GET IN TOUCH

- Please wait...

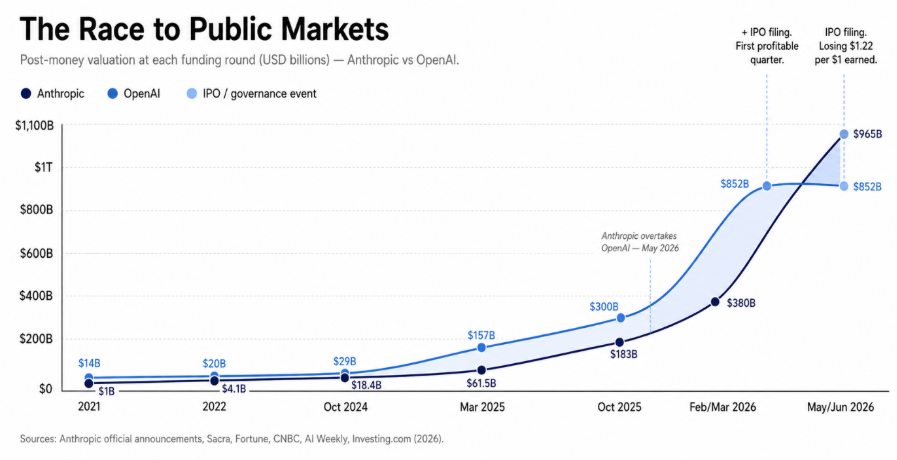

On February 27, 2026, a defining moment in the global AI governance race unfolded when the U.S. Department of Defense gave Anthropic an ultimatum: remove its restrictions on autonomous weapons and mass surveillance or lose the contract. Anthropic declined. Hours later, OpenAI announced its own Pentagon deal while claiming the same ethical red lines. The Pentagon accepted those commitments from one company and rejected them from the other, without releasing the contract to the public.

Three months later, both companies filed confidential S-1s with the SEC just days apart. They are now racing toward the public markets at the same time.

The numbers tell two very different stories.

The company that refused the Pentagon is now worth more than the company that accepted the deal. That outcome is no coincidence. It marks the opening signal of the decade’s most consequential economic race and the first public-market test of whether governance design creates long-term value.

Sovereign wealth funds committed an estimated $120 billion to AI infrastructure during 2025–2026 alone. The investment covered data centres, semiconductor fabrication, and high-performance computing networks. WEF and Bain project that annual AI investment will reach $1.5 trillion for applications and $400 billion for infrastructure by 2030. At the same time, Anthropic’s near-trillion-dollar IPO and SpaceX’s targeted $1.77 trillion valuation represent what analysts describe as the largest concentration of capital ever brought to market simultaneously.

This concentration of capital is reshaping the global economic and political landscape. Courtrooms, S-1 filings, defence procurement decisions, and corporate governance structures are now determining who owns, governs, and profits from frontier AI.

The implication is stark. The global AI economy is not only taking shape but also establishing its governing rules in real time. Companies and governments that move first are deciding how the world will manage safety, data, sovereignty, and access. Those decisions will shape the global economy for decades.

The implication is stark: the global AI economy is not just being built; it is being governed in real time by the companies and states moving fastest. And the governance choices being made now about safety, data, sovereignty, and access will shape the economic landscape for decades.

One critical issue in the governance race remains unresolved: distribution. The countries writing the rules are not the same countries that will bear the consequences.

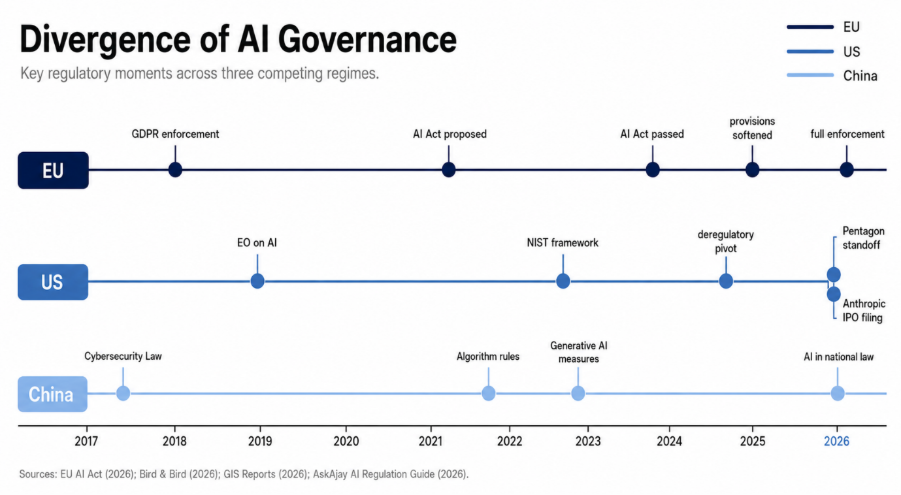

The global record on digital regulation offers a useful reference point. When the EU’s GDPR came into force in 2018, monthly venture capital deals for European tech startups fell by an average of 26% compared with the United States.⁷

The sharpest decline occurred in experimental, cross-border, and data-intensive innovation rather than routine R&D. These activities rely on open data flows, international research partnerships, and the ability to move information across jurisdictions.

Privacy regulation often redirects innovation. It tends to constrain activities that depend heavily on data sharing while leaving less data-intensive work relatively unaffected.⁸

The welfare effects of data regulation depend heavily on context. Strong protections can support innovation in some environments and hinder it in others, depending on institutional capacity and implementation quality.⁹

China’s Cybersecurity Law of 2017 produced similar outcomes. Data-sensitive sectors felt the strongest effects, while smaller and less-capitalised firms carried the heaviest adjustment burden.¹⁰

Despite its ambitions, policymakers have already begun softening the EU AI Act under competitive pressure. As France, Germany, and the UK shift their focus toward industrial policy, they have delayed high-risk provisions and scaled back liability frameworks.¹¹

The pattern is clear. Powerful economies write ambitious rules and then soften them when competitive pressures increase. Countries with less institutional capacity often absorb the costs. They inherit regulatory frameworks they cannot easily implement and lack the leverage to renegotiate.

The same sectors consistently face the greatest pressure: technology, financial services, and healthcare. These industries handle sensitive data, face the most direct compliance requirements, and offer some of the strongest opportunities for digital transformation. As a result, the heaviest compliance burdens often fall on the sectors with the greatest innovation potential.

Capital concentration is shaping the governance architecture of the AI economy. For economies that remain outside these discussions, the window to influence either is rapidly closing.

The UK launched a £500 million Sovereign AI Fund to avoid becoming an “AI taker.”¹² The European Commission proposed sweeping measures to strengthen domestic AI and cloud services while reducing reliance on U.S. and Chinese providers. The first Global South AI Summit attracted more than 100 countries and 20 heads of state, securing investment commitments exceeding $200 billion.¹³ Senator Bernie Sanders also proposed an American AI Sovereign Wealth Fund Act, arguing that the wealth generated by AI should belong, at least in part, to the public whose knowledge and labour helped train these systems.¹⁴

These initiatives reflect a broader reality: the architecture of the AI economy is taking shape now. Countries that develop regulatory frameworks in isolation—or simply copy those of their peers—will inherit more than compliance obligations. They may also import the same innovation constraints into the sectors they most need to grow.

The economies missing from this race are concentrated in a few regions. Africa, for example, accounts for less than 1% of global data-centre capacity despite hosting 18% of the world’s population.¹⁵ Together, Africa and Latin America account for only about 3% of global AI-specialised data-centre hosting capacity.¹⁶

Since 2023, entrepreneurs have launched more than 4,000 venture-backed AI companies in the United States alone. During a recent period, the world’s ten largest AI investors directed $96 billion into U.S.-based funding rounds.¹⁷ Meanwhile, most of South Asia, Southeast Asia, and Latin America still depend on external infrastructure. Training a frontier-scale AI model can consume thousands of megawatt-hours of electricity, and many power grids across these regions cannot reliably support that demand.¹⁸

The distributional stakes are far from abstract. WEF and Bain project $1.5 trillion in annual AI application investment by 2030.¹⁹ The key question is not whether that investment will occur, but where it will flow. Capital will favour economies that build regulatory credibility, strengthen digital infrastructure, and participate actively in shaping the rules. Others risk being left behind.

The evidence points to a framework that is neither the most restrictive model nor an absence of regulation. Instead, governments need a system that is calibrated, sequenced, and tailored to the needs of the economy it governs. Ultimately, the jurisdictions that lead the AI economy will be the ones that earn public trust.

Phasing matters more than ambition. Evidence from GDPR and China’s Cybersecurity Law shows that firms need adequate time to build compliance capacity before new regulations take effect. Governments can ease adjustment costs by introducing sector-specific milestones and realistic implementation timelines.

Calibration is equally important. Regulators should match rules to the actual sensitivity of data instead of applying blanket restrictions across the economy. Treating a credit-scoring algorithm the same as a cross-border research collaboration imposes identical compliance costs on activities with very different levels of risk and innovation value. As a result, high-potential innovation is often the first casualty.

Participation may be the most important element of all. Economies that want to shape the future of AI must engage in regional and multilateral standard-setting processes. The alternative is not neutrality. It is accepting standards written elsewhere and calibrated for countries with different priorities, institutional capacity, and economic structures.

The simultaneous IPO filings of Anthropic and OpenAI offer the first real-world test of this idea. Capital markets are now evaluating governance design alongside financial performance. Anthropic embedded safety commitments into its corporate structure, reached profitability, and became the world’s most valuable AI company. OpenAI pursued rapid expansion, weakened its governance under state pressure, and entered the public markets while losing more than it earned. Whichever model proves more resilient under public-market scrutiny will influence how the next generation of AI companies is built, funded, and regulated around the world.

The article was authored by Labiba Anjumi Kabir, Trainee Consultant at LightCastle Partners. For further clarifications, please contact: [email protected].

Acquisti, A., Taylor, C., & Wagman, L. (2016). The economics of privacy. Journal of Economic Literature, 54(2), 442–492. https://doi.org/10.1257/jel.54.2.442

AI Weekly. (2026, June 8). OpenAI files confidential IPO targeting $850B valuation. https://aiweekly.co/alerts/openai-files-confidential-ipo-targeting-850b-valuation

Anthropic. (2023). The Long-Term Benefit Trust. https://www.anthropic.com/news/the-long-term-benefit-trust

Built In. (2026, March 10). OpenAI’s Pentagon AI deal: What the contract allows and how it differs from Anthropic. https://builtin.com/articles/openai-pentagon-deal

Chen, H., Li, C., Liu, J., & Xu, R. (2025). Navigating digital frontiers: The impact of China’s Cybersecurity Law on corporate digital innovation. International Review of Financial Analysis, 103, 104182. https://doi.org/10.1016/j.irfa.2025.104182

CNBC. (2026, June 5). Anthropic’s IPO sets up first big test of AI boom valuations. https://www.cnbc.com/2026/06/05/tech-download-anthropic-ipo-ai-valuations.html

Council of Europe. (2024). Framework Convention on Artificial Intelligence and Human Rights, Democracy and the Rule of Law (CETS No. 225). https://www.coe.int/en/web/artificial-intelligence/the-framework-convention-on-artificial-intelligence

Fortune. (2026, June 1). Anthropic confidentially files for IPO after raising $65 billion. https://fortune.com/2026/06/01/anthropic-confidentially-files-ipo-965-billion-valuation/

GIS Reports. (2026, June 2). The battle for AI sovereignty. https://www.gisreportsonline.com/r/ai-sovereignty/

Goldfarb, A., & Tucker, C. (2012). Privacy and innovation. Innovation Policy and the Economy, 12(1), 65–90. https://doi.org/10.1086/663156

Jia, J., Jin, G. Z., & Wagman, L. (2021). The short-run effects of the General Data Protection Regulation on technology venture investment. Marketing Science, 40(4), 661–684. https://doi.org/10.1287/mksc.2020.1271

Investing.com. (2026, May 20). The trillion-dollar IPO test: SpaceX and OpenAI face public markets. https://www.investing.com/analysis/the-trilliondollar-ipo-test-spacex-and-openai-face-public-markets-200680688

McKinsey & Company. (2026, March). Sovereign AI ecosystems for strategic resilience and economic impact. https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/sovereign-ai-building-ecosystems-for-strategic-resilience-and-impact

Mehra, S. (2017). The impact of China’s 2016 Cyber Security Law on foreign technology firms, and on China’s big data and smart city dreams. Computer Law & Security Review, 33(1), 67–98. https://doi.org/10.1016/j.clsr.2016.11.011

MIT Technology Review. (2026, March 2). OpenAI’s ‘compromise’ with the Pentagon is what Anthropic feared. https://www.technologyreview.com/2026/03/02/1133850/openais-compromise-with-the-pentagon-is-what-anthropic-feared

NPR. (2026, February 27). Trump bans Anthropic, OpenAI announces Pentagon deal. https://www.npr.org/2026/02/27/nx-s1-5729118/trump-anthropic-pentagon-openai-ai-weapons-ban

Porter, M. E., & van der Linde, C. (1995). Toward a new conception of the environment–competitiveness relationship. Journal of Economic Perspectives, 9(4), 97–118. https://doi.org/10.1257/jep.9.4.97

Titan Investors. (2026, February). Sovereign wealth funds commit $120 billion to AI infrastructure buildout. https://titaninvestors.com/insights/sovereign-wealth-funds-ai-infrastructure-2026

World Economic Forum, & Bain & Company. (2026, January). AI investment projections 2030. Presented at the World Economic Forum Annual Meeting 2026.

Our experts can help you solve your unique challenges

Stay up-to-date with our Thought Leadership and Insights