GET IN TOUCH

- Please wait...

Bangladesh built its economic rise on one advantage above all others: labour. It was cheap, abundant, and reliable, and the country learned to sell it to the world in three forms. It sells labour embedded in garments. It sells labour directly, through the roughly 12 million workers who earn abroad and send money home.

And it increasingly sells labour by the hour, through a fast-growing base of freelancers and digital service firms. For four decades, this model worked. But as automation and AI begin to reshape global production, services, and employment, the foundations of this labour-driven model are facing a new test.

That model now faces a disruption it was not built to deal with. Automation is replacing physical work. Artificial intelligence is beginning to replace cognitive work. For most economies, these are two separate stories. For Bangladesh, they are one story, because the country is exposed on both fronts at once, and on both fronts, it sits on the side that loses.

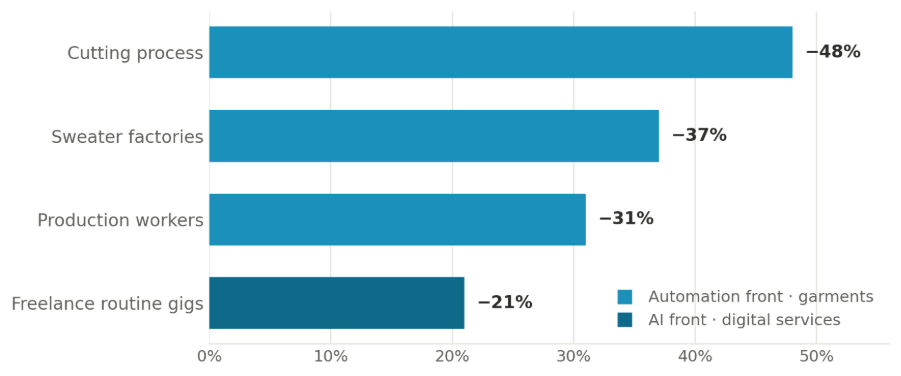

The garment sector shows the pattern most clearly, because the disruption there is no longer a projection. Over the past few years, automation has begun cutting deep into the garment sector labour. One study finds automation has cut the need for production workers by nearly 31 percent, with helpers bearing most of the loss. Cutting was the hardest-hit process at 48 percent, while sweater factories led among subsectors at 37 percent.1

What is exposed extends well beyond garments. RMG employs nearly 4 million people and contributes 14 percent of GDP. Remittance also plays a huge role in terms of employment generation and foreign currency earnings.

Inflows reached a record 30.04 billion dollars in FY 2024-25, equal to roughly 6.57 percent of GDP, and they finance close to 47 percent of the national import bill. Garments and remittance are not two sectors among many. Together, they are the foundation of the country’s foreign earnings and its external stability.

Automation and AI both shift income from labour to capital, rewarding those who own the machines over those who operate them. Bangladesh’s economy sits almost entirely on the labour side of that exchange and owns very little of the capital.

Automation is already eroding the blue-collar work behind the garments and the remittances. AI is now reaching the white-collar and digital work that was meant to be the country’s way up. This article discusses how the mechanism works, why it bites harder across borders than within them, where Bangladesh is most exposed, and what the country can still do.

When a machine substitutes for a worker, the wage disappears, but the output does not. The surplus that the wage used to represent is retained by whoever owns the machine, the software, and the equity behind them. Technology does not destroy the value of the work. It redirects who captures it, from labour to capital.

Automation established this in physical work first, because the substitution is visible. A cutting machine replaces a cutter. The line keeps running. The owner keeps more. AI applies the same logic to cognitive and service work that was long considered protected by its complexity.

The evidence base now supports the pattern. Recent analysis finds that AI reallocates the gains from innovation toward capital, amplifying the share of income that accrues to owners rather than workers, and that the effect arrives as wage compression across the middle and top of the skill distribution rather than the familiar cycle of displacement followed by upskilling.

The wealthiest 1 percent of US households held a record 31.7 percent of all wealth in late 2025, with much of that growth tied to AI-linked equity gains.2 The returns concentrated before the labour market had fully adjusted.

Within a single economy, this is a domestic inequality problem, and rich countries have at least the fiscal capacity to respond. Across borders, the asymmetry is sharper and the buffers are thinner.

The displaced worker sits in Dhaka, Dubai, or Riyadh. The capital that captures the gain sits in California or Shenzhen. Bangladesh supplies the labour that automation displaces and owns almost none of the assets that absorb the returns. The concentration is stark on both counts. UNCTAD finds that just 100 firms, concentrated in the US and China, drive 40 percent of global private R&D, while 118 countries, most of them in the Global South, sit outside the rooms where AI governance is being written.3

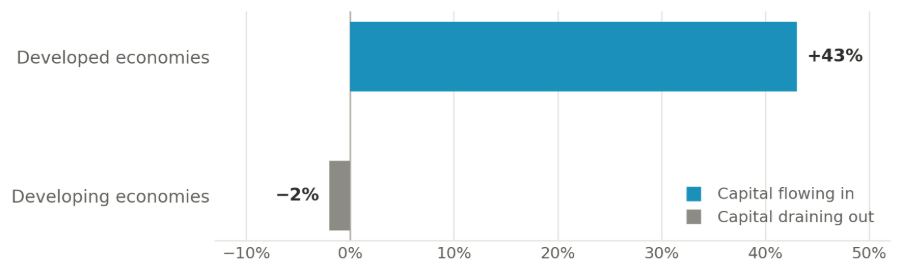

Investment is reinforcing the gap rather than closing it. In 2025, FDI into developed economies climbed 43 percent to roughly USD 728 billion, while developing economies saw a 2 percent decline and three in four least developed countries recorded flat or falling inflows. Data centres alone pulled in over USD 270 billion in announced greenfield investment, almost all of it landing in France, the US, and South Korea.4 The productive base of the AI economy is being built, and it is not being built in Bangladesh.

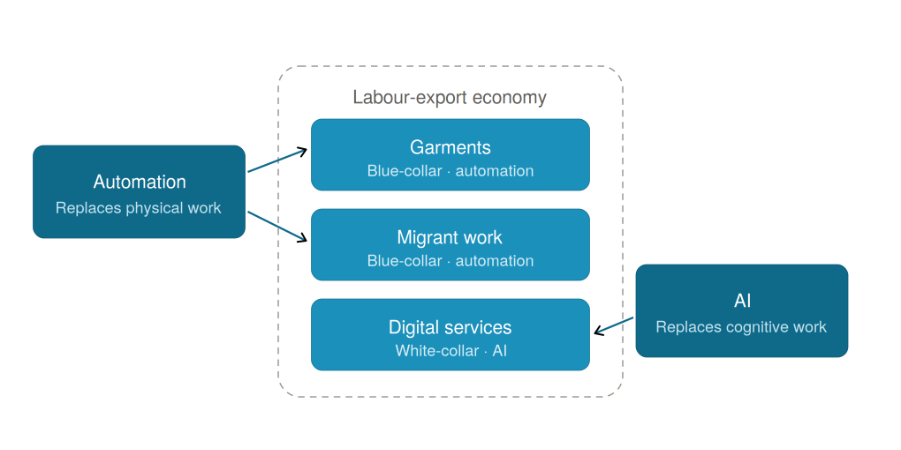

The vulnerability is best understood not as a list of at-risk sectors but as a single structure under pressure from two directions. Bangladesh earns its foreign exchange by selling labour in three forms: garments, migrant work, and digital services, and each rest on the labour side of the divide. Automation threatens the blue-collar share. AI threatens the white-collar share. The two fronts compound.

The first front is physical, and it is already advancing. Domestic RMG automation is the visible edge, and it is now meeting a second shock. Bangladesh loses preferential trade access in 2026 on graduating from Least Developed Country status, precisely as brands shift toward regional production hubs nearer their consumers.5

The distributional burden falls on women, who hold the most automatable roles. One study by Solidaridad found 62 percent of workers reported women being replaced, largely because they were less likely to have the technical skills the new machines required.6 The ILO projects that roughly 60 percent of garment jobs are at risk by 2030-2041.

The same front extends overseas, and this is where the remittance economy becomes the central concern. The migrant workforce is overwhelmingly blue-collar. More than 99 percent of remitters work in blue-collar roles, and the skilled share of outgoing migrants fell from 42 to 44 percent in 2016 to 2019, down to 23 to 24 percent in 2021 to 2024, according to BMET data.

That workforce is concentrated where the pressure is greatest. Around 90 percent of migration flows to the Middle East and Malaysia, and the Gulf is now tightening from two directions simultaneously. The first is automation: Dubai’s robotics programme targets 200,000 robots over the coming decade, and some UAE facility-management firms have aimed to replace a third of their workforce with machines. The second is policy: workforce nationalisation through Saudization, Emiratization, and Omanization is closing expatriate roles by quota. The Bangladeshi worker abroad now faces the robot and the visa rule at once.

The second front is cognitive, and it is arriving in real time. The accepted diversification strategy has been to move labour up and out of low-wage manufacturing into the digital economy, and Bangladesh has built genuine scale there. The freelancing and digital-services base earns around 1.4 billion dollars and has grown by nearly 15 per cent annually,7 alongside a business-process-outsourcing sector worth roughly 850 million dollars across some 400 firms and more than 80,000 jobs.8

The difficulty is that much of this work is routine digital tasking, which is the first category AI absorbs. The World Bank identifies entry-level functions such as data entry, customer service, and IT support as the most exposed. Freelancers are already reporting a contraction of around 21 per cent in routine gigs. As AI handles a growing share of routine coding, the entry rung disappears, and only higher-skill roles remain viable.

The strategic implication is that this is a systemic exposure, not a sectoral one. On both fronts, Bangladesh is a consumer of AI rather than a producer. At this stage, the country, like most of the world, consumes AI products rather than producing them. And because remittances finance close to half the import bill, compression of that inflow does not stop at unemployment.

It transmits to the exchange rate, the balance of payments, and the cost of imported food and fuel. The taka is already under pressure, and domestic job creation is running well below what the labour market requires. A labour shock becomes a foreign-exchange shock, and a foreign-exchange shock becomes a national one.

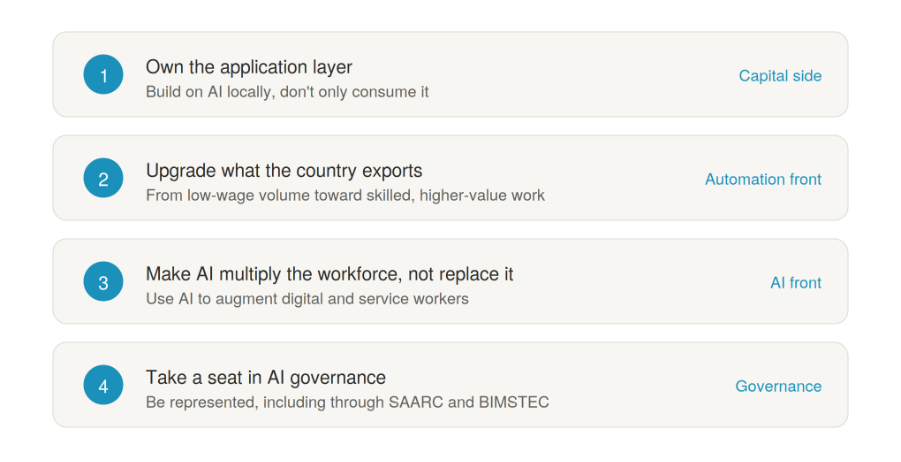

There is a credible case for optimism. Falling inference costs and capable open-weight models are lowering the barrier to adoption, and the history of technological leapfrogging suggests that developing economies can move faster than expected. Ghana has adopted a ten-year national AI strategy with a One Million Coders initiative designed to convert displacement risk into opportunity.10

Bangladesh has the population, the digital base, and a draft policy to pursue a comparable path. But adoption is not the same as ownership, and only one of them changes the country’s position. Skills without ownership leave Bangladesh on the labour side of the very trade it is trying to escape. The economies that capture the AI era will be those that own the machines, not those that remain cheapest to replace.

Bangladesh built its rise on being the world’s affordable workforce, in its factories, on Gulf construction sites, and now at its keyboards. The strategic question is what the country becomes when affordable labour is the one thing the future no longer needs, and whether it will move to own a share of the capital before that question answers itself.

This article was authored by Shoumik Shahriar, Senior Business Consultant & Project Manager at LightCastle Partners. For further clarifications, contact here: [email protected]

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights