GET IN TOUCH

- Please wait...

Bangladesh’s ready-made garment sector has long been one of the country’s strongest engines of growth, employment, and export earnings. Its global position was built on scale, entrepreneurship, competitive production, and the ability to respond to changing buyer requirements. Yet the basis of competitiveness is changing. For apparel exporters, market access is no longer shaped only by cost, capacity, and delivery timelines. It is increasingly shaped by energy reliability, climate performance, environmental compliance, and the ability to finance a industrial upgrading and sustaining a green transition.

This shift is especially important for Bangladesh. The country’s RMG sector is operating in an environment where energy costs are rising, imported fuel dependence is creating macroeconomic pressure, global brands are tightening sustainability expectations, and export markets are moving toward more demanding disclosure and compliance regimes. While this green transition is often framed as an environmental objective, it is increasingly becoming a strategic business imperative for the sector.

It was against this backdrop that LightCastle Partners, under the Oporajita Phase 2 initiative supported by The Asia Foundation, recently convened a high-level Access to Finance Roundtable session in Dhaka. The discussion brought together government officials, development finance institutions, commercial banks, industry leaders, and development partners to examine why green finance remains insufficient despite growing demand for industrial decarbonization.

The case for green industrial investment is increasingly linked to energy security. Bangladesh’s dependence on imported fossil fuels has exposed the economy to global price volatility and supply disruptions. The country imports a significant share, approximately 65%, of its primary energy, while liquefied natural gas supply remains vulnerable to external shocks and geopolitical risks.i

This vulnerability has direct implications for industry. Apparel manufacturing depends on reliable and affordable energy. When energy prices rise or supply becomes uncertain, production costs increase, delivery reliability weakens, and margins come under pressure. These risks are no longer peripheral. They affect the long-term competitiveness of exporters.

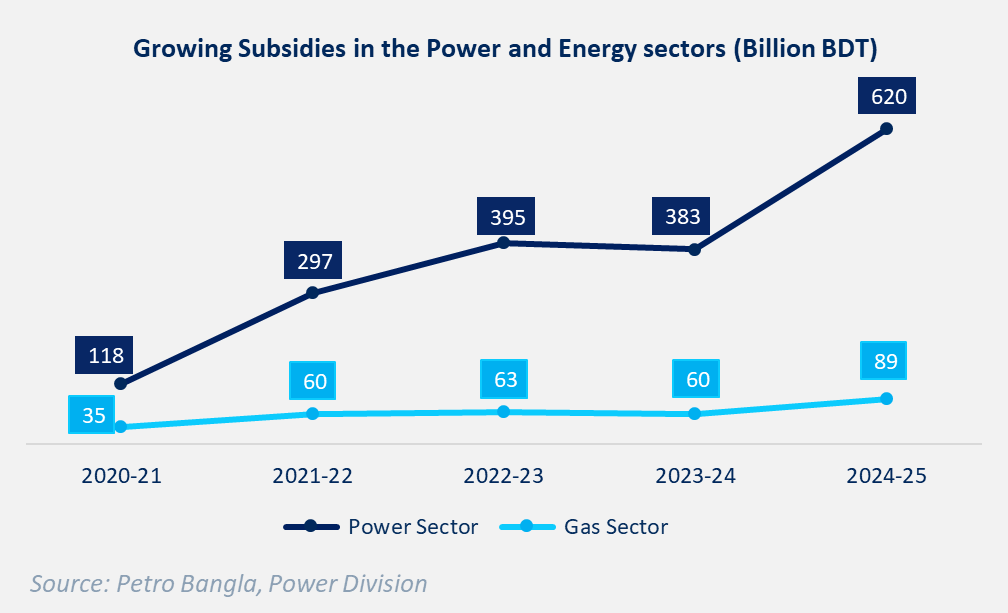

The fiscal burden is also becoming more visible. Power and energy subsidies have risen sharply in recent years, reflecting the increasing cost of maintaining energy supply. This makes industrial energy transition relevant not only for factories, but also for public finance and macroeconomic stability. Investments in renewable energy and energy efficiency can help reduce exposure to imported fuel, lower operating costs, and improve resilience across the apparel value chain.

Bangladesh’s apparel manufacturers are facing a convergence of three pressures. First, regulatory requirements in major export markets are becoming more stringent. The European Union is advancing new sustainability disclosure, due diligence, and environmental compliance regimes that will increasingly affect global supply chains.

Second, buyer expectations are changing. Major international brands are setting decarbonization targets across their supply chains, including Scope 3 emissions. This means suppliers will increasingly be assessed not only on product quality and cost, but also on energy sources, emissions performance, resource efficiency, and traceability.

Third, Bangladesh’s upcoming LDC graduation will create a more competitive trade environment. As preferential market access changes, the sector will need to strengthen productivity, compliance, and value-chain resilience to sustain its position.

Together, these pressures are accelerating the need for investment in cleaner energy, energy efficiency, process upgrading, wastewater management, and broader environmental performance. The challenge is that the investment requirement is significantly larger than the finance currently available.

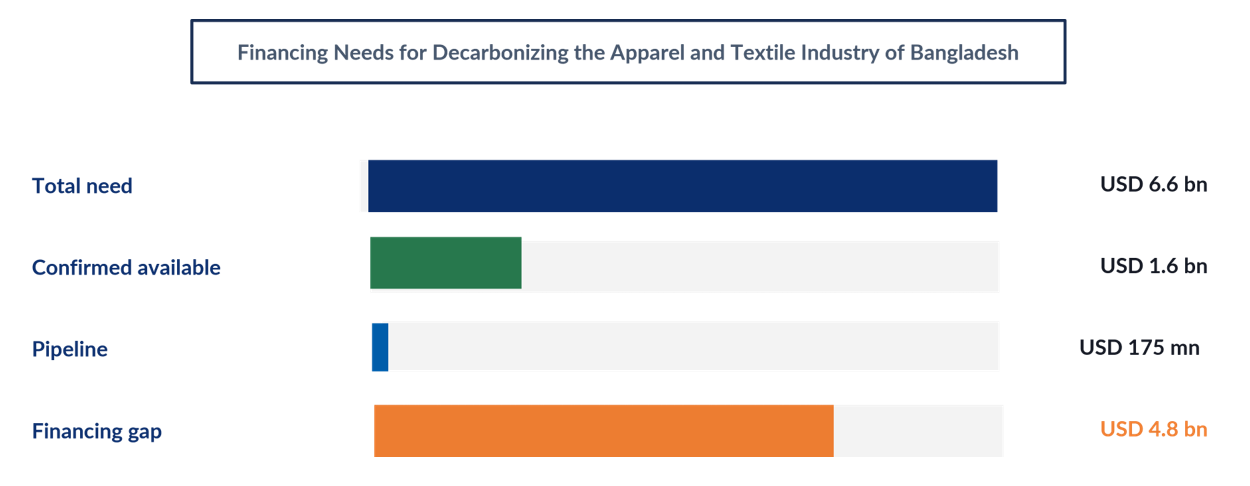

The RMG sector is estimated to require around USD 6.6 billion to achieve a 50 percent greenhouse gas reduction by 2030. This implies an annual investment requirement of roughly USD 1.29 billion for renewable energy and energy-efficiency upgrades.ii Against this requirement, confirmed available financing stands at around USD 1.6 billion, with a further USD 175 million in the pipeline. This leaves an estimated unmet financing need of around USD 4.8 billion between 2025 and 2029.iii

The size of the gap is only one part of the challenge. Many decarbonization investments require substantial upfront capital. Combined renewable-energy and energy-efficiency interventions can cost millions of dollars per factory, while energy audits and technical assessments add further costs before financing can even be secured. For larger manufacturers, these investments may be manageable. For smaller and mid-sized factories, they can be difficult to absorb without concessional finance, technical support, and repayment structures that reflect project cash flows.

Bangladesh has made important progress in building the policy foundation for sustainable finance. The Sustainable Finance Policy, Environmental and Social Risk Management Guidelines, Green Bond Financing Policy, sustainability disclosure requirements, and climate risk guidelines have strengthened the financial sector’s ability to recognize environmental and social risks. These are important foundations. However, the current policy architecture is still stronger on risk management and disclosure than on active capital allocation for industrial decarbonization.

Several domestic and international facilities already support green investment in Bangladesh. These include refinancing windows, technology upgrade funds, climate finance channels, and grant-blended facilities. Yet availability does not automatically translate into accessibility.

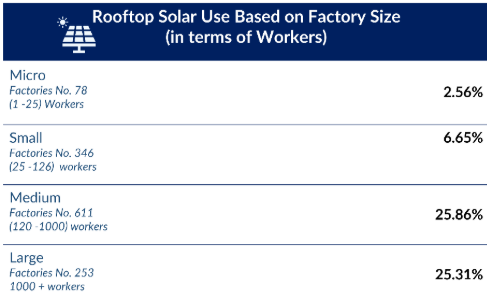

One major constraint is that green finance often reaches stronger borrowers first. Larger factories with better collateral, stronger banking relationships, and higher compliance standards are better positioned to access available funds.

Smaller factories, especially those with older infrastructure or weaker compliance records, often face greater difficulty. This creates a difficult sequencing problem. Factories may need finance to improve compliance, but they may also need compliance to qualify for finance.

There is also a mismatch between financing tenors and asset lifecycles. Many renewable energy and energy-efficiency investments generate savings over several years. If loan tenors are too short, even commercially viable projects can create near-term cash-flow pressure. This discourages adoption, particularly among manufacturers with limited financial flexibility.

Another constraint is the lack of standardized sustainability-linked financing for the RMG sector. Where such facilities exist, they are often bespoke and costly to structure. Without standardized templates, common performance indicators, and predictable pricing mechanisms linked to verified environmental outcomes, smaller firms remain largely excluded from performance-based financing.

Administrative and fiscal issues also affect project economics. Approval timelines, duty structures, and uneven treatment of capital and service-based renewable energy models can increase costs and reduce returns. These frictions are especially important for rooftop solar and energy-efficiency projects, where deployment potential exists, but project economics must be reliable enough to attract both factories and financiers.

While renewable energy receives much of the attention, energy efficiency may offer one of the fastest and most cost-effective pathways for near-term decarbonization. Measures such as efficient motors, waste heat recovery, improved steam systems, LED lighting, and energy management systems can reduce energy consumption while improving productivity.

For manufacturers, energy efficiency has a practical advantage. It lowers operating costs and reduces exposure to energy price volatility. For the financial sector, it can offer relatively shorter payback periods compared with larger renewable energy investments. At scale, energy efficiency could generate substantial savings across the industrial sector, helping reduce both emissions and energy demand.

This makes energy efficiency a strong entry point for green finance. It can help factories build a track record of successful transition investment before moving into larger renewable energy or cleaner production projects.

Experience from regional markets suggests that green finance becomes more effective when it is standardized, aggregated, and de-risked. Vietnam has shown the value of integrating environmental and social risk management into the banking system while developing sector-relevant green credit channels.iv India has demonstrated the importance of aggregation and credit support for smaller enterprises that cannot access capital markets individually.v Indonesia has highlighted the role of transition finance and blended capital in reaching manufacturers that are important to supply-chain decarbonization but often excluded from traditional finance.vi

For Bangladesh, the lesson is not to replicate any one model directly. Rather, the key is to design financing mechanisms that reflect the structure of the RMG sector. This means recognizing the needs of smaller factories, reducing transaction costs, aligning repayment terms with project economics, and using concessional capital and guarantees to mobilize commercial finance.

Bangladesh’s green-finance challenge is often described as a funding gap. That is accurate, but incomplete. The deeper issue is whether the financing system is structured to deliver capital where it is most needed. Existing policies and facilities provide a credible starting point, but they need to evolve from risk screening toward transition enablement.

This will require stronger coordination among regulators, banks, development finance institutions, industry associations, buyers, and manufacturers. It will also require practical mechanisms that support compliance-in-progress factories, standardize sustainability-linked lending, improve access to long-tenor finance, and reduce project risks for commercial lenders.

The opportunity is significant. If Bangladesh can align green finance with industrial competitiveness, the RMG sector can strengthen its resilience, reduce energy vulnerability, and remain competitive in a changing global market. The transition is not only about meeting sustainability expectations. It is about preparing the country’s most important export industry for the next phase of growth.

This article was co-authored by Shoumik Shahriar, Project Manager and Senior Business Consultant and Safin Sadique, a Business Analyst working in the Development & Management Consulting department at LightCastle Partners. For further clarifications, contact us here: [email protected]

[i] IEEFA Report on Primary Energy Import Reliance: https://www.thedailystar.net/business/news/reliance-expensive-fossil-fuel-imports-making-power-sector-unsustainable-ieefa-3608751

[ii] IEEFA RE financing requirement: https://ieefa.org/resources/catalysing-renewable-energy-finance-bangladesh

[iii] Aii/DFI financing gap estimates (2025): https://apparelimpact.org

PPP guidelines detail (PV Magazine): https://www.pv-magazine.com/2026/04/21/bangladesh-opens-public-land-to-utility-scale-solar-under-ppp-model/

[iv] Green credit ~USD 27.1–27.5 bn (Q1 2025)https://www.reccessary.com/en/news/vietnam-financial-sector-accelerates-esg-adoption

[v] 63 million MSMEs in Indiahttps://ieefa.org/resources/how-mobilise-green-finance-indian-micro-small-and-medium-enterprises. CGTMSE Loan: https://www.dmifinance.in/business-loan/cgtmse-loan-scheme/

[vi] Indonesia ETM: https://unfccc.int/sites/default/files/resource/14_Indonesia%20present%20on%20just%20energy%20transition%20mechanism_Noor.pdf

https://www.ptsmi.co.id/indonesia-etm

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights