GET IN TOUCH

- Please wait...

Bangladesh’s Ready-made garments account for approximately 81% of total merchandise export earnings.1 This concentration has delivered decades of growth but left the country structurally fragile. This vulnerability was exposed between 2024 and 2025, when the political situation, escalating US reciprocal tariffs. And India’s cancellation of transhipment arrangements converged to pressure the country’s trade position simultaneously. Such situations highlight the urgency of developing credible alternative export engines, among which leather and footwear stand out as one of the most investment-ready and globally competitive sectors in Bangladesh’s industrial base.

Bangladesh possesses the raw-material base, manufacturing scale, and labour-cost structure to make the leather and footwear sector the next success story in exports. However, the sector has consistently failed to convert production scale into export value so far. This article examines why this sector hasn’t grown, and what interventions are required to make the leather and footwear sector a driver of our export growth.

Bangladesh’s leather and footwear sector is built on structural advantages that are difficult to replicate. The country’s domestic livestock population represents approximately 2.4% of global livestock, enabling annual processing of around 35 million square feet of leather and accounting for roughly 1.1-1.3% of global leather output, almost entirely sourced domestically.2 This distinguishes Bangladesh from competing exporters such as Vietnam, which rely heavily on imported hides and skins. In non-leather footwear, however, the picture diverges: an estimated 80-90% of key synthetic inputs, including EVA and PU compounds, rubber soles, and adhesives, are imported, primarily from China, Taiwan, and South Korea.

Annual footwear production stands at approximately 423 million pairs across more than 3,600 units, comprising over 3,500 MSMEs and roughly 90 large export-oriented factories.3 The value chain employs an estimated 850,000 workers, and domestic consumption of 355 million pairs annually provides stable capacity utilization.4 Labor costs remain significantly lower than those in Vietnam and Indonesia, thereby sustaining competitiveness in cutting, stitching, and finishing. However, most of the workforce is unskilled or semi-skilled, with productivity running 30-40% below comparable Vietnamese factories.

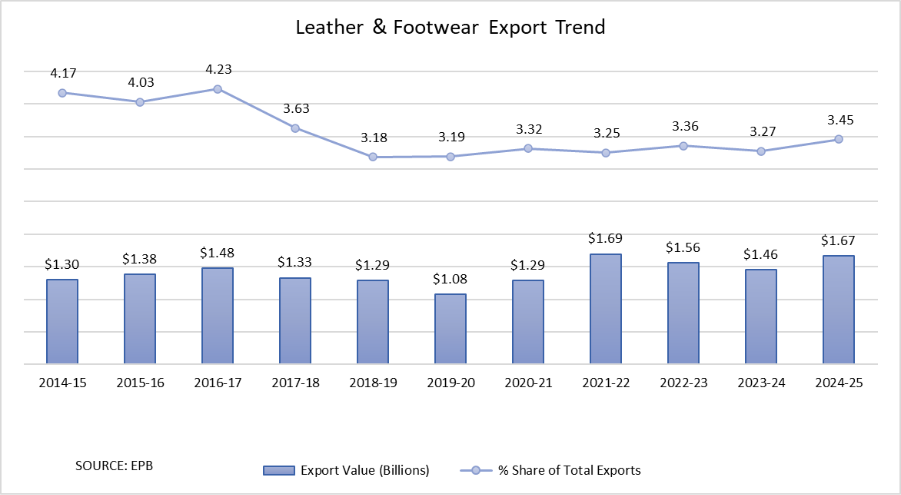

Bangladesh’s leather goods and footwear sector is the country’s largest non-RMG manufacturing export category, yet its export performance has remained broadly stagnant for over a decade. Total exports have hovered between USD 1 billion and USD 1.7 billion since the early 2010s, contributing approximately 3% of total merchandise export earnings. In FY2024-25, total leather goods and footwear exports reached USD 1.67 billion, with footwear alone accounting for 72% of that figure at approximately USD 1.19 billion.5 This growth in footwear, however, masks deterioration elsewhere. Finished leather exports declined sharply following the relocation of tanneries from Hazaribagh to Savar in 2017 and have not recovered to pre-relocation levels.

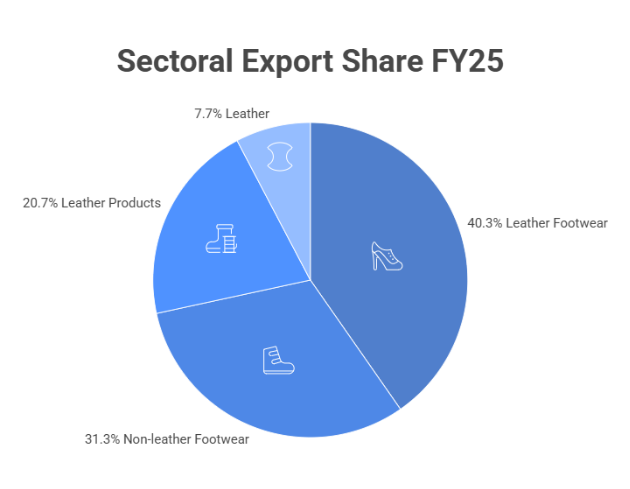

Within footwear, leather footwear remains the dominant export category. At approximately USD 672 million in FY2024-25, equivalent to roughly 40% of total sector revenues. Non-leather footwear is the fastest-growing segment. The sector expanded from low double-digit export shares in the early 2010s to approximately 31% of sector revenues today. Leather goods, including bags, wallets, belts and accessories, account for approximately 20% of sector exports, while finished leather contributes around 7%. 6

Bangladesh currently exports approximately 85 million pairs of footwear annually. That is equivalent to 20% of its 423 million pairs of annual production. At average export price of USD 15 per pair, Bangladesh is positioned above basic rubber and plastic footwear at USD 7 per pair. But it is well below the premium leather footwear average of USD 31 per pair. And Vietnam’s average export price of USD 35-40 per pair.7 This pricing gap reflects the sector’s concentration in mid-tier segments and limited progression into higher-value original design manufacturer or compliance-certified supply chains, where unit values and order stability are materially stronger.

The global footwear market exceeds USD 450 billion annually, expanding at a CAGR of 6.75%, with production stable at approximately 23-24 billion pairs per year. Asia dominates both production and consumption, accounting for 54.7% of global footwear consumption by volume. China holds a 17.1% global consumption share, India 12.4%, and the United States 9.4%. Bangladesh ranks 9th globally in footwear consumption at 1.7% of the world’s share. 8

| Continent | Percentage of Total Footwear Consumption |

| Asia | 54.7% |

| Europe | 13.9% |

| North America | 13.4% |

| Africa | 10.3% |

| South America | 6.8% |

| Oceania | 0.9% |

On the production side, China accounts for 55% of global output and 29.4% of world export value. While Vietnam, with only 6.3% of global production, captures 17.1% of world export value at an export orientation of 95.3%. Bangladesh, producing 1.9% of global output, captures only 0.8% of world export value, a conversion gap that reflects structural constraints rather than any absence of global demand.

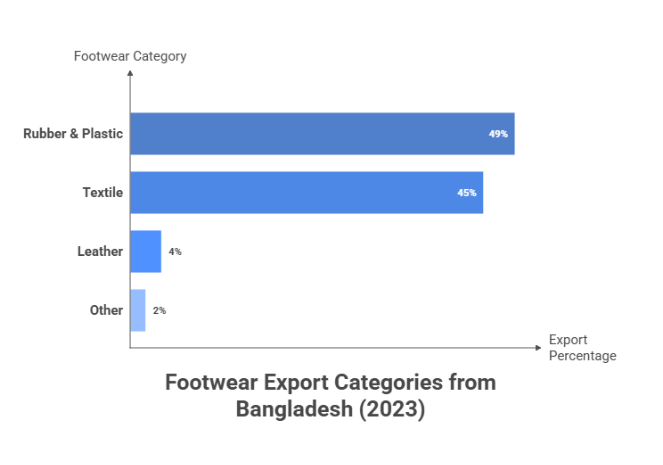

Product mix dynamics are shifting materially. Rubber and plastic footwear dominate global export volume at 50% of pairs traded. While leather footwear, representing only 15% of volume, commands 37% of total export value. At an average price of USD 31 per pair, compared to USD 7 for rubber and plastic and USD 12 for textile footwear. Non-leather segments, particularly athletic, casual, and synthetic footwear, now account for approximately USD 280-300 billion of the global market. And are also growing faster than leather across all major consumption markets. This is driven by shifting consumer preferences toward sustainable and animal-welfare-friendly alternatives.

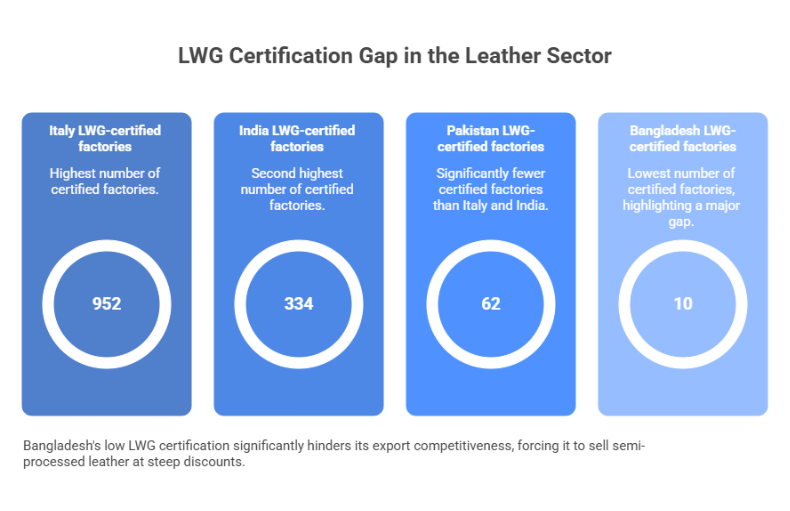

The European Union represents the highest-value destination cluster for Bangladeshi exporters, supported by duty-free, quota-free access under the Everything But Arms initiative. However, effective EU market participation is increasingly conditioned on REACH chemical compliance, ZDHC protocols, and LWG certification. With LDC graduation approaching in 2026, Bangladesh faces potential MFN tariff exposure of 10-17% in the EU and 12-18% in the UK. That is sufficient to eliminate exporter margins in price-sensitive segments without preferential replacement arrangements. Japan and South Korea, both among the top five global footwear consumers with rising purchasing power parity, remain significantly underpenetrated despite offering stable demand and geographic diversification.

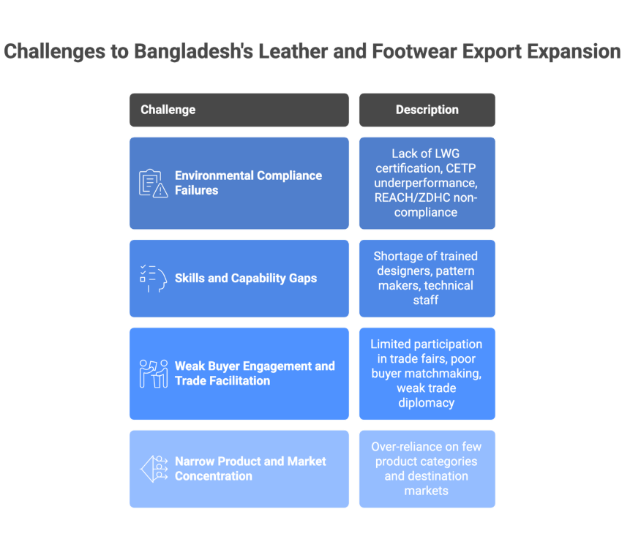

Bangladesh’s leather and footwear sector is not constrained by demand, production capacity, or labour availability. It is constrained by export eligibility. The following challenges represent the most binding barriers preventing the sector from converting production scale into export value.

1. Environmental Compliance Failures Systematically Exclude Bangladesh from Premium Markets

The relocation of tanneries from Hazaribagh to the Savar Tannery Industrial Estate in 2017 was intended to resolve environmental non-compliance through centralized waste treatment. Instead, weak governance has entrenched the problem. The Central Effluent Treatment Plant, built for BDT 565 crore, operates at only approximately 14,000 cubic meters per day against peak wastewater generation of 35,000 cubic meters, with untreated effluent continuing to discharge into the Dhaleshwari River. The market consequences are direct. Non-compliant tanneries cannot obtain Leather Working Group certification. This forces exports into semi-processed wet blue leather shipments to China at significant price discounts relative to finished leather. Compliance failures also restrict credit access, creating a self-reinforcing compliance-finance trap that perpetuates underinvestment across the leather value chain.

2. Skills and Capability Gaps Prevent Value Upgrading

Industry diagnostics indicate that a large part of the footwear workforce is unskilled or semi-skilled. Comparitive productivity running 30-40% below Vietnamese factories. Workers typically lack formal training in export-critical functions, including precision cutting, finishing, quality inspection, and compliance documentation. Translating directly into higher defect rates and weaker buyer confidence. While leather goods can achieve significantly higher value addition when supported by skilled design and finishing capabilities, Bangladesh remains concentrated in basic OEM manufacturing. The country lacks dedicated footwear design institutes and buyer-linked training centres. The kind that supported upgrading in Vietnam and Indonesia. As global buyers consolidate sourcing toward fewer, more capable suppliers, this skills deficit has become a structural barrier to value upgrading regardless of improvements elsewhere.

3. Weak Buyer Engagement and Trade Facilitation Constrain Market Access

Despite operating in the fastest-growing segment of global demand, Bangladesh’s non-leather footwear exports remain concentrated in low-value regional markets. Most exporters rely on buying houses or opportunistic orders with limited investment in direct buyer outreach or participation in major trade fairs and sourcing platforms in Europe and East Asia. Without systematic engagement with global sourcing networks, Bangladeshi firms struggle to move beyond transactional relationships. Long-term supply agreements unlock higher order volumes, design collaboration and preferential pricing. The absence of a structured trade facilitation framework, including buyer matchmaking, export promotion through international sourcing events, and dedicated outreach to key markets such as Germany, the Netherlands, Japan, and South Korea, leaves significant market access potential unrealized.

4. Narrow Product and Market Concentration Increase Export Vulnerability

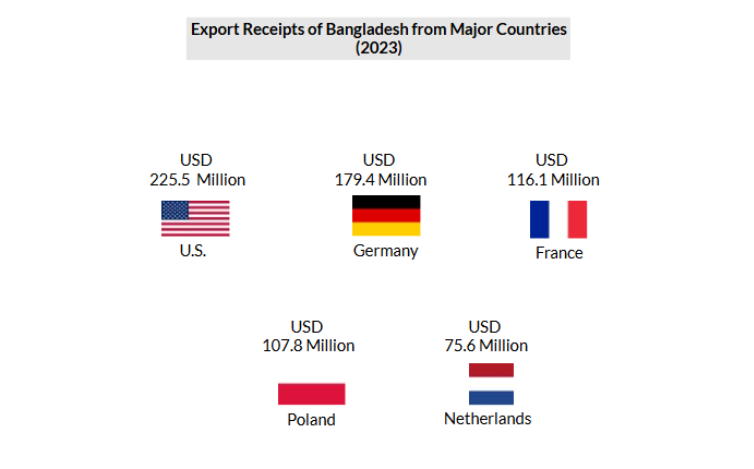

Leather footwear alone accounts for approximately 40% of total sector export revenues, exposing performance to product-specific compliance tightening and tariff risk. Non-leather footwear, despite recording a high CAGR over the past decade, represents only 30% of sector revenues against a 60-70% share of global footwear demand. Geographically, the top five markets of the United States, Germany, France, Poland, and the Netherlands absorb most export receipts. While Japan, South Korea, Canada, and Australia collectively account for less than 10% of sector exports. This concentration amplifies the impact of any single market disruption and heightens post-LDC tariff exposure given the absence of preferential arrangements beyond EBA.

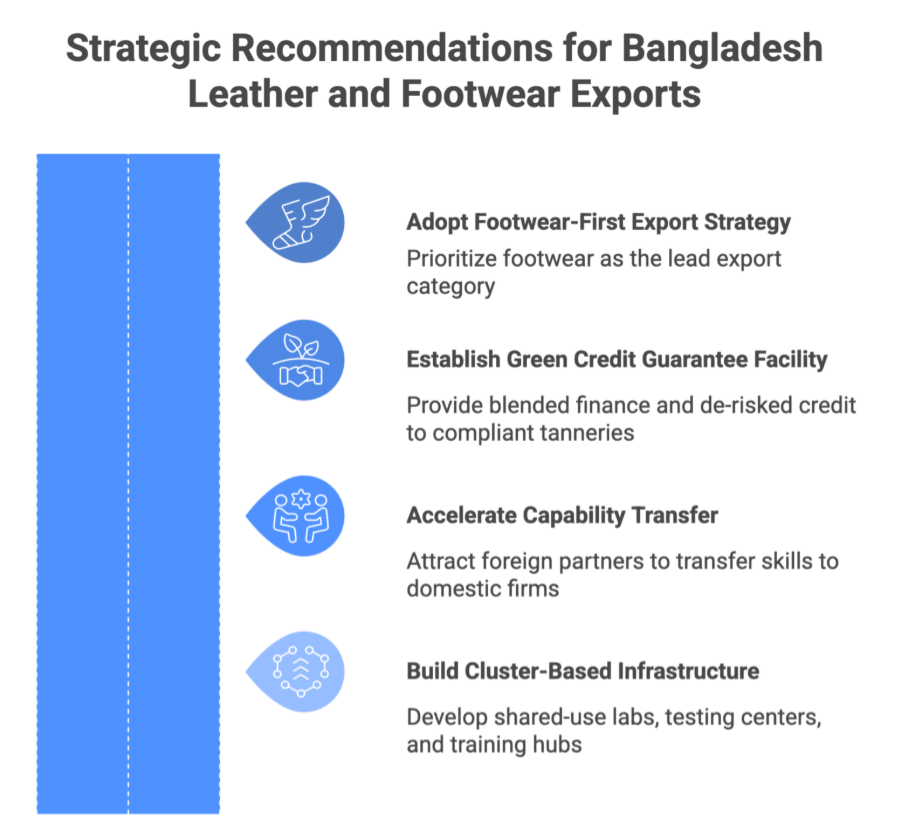

1. Adopt a Footwear-First Export Strategy

Footwear already accounts for 70% of sector exports and is the only segment recording consistent growth. The export strategy should focus on finished footwear with an explicit tilt toward non-leather segments, where 60-70% of global demand is concentrated, and compliance risks are more manageable than in leather processing. Bangladesh’s non-leather footwear share of 30% of sector revenues remains severely misaligned with global demand patterns. Incremental ODM upgrading through limited design input, material optimization, and in-house compliance ownership can raise average export prices from the current USD 15 per pair toward the USD 25-27 range without requiring full branding investment, as demonstrated by Indonesia’s export price trajectory between 2008 and 2018.

2. Establish a Green Credit Guarantee Facility Linked to Certification Milestones

SMEs currently face collateral requirements of 120-150%, and loan tenors are also quite short, which are structurally incompatible with compliance investments that pay back over multiple production cycles. Bangladesh Bank should establish a green credit guarantee window explicitly linked to buyer-recognized standards, including LWG, REACH, and ZDHC, with guaranteed tranches released against verified certification progress to limit moral hazard. Italy’s SACE green guarantee model, which links state-backed credit to environmental certification in leather clusters, provides a proven reference point. Fiscal incentives should be gradually shifted from cash rebates toward co-financing for certification, testing, and audits, particularly for firms targeting post-LDC markets where compliance is a binding entry condition.

3. Accelerate Capability Transfer through Targeted Joint Ventures

The footwear sector remains predominantly domestically owned, limiting access to advanced production engineering, compliance systems, and buyer-linked operating models. Joint ventures with investors from Taiwan, South Korea, and Vietnam, who bring proven experience supplying global footwear brands, represent the fastest lower-risk pathway to capability transfer at scale. Over 70% of Vietnam’s footwear exports are produced in FDI-backed or joint-venture facilities, a structure that enabled the rapid transfer of technology, management practices, and compliance systems. Investment promotion agencies should move beyond passive facilitation and actively broker footwear-specific JV partnerships.

4. Build Cluster-Based Testing, Certification, and Skills Infrastructure

Most exporters currently rely on overseas laboratories in India, China, or Europe for chemical and performance testing, adding lead times, costs, and rejection risk that disproportionately affect smaller exporters. National leather goods and footwear testing hubs should be established within production clusters under PPP models, accredited to ISO/IEC 17025 to support LWG, REACH, ZDHC, and buyer-specific requirements. Skills upgrading must be export-task specific, focused on supervisors, quality controllers, lab technicians, and compliance managers directly responsible for export outcomes.

Bangladesh’s leather and footwear sector sits at a structural inflection point. The combination of global sourcing shifts, rising competitor costs, and a domestic raw material base that no regional peer can replicate makes the export opportunity significant. Yet the sector has repeatedly failed to convert these advantages into market share, and the policy and institutional conditions that allowed that failure to persist are running out of time. The path forward requires coordinated action across environmental governance, skills development, and market engagement. Whether Bangladesh treats this moment as a catalyst or allows it to pass will determine whether leather and footwear become a second export pillar or remain a sector of perpetually unrealized potential.

This article was authored by Shoumik Shahriar, Senior Business Consultant & Project Manager at LightCastle Partners.

For further clarifications, contact here: [email protected]

1. Bangladesh Garment Manufacturers and Exporters Association. (n.d.). Export performance.

2. Bangladesh Investment Development Authority. (n.d.). Leather and footwear sector.

3. Bangladesh Investment Development Authority. (n.d.). Leather and footwear sector.

4. World Footwear. (2023). The World Footwear Yearbook 2023.

5. Leather Goods and Footwear Manufacturers & Exporters Association of Bangladesh (LFMEAB). (n.d.). Sector data and industry insights.

6. Export Promotion Bureau (EPB). (2025). Export statistics (FY2024–25). Government of Bangladesh.

7. World Footwear. (2023). The World Footwear Yearbook 2023.

8. World Footwear. (2023). The World Footwear Yearbook 2023.

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights