Bangladesh’s ability to produce finished leather goods at scale and quality levels demanded by global buyers. Without targeted investments in processing facilities and workforce upskilling, the country risks being a low-value raw material exporter rather than a high-value finished goods producer.

Fluctuations in the Bangladeshi Taka increase the cost of imported inputs, further elevating production costs for finished leather products. This volatility complicates pricing and profitability, making integration with the RMG sector financially riskier.

Leather SMEs often lack the certifications, quality control systems, and environmental standards familiar to RMG exporters. Without alignment on social, environmental, and production compliance, integrating these sectors for global lifestyle brands may face significant hurdles.

Addressing these challenges requires coordinated policy intervention, infrastructure investment, and capacity building. Only by tackling raw material leakage, scaling domestic production, and ensuring regulatory and compliance alignment can Bangladesh successfully integrate its leather and RMG sectors into a sustainable, high-value export ecosystem.

Hausmann and Hidalgo’s Product Space framework offers a powerful lens through which to understand Bangladesh’s leather sector opportunity. Countries move from the products they already produce to others that are similar in terms of capital requirements, knowledge, and skills and the key challenge in any diversification process is identifying sectors that are both feasible given existing productive capabilities and have higher potential to sustain economic development.

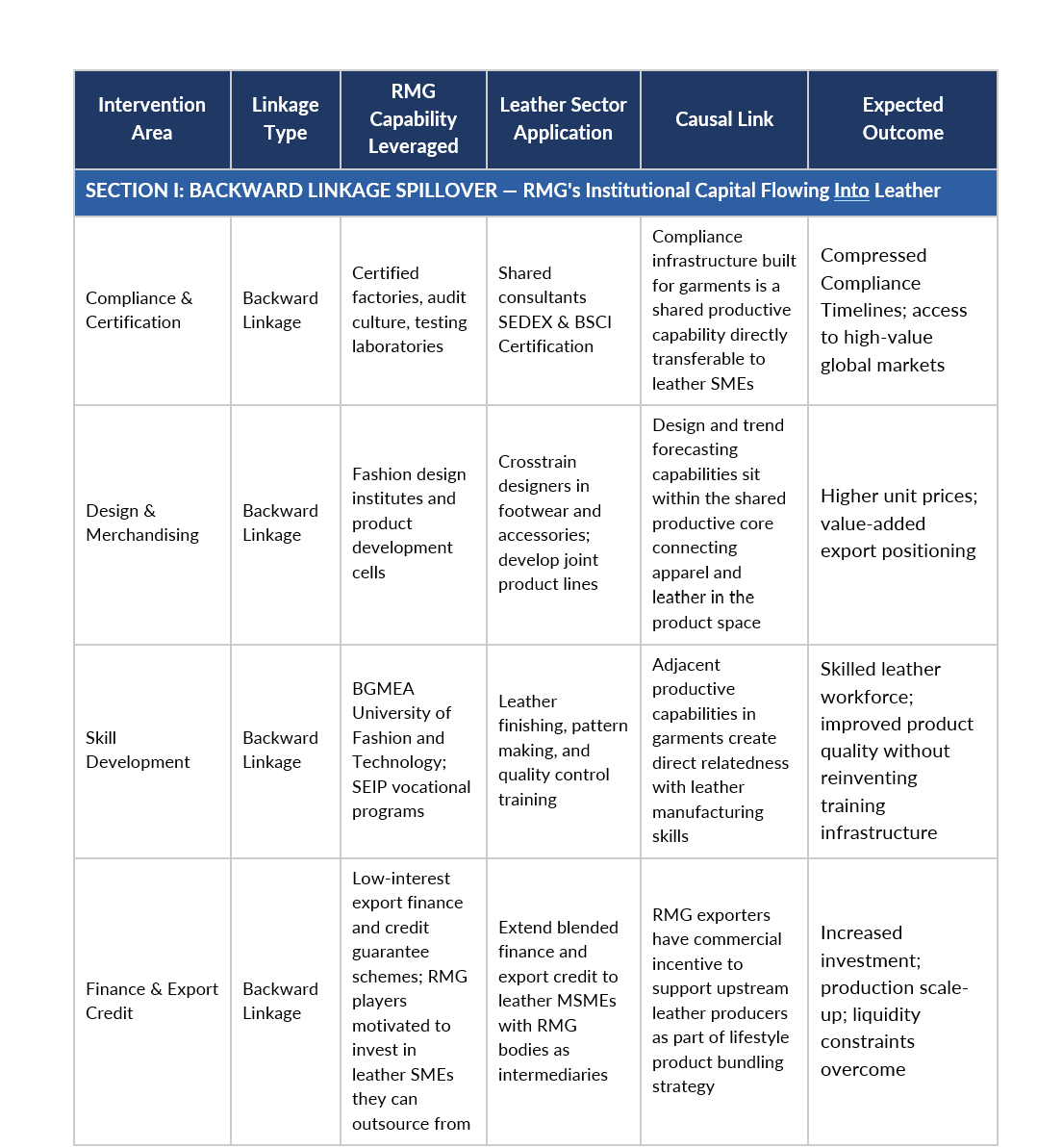

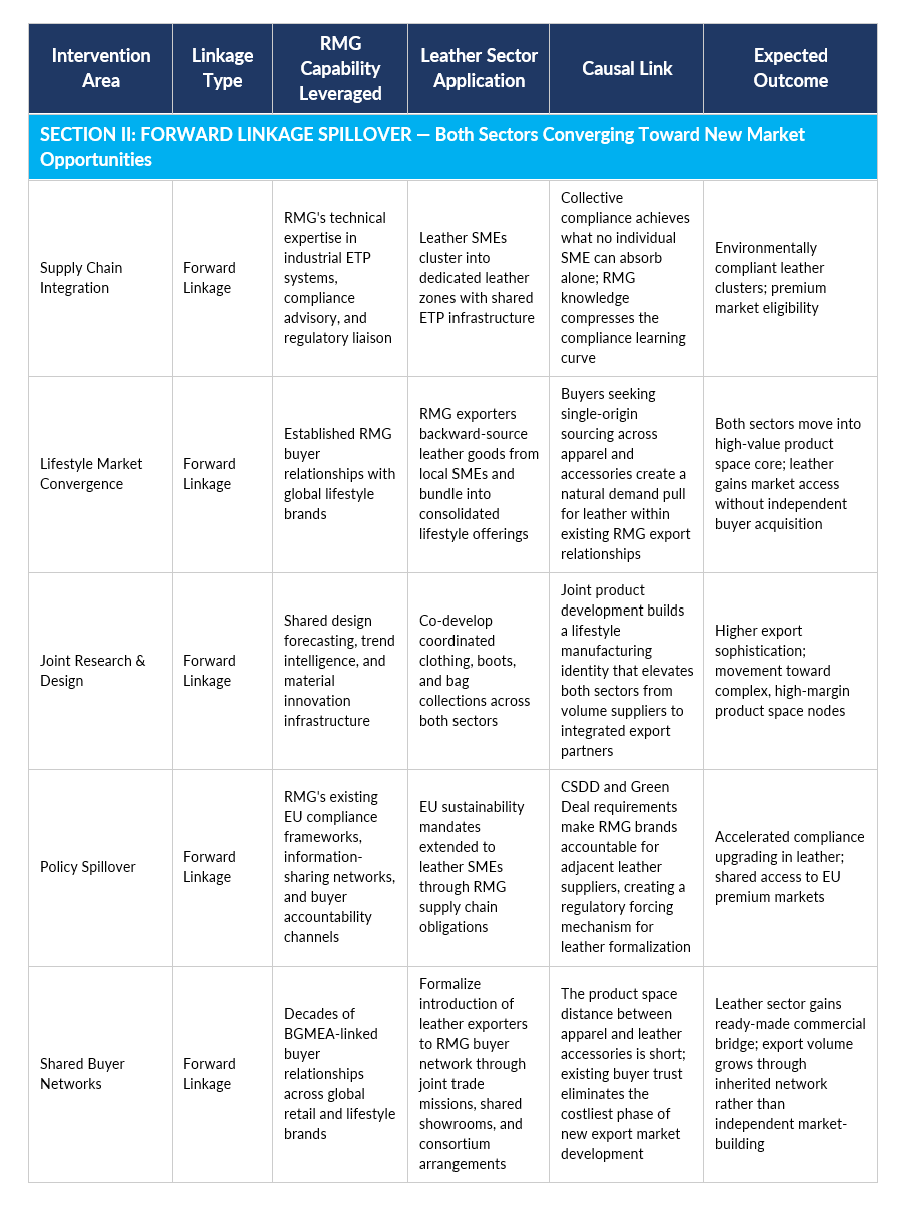

Leather goods and garments are adjacent nodes in Bangladesh’s product space. They share buyer networks, compliance cultures, design competencies, and labor skill sets. The spillover, therefore, does not require a leap; it requires a deliberate policy to nudge across a short distance. That nudge operates through two distinct but complementary channels: backward linkages, where the RMG sector’s accumulated institutional capital flows into leather, and forward linkages, where both sectors converge to create new, higher-value market opportunities together.

Hirschman’s backward linkage theory describes how a developing industry can draw upon the institutional capital and capabilities of an already established sector to accelerate its own growth. In Bangladesh’s context, the leather sector reaches backward into RMG’s already built ecosystem — its buyer networks, compliance frameworks, training institutions, and export finance channels — absorbing decades of institutional learning rather than rebuilding it from scratch.

Forward linkages describe what RMG and leather can create together, the new markets, products, and policy environments that emerge from their convergence. In the Product Space framework, these represent movements toward higher complexity, higher value nodes that neither sector could reach independently.

In conclusion, Bangladesh’s NBR Customs Tariff 2025–2026 exposes a policy contradiction at the heart of the leather sector’s stagnation. Raw hides leave the country at a Total Tax Incidence of just 7–10%, while finished leather goods bear a burden of up to 89.32%, a structure that inadvertently rewards raw material export over domestic value addition. Closing this gap requires graduated policy correction: phased export duties on raw hides to discourage unprocessed exports, paired with a reduced tax burden on finished goods to make value-added production the commercially rational choice.

Yet taxation alone cannot unlock the sector’s potential. The deeper constraint is capacity, and this is precisely where the RMG sector’s institutional legacy becomes the leather sector’s most asset. The skills, compliance infrastructure, buyer networks, training institutions, and export finance channels that RMG has built over decades represent a ready-made scaffold for leather sector upgrading. Transferring this ecosystem, through shared ETP facilities, compliance advisory, finishing technology investment, and workforce cross-training — builds the SME capacity needed to absorb the policy shift and redirect raw material into compliant, finished, export-ready goods.

Bangladesh’s RMG sector has already proven that deliberate policy, institutional investment, and export ecosystem development can transform a nascent industry into a global powerhouse. Applying the same logic to leather correcting the tax structure, transferring institutional knowledge, and investing in SME capacity in a coordinated sequence creates the conditions for sustainable, inclusive expansion of the sector. This cross-sectoral approach aligns with global best practices in cluster-based diversification (World Bank, 2024), promotes inclusive industrialization (ADB, 2023), and strengthens macroeconomic resilience through export risk mitigation (IMF, 2022). The policy gap is visible. The solution is already built. What remains is the will to connect the two.

This article was authored by Tasnia Isbat, a Business Analyst at LightCastle Partners.

For further clarification, please contact: [email protected].

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights